Jewelry Box Market Size

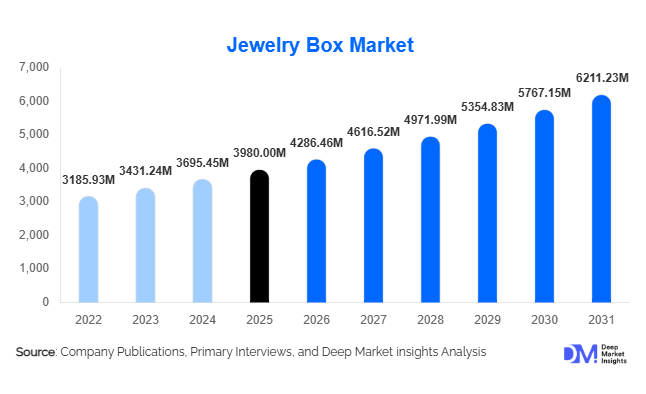

According to Deep Market Insights, the global jewelry box market size was valued at USD 3,980 million in 2025 and is projected to grow from USD 4,286.46 million in 2026 to reach USD 6,211.23 million by 2031, expanding at a CAGR of 7.7% during the forecast period (2026–2031). Market growth is primarily driven by rising global jewelry ownership, increasing demand for premium gifting products, and growing consumer interest in organized living and decorative storage solutions. Jewelry boxes are evolving beyond functional storage items into lifestyle and décor accessories, supported by premiumization trends and expanding e-commerce distribution channels worldwide.

Key Market Insights

- Premium and personalized jewelry storage solutions are gaining popularity, driven by rising luxury jewelry purchases and gifting culture worldwide.

- Online retail channels dominate market expansion, enabling global reach for niche brands and customized product offerings.

- Asia-Pacific leads global demand, supported by strong jewelry consumption in China and India and expanding middle-class income levels.

- Sustainable materials adoption is accelerating, particularly in Europe and North America where eco-conscious purchasing behavior is increasing.

- Travel-friendly and portable jewelry boxes are witnessing strong adoption, aligned with mobile lifestyles and frequent travel trends.

- Technology integration, including smart locks, LED lighting, and anti-tarnish protection, is redefining premium product innovation.

What are the latest trends in the jewelry box market?

Premiumization and Design-Led Product Innovation

Jewelry boxes are increasingly positioned as lifestyle accessories rather than simple storage products. Consumers are prioritizing craftsmanship, aesthetic appeal, and personalization features such as engraved surfaces, modular compartments, and luxury finishes. High-end wooden and leather-based designs are witnessing strong growth as consumers seek storage solutions that complement interior décor. Luxury brands are also introducing branded jewelry storage to enhance post-purchase customer experience, strengthening brand loyalty and increasing repeat purchases.

Sustainable and Eco-Friendly Materials Adoption

Sustainability has emerged as a defining trend across the jewelry box industry. Manufacturers are increasingly incorporating bamboo, recycled materials, FSC-certified wood, and vegan leather alternatives into product designs. Eco-friendly packaging and reduced plastic usage are becoming competitive differentiators, particularly in European markets. Consumers are demonstrating willingness to pay premium prices for environmentally responsible products, encouraging companies to redesign supply chains and sourcing strategies to meet sustainability expectations.

What are the key drivers in the jewelry box market?

Rising Global Jewelry Ownership

Growth in global jewelry consumption directly influences jewelry box demand. Increasing disposable incomes, expanding middle-class populations, and cultural purchasing traditions are encouraging higher jewelry ownership worldwide. As collections expand, consumers increasingly require structured storage solutions that protect valuables from damage and tarnishing. This structural linkage between jewelry sales and storage demand continues to drive steady market expansion.

Expansion of Gifting Culture

Jewelry boxes are widely purchased during weddings, festivals, anniversaries, and corporate gifting occasions. Emerging economies such as India and Southeast Asian countries contribute significantly due to strong cultural gifting traditions. Retailers increasingly bundle jewelry boxes with premium jewelry purchases, strengthening product visibility and expanding market penetration.

What are the restraints for the global market?

Price Competition from Low-Cost Manufacturers

The presence of low-cost, mass-produced jewelry boxes creates pricing pressure across mid-range segments. Unorganized manufacturing clusters, particularly in developing economies, offer inexpensive alternatives that limit premium brand pricing flexibility and compress profit margins.

Raw Material Price Volatility

Fluctuations in wood, leather, and metal prices impact manufacturing costs and pricing strategies. Premium product categories are especially sensitive to raw material cost changes since product value perception is closely tied to material quality and craftsmanship.

What are the key opportunities in the jewelry box industry?

Smart Jewelry Storage Solutions

The integration of technology into jewelry storage presents significant growth opportunities. Smart jewelry boxes featuring biometric locks, humidity control, LED lighting, and anti-tarnish linings are emerging as premium offerings targeting high-value jewelry owners. As jewelry collections increase in value, consumers are investing more in protective storage solutions, opening avenues for cross-industry innovation between electronics and lifestyle accessory manufacturers.

Sustainable Luxury Personalization

Customization combined with sustainability represents a major opportunity for market participants. Personalized designs, engraved branding, and eco-friendly materials allow manufacturers to command higher margins while appealing to environmentally conscious consumers. Direct-to-consumer business models further enable brands to scale personalized production efficiently.

Product Type Insights

The global jewelry box market demonstrates strong diversification across product categories, with standard jewelry boxes continuing to dominate demand due to their practicality, accessibility, and wide consumer acceptance. Standard jewelry boxes account for nearly 34% of total market share in 2025, supported by their affordability, versatile storage configurations, and suitability for everyday household use. The leading segment driver for this category is the growing emphasis on personal organization and jewelry protection among consumers, particularly as jewelry ownership expands across both developed and emerging economies. Manufacturers are increasingly introducing modular layouts, compact designs, and aesthetic finishes that align with modern home décor preferences, further strengthening adoption.Multi-compartment jewelry chests are gaining significant traction among consumers with expanding jewelry collections, particularly in premium and luxury segments. These products offer advanced storage functionality, enabling organized separation of rings, necklaces, earrings, and watches while minimizing damage and tangling. Rising disposable income levels and increased purchases of fine jewelry are encouraging consumers to invest in higher-capacity storage solutions.

Meanwhile, travel jewelry cases are witnessing accelerated growth driven by increasing global travel activity, business mobility, and demand for portable protective storage solutions. Lightweight construction, compact form factors, and anti-tarnish interiors are becoming key product differentiators.Smart jewelry boxes represent an emerging premium category integrating advanced technologies such as biometric locks, humidity control, LED lighting, and anti-theft systems. Their growth is primarily fueled by rising demand for secure storage among high-value jewelry owners and growing consumer interest in smart home accessories. Additionally, display-oriented jewelry boxes are expanding within retail and commercial environments, as jewelry brands increasingly prioritize visual merchandising and premium packaging experiences to enhance brand perception and customer engagement.

Material Type Insights

Material selection plays a critical role in shaping consumer purchasing behavior, influencing durability, aesthetics, and perceived product value. Wood-based jewelry boxes lead the global market with approximately 38% share of global revenue, supported by their premium appeal, structural strength, and compatibility with luxury interior design trends. The leading segment driver for wooden jewelry boxes is the strong consumer preference for long-lasting and aesthetically refined storage solutions that complement home décor while providing superior protection for valuable items. Handcrafted finishes and traditional craftsmanship further enhance demand in premium segments.Leather and faux leather jewelry boxes represent a significant share of the market, offering an attractive balance between luxury aesthetics and cost efficiency. These materials appeal particularly to urban consumers seeking modern styling combined with portability.

Plastic and acrylic jewelry boxes maintain consistent demand within entry-level and mass-market segments due to affordability, lightweight construction, and wide availability through online retail platforms. Their popularity is further supported by colorful and customizable designs targeting younger consumers.Sustainable materials, including bamboo, recycled wood composites, and eco-friendly fabrics, are experiencing rapid adoption as environmental awareness increases globally. Consumers are increasingly prioritizing sustainable lifestyle products, encouraging manufacturers to adopt environmentally responsible sourcing and production methods. Regulatory pressure and brand sustainability initiatives are expected to further accelerate innovation in biodegradable and recyclable jewelry storage materials over the forecast period.

Distribution Channel Insights

Distribution channels continue to evolve alongside shifting consumer purchasing habits, with online retail emerging as the dominant sales platform. Online channels account for around 36% of total market sales, driven by expanding e-commerce ecosystems, convenience, and broader product accessibility. The leading driver for this segment is the ability of digital platforms to offer extensive product variety, competitive pricing, customer reviews, and customization options, enabling informed purchasing decisions. Cross-border trade and direct-to-consumer brand strategies have further strengthened online market penetration.

Despite rapid digital expansion, offline retail channels remain highly relevant, particularly within premium product categories. Specialty gift stores and jewelry retailers continue to play an essential role by offering tactile product experiences, personalized recommendations, and premium packaging services that influence purchasing decisions. Department stores contribute significantly to seasonal and impulse-driven purchases, especially during festive occasions, weddings, and holiday gifting periods. Omnichannel retail strategies combining online discovery with offline purchasing experiences are increasingly shaping market competitiveness.

End-Use Insights

Individual consumers represent the largest end-use segment, contributing nearly 68% of global demand, reflecting growing personal jewelry ownership and rising awareness regarding jewelry maintenance and organization. The leading segment driver is the expansion of fashion consciousness and self-expression trends, encouraging consumers to invest in dedicated storage solutions that protect and showcase personal accessories. Increasing participation of younger demographics in jewelry consumption is further supporting sustained demand growth.Jewelry retailers are increasingly adopting branded jewelry boxes as part of premium packaging strategies aimed at enhancing customer experience and strengthening brand identity. Customized storage packaging not only improves product presentation but also contributes to brand recall and perceived product value. The hospitality industry is emerging as a niche yet growing application area, with luxury hotels and resorts incorporating jewelry organizers into premium guest accommodations to elevate customer experience standards.Corporate gifting represents another expanding application segment, supported by growing business promotional activities and festive gifting traditions across regions. Companies increasingly utilize customized jewelry boxes as premium gifting solutions for employees, partners, and clients, particularly during seasonal celebrations and marketing campaigns.

| By Product Type | By Material Type | By Distribution Channel | By End User |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America holds approximately 24% of the global jewelry box market share, supported by high consumer purchasing power and strong demand for premium lifestyle accessories. The United States remains the primary contributor, driven by well-established gifting culture, rising demand for home organization products, and increasing adoption of designer storage solutions. Regional growth is further supported by strong e-commerce infrastructure, high penetration of luxury jewelry ownership, and consumer preference for aesthetically refined home accessories. In Canada, expanding online retail adoption and growing awareness of product customization are contributing to steady market expansion. The increasing popularity of personalized gifting and sustainable product offerings is also encouraging innovation among regional manufacturers.

Europe

Europe accounts for nearly 22% of global demand, with Germany, France, Italy, and the United Kingdom serving as major revenue-generating markets. Regional growth is driven by strong appreciation for craftsmanship, heritage design, and premium-quality materials. Sustainability remains a key market driver, as environmentally conscious consumers increasingly prefer eco-friendly and responsibly sourced jewelry boxes. The region’s well-developed luxury goods sector further supports demand for high-end wooden and leather storage solutions. Additionally, rising interest in minimalist interior design trends and durable lifestyle products continues to influence purchasing behavior across European households.

Asia-Pacific

Asia-Pacific dominates the global jewelry box market with around 37% share in 2025, supported by expanding middle-class populations, rising disposable incomes, and strong cultural associations with jewelry ownership. China and India serve as the primary demand centers due to high jewelry consumption linked to weddings, festivals, and traditional gifting practices. Regional growth is driven by rapid urbanization, expanding e-commerce penetration, and increasing adoption of organized living solutions among younger consumers. India represents the fastest-growing market, fueled by wedding-driven jewelry purchases, growing gifting culture, and increasing awareness of jewelry preservation. Japan and South Korea contribute stable demand supported by preferences for compact, technologically advanced, and premium-quality storage products aligned with space-efficient lifestyles.

Latin America

Latin America accounts for approximately 9% of global demand, led by Brazil and Mexico. Regional market growth is supported by rising disposable income levels, expanding middle-class consumer bases, and increasing exposure to global lifestyle trends. Growth drivers include the development of organized retail channels, growing popularity of fashion accessories, and improved accessibility through online marketplaces. Urbanization and evolving gifting practices are encouraging consumers to adopt dedicated jewelry storage solutions, while local retailers are expanding product assortments to meet changing consumer preferences.

Middle East & Africa

The Middle East & Africa region is experiencing notable growth driven by strong luxury consumption patterns and high jewelry ownership rates, particularly in the United Arab Emirates and Saudi Arabia. Regional demand is supported by deep-rooted gifting traditions, premium lifestyle preferences, and increasing tourism-driven retail activity. Consumers in the Gulf countries demonstrate strong demand for luxury and customized jewelry storage solutions that reflect status and personalization. In Africa, South Africa represents an emerging growth market supported by expanding retail infrastructure, improving consumer spending capacity, and increasing penetration of international lifestyle brands. Rising urbanization and growing awareness of product organization solutions are expected to further strengthen regional market expansion.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Jewelry Box Market

- Wolf Designs Inc.

- Mele & Co.

- Pottery Barn

- LC Designs Co. Ltd. (Stackers)

- Songmics (VASAGLE)

- Umbra Ltd.

- Reed & Barton

- Hives & Honey

- Kendal & Hyde

- Glenor Co.

- Bey-Berk International

- Agresti Firenze

- Windrose (Sacher & Co.)

- Chasing Yachts Luxury Storage

- Trove Company