Juicer Market Size

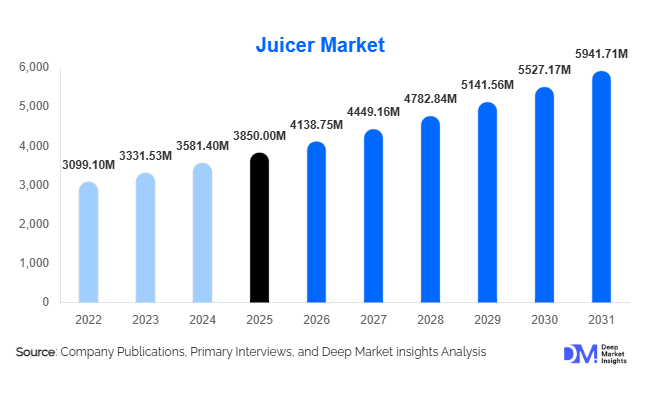

According to Deep Market Insights, the global juicer market size was valued at USD 3,850 million in 2025 and is projected to grow from USD 4,138.75 million in 2026 to reach USD 5,941.71 million by 2031, expanding at a CAGR of 7.5% during the forecast period (2026–2031). The juicer market growth is primarily driven by increasing health consciousness, rising demand for fresh and nutrient-rich beverages, and technological advancements in cold-press and slow juicing systems. The growing adoption of smart kitchen appliances and the expansion of commercial foodservice establishments further support sustained market expansion globally.

Key Market Insights

- Health-conscious consumer behavior is accelerating demand for nutrient-preserving juicing solutions, particularly cold-press juicers.

- Masticating juicers are gaining strong traction due to superior juice quality and higher extraction efficiency compared to centrifugal models.

- Asia-Pacific dominates the market, driven by population size, rising incomes, and growing wellness awareness.

- Commercial applications are the fastest-growing segment, fueled by the expansion of juice bars, cafes, and fitness centers.

- Online retail channels are rapidly expanding, supported by e-commerce penetration and consumer preference for convenience.

- Technological innovations, including smart connectivity and multifunctional appliances, are reshaping product differentiation.

What are the latest trends in the juicer market?

Shift Toward Cold-Press and Nutrient-Preserving Technologies

The market is witnessing a strong transition from traditional centrifugal juicers to cold-press (masticating) technologies. Consumers are increasingly prioritizing juice quality, nutrient retention, and shelf life, which slow juicing methods offer. This trend is particularly prominent in developed markets where health awareness is high. Manufacturers are focusing on improving extraction efficiency, reducing oxidation, and enhancing durability, thereby positioning cold-press juicers as premium offerings. Additionally, the rise of detox diets and wellness programs has further accelerated the adoption of these advanced juicing technologies.

Integration of Smart and Multifunctional Features

Technological advancements are playing a critical role in shaping consumer preferences. Modern juicers are increasingly equipped with smart features such as app connectivity, automated pulp control, and programmable settings. Multifunctional appliances that combine juicing, blending, and food processing capabilities are gaining popularity, particularly among urban households with limited kitchen space. These innovations enhance convenience and efficiency, making juicers more appealing to tech-savvy consumers and contributing to higher adoption rates in premium segments.

What are the key drivers in the juicer market?

Rising Health and Wellness Awareness

The growing prevalence of lifestyle-related diseases and increasing focus on preventive healthcare are driving demand for fresh juice consumption. Consumers are actively seeking ways to incorporate fruits and vegetables into their daily diets, making juicers an essential kitchen appliance. The trend is further supported by social media influence and wellness campaigns promoting healthy living.

Expansion of the Foodservice and Hospitality Industry

The rapid growth of juice bars, cafes, and restaurants is significantly boosting demand for commercial juicers. These establishments are incorporating fresh juice offerings to cater to evolving consumer preferences for healthier beverage options. The increasing number of fitness centers and wellness facilities also contributes to the rising demand in this segment.

What are the restraints for the global market?

High Cost of Premium Juicers

Advanced juicers, particularly masticating and twin-gear models, are relatively expensive, limiting their adoption in price-sensitive markets. The high upfront cost acts as a barrier, especially in developing regions where consumers prioritize affordability.

Availability of Substitute Products

The presence of ready-to-drink packaged juices and smoothies poses a challenge to market growth. These alternatives offer convenience and lower initial costs, which may discourage consumers from investing in juicers. Additionally, maintenance and cleaning requirements can further impact purchasing decisions.

What are the key opportunities in the juicer market?

Expansion in Emerging Markets

Emerging economies such as India, China, and Brazil present significant growth opportunities due to rising disposable incomes and increasing health awareness. Urbanization and the expansion of middle-class populations are driving demand for home appliances, including juicers. Companies offering affordable yet efficient products can capitalize on this growing market segment.

Growth of Commercial Applications

The proliferation of juice bars, wellness cafes, and fitness centers is creating strong demand for commercial-grade juicers. Businesses are increasingly investing in high-capacity and durable machines to meet growing consumer demand for fresh juices. This trend is expected to drive substantial growth in the commercial segment over the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3850 Million |

| Market Size in 2026 | USD 4138.75 Million |

| Market Size in 2031 | USD 5941.71 Million |

| CAGR | 7.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Masticating (cold press) juicers dominate the global market, accounting for approximately 38% of total market share in 2025. The leadership of this segment is primarily driven by the growing consumer preference for nutrient-rich and minimally processed beverages. Masticating juicers operate at low speeds, which helps preserve enzymes, vitamins, and antioxidants, making them highly attractive to health-conscious consumers and wellness-focused households. Additionally, their ability to process a wide range of ingredients, including leafy greens, nuts, and soft fruits, has expanded their usability beyond traditional juicing, further strengthening demand. The premiumization trend in kitchen appliances has also contributed to the growth of this segment, as consumers are increasingly willing to invest in high-performance, durable products.

Centrifugal juicers continue to hold a substantial share, particularly in price-sensitive markets, due to their affordability, faster processing time, and ease of use. These products are widely adopted in entry-level and mass-market segments. Citrus juicers maintain niche demand, especially in commercial environments such as quick-service restaurants and juice bars, where speed and simplicity are critical. Triturating (twin gear) juicers, although limited in volume, cater to a premium customer base seeking maximum extraction efficiency and superior juice quality, particularly in developed markets.

Application Insights

Residential applications account for nearly 70% of the global juicer market, making it the leading segment. This dominance is largely driven by increasing household penetration of kitchen appliances and a strong shift toward healthier lifestyles. Consumers are actively incorporating fresh juices into their daily diets as part of preventive healthcare practices, which has significantly boosted demand. The growing influence of social media, fitness trends, and home-based wellness routines has further accelerated adoption in this segment.

On the other hand, commercial applications are witnessing faster growth, supported by the rapid expansion of foodservice establishments. Juice bars, cafes, hotels, and wellness centers are increasingly offering fresh juice options to cater to evolving consumer preferences. The rise of cold-pressed juice brands and subscription-based juice delivery services has also contributed to commercial demand. Additionally, new application areas such as corporate offices, co-working spaces, and healthcare facilities are integrating juicing solutions into wellness programs, creating incremental growth opportunities.

Distribution Channel Insights

Offline retail channels, including supermarkets, hypermarkets, and specialty stores, continue to dominate the juicer market due to strong consumer preference for in-store product evaluation and immediate purchase. These channels are particularly influential in emerging markets where physical retail infrastructure remains robust. However, online retail is rapidly gaining traction and currently accounts for approximately 40% of total sales, making it the fastest-growing distribution channel.

The growth of e-commerce is driven by factors such as convenience, wider product availability, competitive pricing, and access to customer reviews. Consumers increasingly rely on digital platforms to compare features, prices, and performance before making purchasing decisions. Direct-to-consumer (D2C) channels are also expanding as manufacturers invest in their own online platforms, enabling better brand engagement and higher margins. The integration of digital marketing, influencer promotions, and targeted advertising is further accelerating online sales growth.

End-Use Insights

The residential segment remains the largest end-use category, driven by rising consumer awareness regarding nutrition and healthy living. The increasing adoption of home-based wellness routines, coupled with growing disposable incomes, has significantly contributed to the expansion of this segment. Consumers are increasingly viewing juicers as essential kitchen appliances rather than luxury products, further supporting demand.

Meanwhile, the commercial segment is the fastest-growing, expanding at a CAGR exceeding 9%. This growth is primarily fueled by the global foodservice industry, valued at over USD 3 trillion, which is increasingly incorporating fresh juice offerings into menus. Juice bars, cafes, and quick-service restaurants are key contributors to this demand. Additionally, emerging end-use sectors such as fitness centers, spas, hospitals, and corporate offices are adopting juicers to enhance their service offerings and promote wellness. Export-driven demand is also notable, particularly from manufacturing hubs in Asia, where large-scale production supports global supply chains.

Explore more data points, trends and opportunities Download Free Sample Report

Juicer Market Segmentations

By Product Type

- Centrifugal Juicers

- Masticating (Cold Press) Juicers

- Triturating (Twin Gear) Juicers

- Citrus Juicers

By Application

- Residential

- Commercial

By Distribution Channel

- Online Retail

- Supermarkets/Hypermarkets

- Specialty Stores

- Direct Sales

By End-Use

- Residential

- Hotels & Restaurants

- Juice Bars & Cafés

- Healthcare & Wellness Centers

Regional Insights

Asia-Pacific

Asia-Pacific leads the global juicer market, accounting for approximately 35% of total market share in 2025, driven by a combination of a large population base, rapid urbanization, and rising disposable incomes. China plays a dual role as both the largest manufacturing hub and a major consumer market, benefiting from strong domestic production capabilities and export dominance. India is emerging as the fastest-growing market within the region, supported by increasing health awareness, an expanding middle-class population, and government initiatives promoting domestic manufacturing. Japan and South Korea contribute significantly through high adoption of technologically advanced and premium appliances. The region’s growth is further driven by the expansion of e-commerce platforms, increasing penetration of modern retail, and the rising popularity of wellness-focused lifestyles.

North America

North America holds approximately 28% of the global market share, with the United States being the primary contributor. The region’s growth is driven by high disposable incomes, strong consumer awareness regarding nutrition, and a well-established culture of health and fitness. The widespread popularity of cold-pressed juices and detox diets has significantly boosted demand for premium juicers, particularly masticating models. Additionally, the presence of leading appliance manufacturers and continuous product innovation contributes to market expansion. Canada also shows steady growth, supported by similar consumer trends and increasing adoption of smart kitchen appliances.

Europe

Europe accounts for around 22% of the global juicer market, with Germany, the United Kingdom, and France being key markets. Growth in this region is primarily driven by strong consumer preference for sustainable and energy-efficient products. European consumers are highly conscious of environmental impact, prompting manufacturers to focus on eco-friendly materials and energy-saving technologies. The region also benefits from a mature retail infrastructure and high penetration of premium appliances. Additionally, increasing interest in organic food consumption and home-based wellness practices is supporting steady demand for juicers.

Latin America

Latin America is an emerging market, led by Brazil and Mexico, where growing urbanization and improving economic conditions are driving appliance adoption. The region’s growth is supported by increasing awareness of healthy lifestyles and the rising popularity of fresh juice consumption. However, affordability remains a key factor influencing purchasing decisions, leading to higher demand for mid-range and entry-level products. The expansion of retail networks and the gradual growth of e-commerce platforms are also contributing to market development in this region.

Middle East & Africa

The Middle East & Africa region is experiencing gradual growth, with the UAE and South Africa emerging as key markets. Growth drivers include rising disposable incomes, expanding hospitality and tourism sectors, and increasing adoption of premium lifestyle products. The strong presence of hotels, restaurants, and cafes in the Middle East is driving demand for commercial juicers, while urbanization and improving living standards in Africa are supporting residential adoption. Additionally, government investments in infrastructure and retail development are enhancing market accessibility, further contributing to regional growth.