Jet Pack Market Size

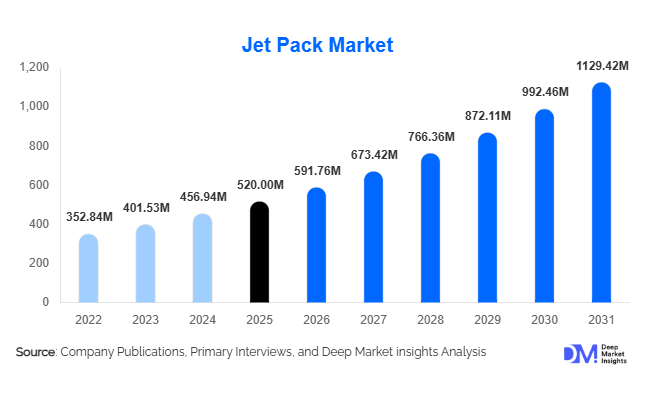

According to Deep Market Insights, the global jet pack market size was valued at USD 520 million in 2025 and is projected to grow from USD 591.76 million in 2026 to reach USD 1,129.42 million by 2031, expanding at a CAGR of 13.8% during the forecast period (2026–2031). The jet pack market growth is primarily driven by increasing defense investments in advanced mobility systems, rising demand for high-end recreational experiences, and rapid technological advancements in propulsion and lightweight materials.

Key Market Insights

- Defense and military applications dominate demand, with governments investing heavily in next-generation tactical mobility solutions.

- Water jet packs are leading commercialization, particularly in tourism-driven economies, due to affordability and ease of use.

- North America dominates the global market, driven by strong R&D capabilities and defense spending.

- Asia-Pacific is the fastest-growing region, supported by rising tourism and defense modernization initiatives.

- Electric and hybrid propulsion systems are gaining traction, driven by sustainability concerns and regulatory pressure.

- High costs and regulatory barriers remain key challenges, limiting widespread adoption beyond niche applications.

What are the latest trends in the jet pack market?

Shift Toward Electric and Hybrid Jet Packs

The jet pack industry is witnessing a transition toward electric and hybrid propulsion systems. Manufacturers are focusing on reducing carbon emissions and improving energy efficiency through advanced battery technologies and hybrid propulsion models. Electric jet packs offer quieter operation, lower maintenance, and reduced environmental impact, making them attractive for urban and commercial applications. As battery density improves, flight duration and payload capacity are expected to increase, enabling broader use cases.

Integration with Defense and Tactical Operations

Jet packs are increasingly being integrated into military operations for rapid deployment, reconnaissance, and special missions. Defense agencies are conducting trials to evaluate their effectiveness in complex terrains and urban warfare scenarios. This trend is supported by growing defense budgets and the need for innovative mobility solutions. Strategic collaborations between manufacturers and defense organizations are accelerating product development and deployment.

What are the key drivers in the jet pack market?

Rising Defense Expenditure

Global defense spending has significantly increased, with governments prioritizing advanced technologies for enhanced operational efficiency. Jet packs provide unique capabilities such as rapid troop mobility and access to hard-to-reach areas, making them valuable assets in modern warfare. This has resulted in increased procurement and R&D investments by defense agencies.

Growth in Adventure Tourism and Luxury Experiences

The demand for unique and high-end recreational activities is driving the adoption of jet packs, particularly water-based systems. Tourism operators are incorporating jet pack experiences into their offerings, attracting affluent consumers seeking novel adventure activities. Coastal regions and luxury tourism hubs are key markets for this segment.

What are the restraints for the global market?

High Cost of Ownership and Operation

Jet packs remain expensive due to complex engineering, high-performance materials, and limited production scale. Prices ranging from USD 100,000 to USD 400,000 restrict adoption to niche markets, including defense and high-net-worth individuals.

Regulatory and Safety Challenges

Strict aviation regulations, airspace restrictions, and safety concerns pose significant barriers to commercialization. Compliance with safety standards and obtaining operational approvals remain complex and time-consuming, limiting market expansion.

What are the key opportunities in the jet pack industry?

Expansion in Defense and Emergency Services

Jet packs present significant opportunities in defense and emergency response applications. Governments are increasingly investing in technologies that enable rapid deployment and efficient rescue operations. Jet packs can be used in disaster response, firefighting, and search-and-rescue missions, offering faster access to critical locations. This opens new revenue streams for manufacturers targeting institutional buyers.

Growth in Adventure Tourism Markets

The expansion of global tourism, particularly in emerging economies, provides strong growth opportunities for jet pack operators. Countries in Southeast Asia and the Middle East are investing in premium tourism experiences, creating demand for water jet packs and recreational services. Partnerships with resorts and tourism operators can further enhance market penetration.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 520 Million |

| Market Size in 2026 | USD 591.76 Million |

| Market Size in 2031 | USD 1129.42 Million |

| CAGR | 13.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Water jet packs continue to dominate the global jet pack market, accounting for approximately 38% of the total share in 2025. This leadership is primarily driven by their strong adoption in the recreational and tourism sectors, where ease of operation, relatively lower costs, and minimal regulatory constraints make them highly accessible. Coastal tourism hubs in regions such as Southeast Asia, the Middle East, and parts of Europe have significantly contributed to this segment’s expansion. In contrast, gas turbine jet packs are preferred in defense and professional applications due to their superior thrust-to-weight ratio, higher altitude capabilities, and suitability for tactical operations. Electric jet packs are emerging as a high-growth segment, supported by rapid advancements in battery energy density, reduced noise levels, and increasing environmental regulations. Hybrid jet packs are gaining traction as a transitional solution, combining fuel-based propulsion with electric efficiency, thereby improving flight duration and operational flexibility. The leading segment (water jet packs) is expected to maintain dominance due to scalability in tourism-driven markets and lower entry barriers compared to advanced propulsion systems.

Application Insights

Military and defense applications lead the jet pack market, accounting for approximately 32% of the total share in 2025. This dominance is driven by increasing global defense budgets and the need for advanced mobility solutions in complex terrains and rapid deployment scenarios. Jet packs offer strategic advantages such as vertical mobility, reduced dependence on traditional infrastructure, and enhanced mission flexibility, making them valuable for special operations forces. Recreational and sports applications represent the fastest-growing segment, fueled by rising global tourism, increasing disposable incomes, and demand for unique adventure experiences. Commercial applications, including emergency response, firefighting, and industrial inspections, are gaining momentum as organizations seek innovative solutions to improve operational efficiency and worker safety. Personal mobility remains an emerging segment, with potential growth linked to developments in urban air mobility (UAM) ecosystems. The continued dominance of defense applications is supported by consistent government funding, long procurement cycles, and high-value contracts.

Distribution Channel Insights

Direct sales dominate the jet pack market, accounting for nearly 60% of total revenue in 2025, primarily due to the nature of high-value transactions involving government contracts and enterprise-level procurement. Defense agencies and large commercial buyers typically engage directly with manufacturers for customized solutions, after-sales support, and long-term service agreements. Specialized dealers and distributors play a crucial role in expanding the reach of recreational and commercial jet packs, particularly in tourism-driven markets where localized expertise and training services are essential. Meanwhile, online and direct-to-consumer (D2C) channels are gradually gaining traction, especially for water jet packs and entry-level recreational models. Manufacturers are increasingly investing in digital platforms, virtual demonstrations, and direct marketing strategies to reach high-net-worth individuals and niche consumer segments. The dominance of direct sales is expected to persist due to the complexity, customization requirements, and regulatory considerations associated with jet pack systems.

End-User Insights

Government and defense agencies represent the largest end-user segment, holding approximately 40% of the global market share in 2025. This dominance is driven by sustained investments in advanced military technologies and the strategic importance of rapid mobility solutions in modern warfare. Defense organizations are not only procuring jet packs but also actively funding R&D initiatives to enhance performance, safety, and integration with existing military systems. Commercial enterprises, including tourism operators, industrial service providers, and emergency response organizations, are increasingly adopting jet packs for specialized applications such as offshore inspections, high-rise maintenance, and rescue operations. Individual consumers, particularly high-net-worth individuals and enthusiasts, contribute to demand in the recreational segment, although their share remains limited due to high acquisition and maintenance costs. The leadership of the government and defense segment is reinforced by high budget allocations, long-term contracts, and continuous technological advancements driven by military requirements.

Explore more data points, trends and opportunities Download Free Sample Report

Jet Pack Market Segmentations

By Product Type

- Water Jet Packs

- Gas Turbine Jet Packs

- Electric Jet Packs

- Hybrid Jet Packs

By Application

- Military & Defense Operations

- Recreational & Sports

- Commercial Applications

- Personal Mobility

By Distribution Channel

- Direct Sales

- Specialized Dealers & Distributors

- Online & Direct-to-Consumer Channels

By End-User

- Government & Defense Agencies

- Commercial Enterprises

- Individual Consumers

Regional Insights

North America

North America holds the largest share of the jet pack market, accounting for approximately 35% in 2025, with the United States representing the majority of regional demand. Growth in this region is primarily driven by high defense expenditure, the strong presence of leading manufacturers, and advanced R&D capabilities. The U.S. Department of Defense has been actively exploring jet pack applications for tactical mobility and special operations, significantly boosting demand. Additionally, the region benefits from a mature innovation ecosystem, availability of venture capital funding, and early adoption of emerging technologies. The recreational segment is also expanding, particularly in coastal states such as Florida and California, where tourism-driven demand for water jet packs is strong.

Europe

Europe accounts for approximately 25% of the global market, with key countries including the United Kingdom, Germany, and France. Regional growth is driven by defense modernization programs, increasing investments in advanced mobility technologies, and a strong focus on sustainability. European governments are actively supporting the development of electric and low-emission propulsion systems, aligning with broader environmental goals. The region also benefits from a well-established tourism industry, particularly in Southern Europe, where recreational jet pack activities are gaining popularity. Collaborative R&D initiatives and partnerships between aerospace companies and defense agencies further support market expansion.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the jet pack market, with a projected CAGR exceeding 16%. China, Japan, and Australia are key contributors, driven by rising defense budgets, technological advancements, and expanding tourism sectors. China is heavily investing in next-generation mobility technologies as part of its broader industrial strategy, while Japan focuses on innovation and robotics integration. Southeast Asia, including countries such as Thailand and Indonesia, is emerging as a major hub for recreational jet pack activities due to booming tourism infrastructure and increasing international visitor inflows. Growing middle-class income levels and government support for tourism development are key drivers of regional growth.

Latin America

Latin America holds a smaller share of approximately 8% in 2025, with Brazil and Mexico leading the market. Growth in this region is primarily driven by recreational applications, particularly in coastal and resort areas with strong tourism activity. Increasing investments in tourism infrastructure and rising interest in adventure sports are supporting demand for water jet packs. However, limited defense spending and economic constraints restrict large-scale adoption in military applications. The market is expected to grow steadily as tourism continues to recover and expand across the region.

Middle East & Africa

The Middle East & Africa region accounts for around 10% of the global market, with the UAE and Saudi Arabia emerging as key growth hubs. The region’s growth is driven by luxury tourism, government-led innovation initiatives, and economic diversification strategies aimed at reducing dependence on oil revenues. Countries such as the UAE are investing heavily in futuristic mobility solutions and experiential tourism, creating strong demand for both recreational and advanced jet pack systems. Additionally, high disposable incomes and a preference for premium experiences support the adoption of jet packs in the tourism sector. In Africa, growth is more limited but gradually increasing, particularly in tourism-focused economies.

Key Players in the Jet Pack Market

- Gravity Industries

- JetPack Aviation

- Zapata Company

- Martin Aircraft Company

- JetLev Technologies

- Flyboard Air

- Aeromen Technologies

- SkyRunner

- FusionFlight

- Mayman Aerospace

- Hoversurf

- Volans

- Malloy Aeronautics

- Urban Aeronautics

- LIFT Aircraft