Intraocular Lens Market Size

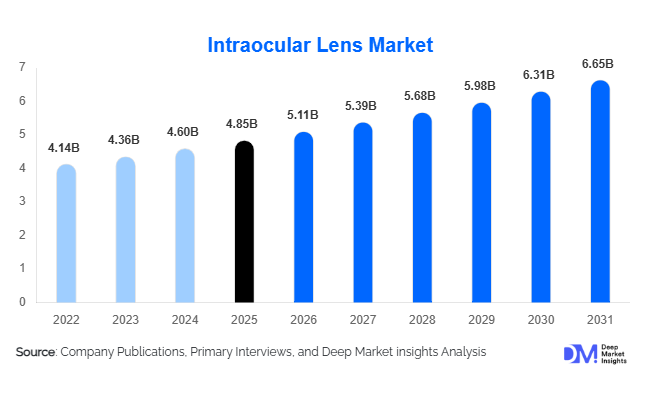

According to Deep Market Insights, the global intraocular lens market size was valued at USD 4.85 billion in 2025 and is projected to grow from USD 5.11 billion in 2026 to reach USD 6.65 billion by 2031, expanding at a CAGR of 5.4% during the forecast period (2026–2031). The intraocular lens market growth is primarily driven by the increasing prevalence of cataracts, rising aging population worldwide, the growing demand for premium vision correction procedures, and rapid advancements in ophthalmic surgical technologies. Expanding healthcare access across emerging economies and rising adoption of minimally invasive cataract surgeries are further strengthening global demand for advanced intraocular lens (IOL) implants.

Key Market Insights

- Premium intraocular lenses are rapidly gaining adoption, particularly multifocal, trifocal, toric, and extended depth-of-focus (EDOF) lenses that reduce dependency on corrective eyewear.

- Hydrophobic acrylic lenses dominate the market due to superior biocompatibility, lower complication risks, and increasing preference for foldable implants.

- North America dominates the global intraocular lens market, supported by advanced ophthalmic infrastructure, strong reimbursement systems, and high premium lens penetration.

- Asia-Pacific is the fastest-growing region, driven by rising cataract surgery volumes, expanding healthcare investments, and increasing medical tourism in China and India.

- Technological advancements in digital ophthalmology, including AI-assisted surgical planning and femtosecond laser-assisted cataract surgery, are improving procedural precision and patient outcomes.

- Government blindness prevention initiatives across emerging economies are accelerating cataract treatment accessibility and supporting long-term intraocular lens market growth.

Intraocular Lens Market Trends

Growing Shift Toward Premium and Customized Vision Correction

The intraocular lens industry is witnessing a major transition toward premium and personalized vision correction technologies. Patients increasingly seek spectacle independence following cataract surgery, resulting in rising adoption of multifocal, trifocal, toric, and extended depth-of-focus lenses. Premium intraocular lenses provide improved near, intermediate, and distance vision compared with traditional monofocal implants, making them highly attractive in developed healthcare markets. Manufacturers are focusing on advanced optical engineering, customized lens designs, and enhanced contrast sensitivity to improve patient satisfaction and reduce postoperative visual disturbances. Light-adjustable lenses and wavefront-guided technologies are also emerging as next-generation solutions capable of delivering highly individualized refractive outcomes. This premiumization trend is significantly improving profitability across the ophthalmic device industry.

Digitalization and AI Integration in Ophthalmic Surgery

Advanced digital technologies are increasingly transforming cataract surgery workflows and intraocular lens implantation procedures. AI-assisted diagnostics, intraoperative aberrometry, digital imaging systems, and predictive analytics are enabling surgeons to achieve highly precise refractive outcomes. Femtosecond laser-assisted cataract surgeries are gaining wider adoption due to improved incision accuracy, reduced surgical variability, and faster patient recovery times. Manufacturers are integrating software ecosystems with premium IOL portfolios to strengthen surgeon engagement and optimize procedural planning. Digital surgical guidance platforms are also enhancing patient education and preoperative decision-making by enabling visualization of postoperative vision outcomes. These technological advancements are expected to further accelerate adoption of premium intraocular lenses globally.

Intraocular Lens Market Drivers

Rapidly Aging Global Population

The increasing elderly population worldwide is one of the primary drivers supporting intraocular lens market growth. Cataracts are strongly age-associated, and the growing number of individuals above 60 years of age is significantly increasing cataract surgery volumes globally. Countries such as Japan, Germany, Italy, China, and the United States are experiencing substantial demographic aging, which directly contributes to higher demand for ophthalmic procedures. Cataract surgery remains among the most commonly performed surgical procedures globally, ensuring stable long-term demand for intraocular lenses. Governments and healthcare systems are prioritizing cataract treatment programs to reduce preventable blindness and improve quality of life among aging populations.

Increasing Adoption of Premium Intraocular Lenses

Demand for premium intraocular lenses continues to rise due to growing patient preference for enhanced postoperative visual outcomes. Multifocal, trifocal, toric, and EDOF lenses are increasingly preferred because they reduce dependence on glasses after surgery while improving visual acuity across multiple focal ranges. Rising disposable incomes and growing awareness regarding advanced ophthalmic procedures are further supporting adoption of premium IOL technologies. Hospitals and ophthalmic clinics also benefit from higher procedural margins associated with premium lens implantation, encouraging wider clinical acceptance. This trend is particularly strong in North America, Europe, Japan, and urban healthcare centers across Asia-Pacific.

Intraocular Lens Market Restraints

High Cost of Premium Lens Technologies

One of the key restraints impacting market expansion is the high cost associated with premium intraocular lenses. Multifocal and toric lenses remain significantly more expensive than conventional monofocal implants, limiting accessibility in price-sensitive markets. In several countries, insurance reimbursement covers only standard cataract surgery procedures, forcing patients to pay additional out-of-pocket expenses for premium lens upgrades. This affordability challenge continues to restrict adoption rates across developing economies despite growing clinical awareness and demand.

Postoperative Visual Complications and Patient Adaptation Issues

Advanced intraocular lenses may sometimes cause postoperative complications such as glare, halos, reduced contrast sensitivity, or difficulties adapting to multifocal optics. These challenges can impact patient satisfaction and create hesitation among surgeons regarding broader premium lens adoption. Inadequate patient selection and limited surgeon training in emerging markets can further increase risks of suboptimal outcomes. Regulatory approval requirements for innovative implant technologies also increase commercialization timelines and development costs for manufacturers operating within the global intraocular lens market.

Intraocular Lens Market Opportunities

Expansion of Cataract Surgery Programs in Emerging Economies

Emerging economies present significant opportunities for intraocular lens manufacturers due to increasing healthcare investments and blindness prevention initiatives. Countries including India, China, Indonesia, Brazil, and several African nations are expanding cataract treatment accessibility through public healthcare programs and mobile surgical units. Rising healthcare infrastructure development and increasing ophthalmologist availability are expected to accelerate procedural volumes substantially over the forecast period. Medical tourism growth in countries such as India, Thailand, Turkey, and the UAE is also creating opportunities for advanced ophthalmic care providers and premium IOL manufacturers.

Development of Adjustable and Smart Intraocular Lenses

The emergence of adjustable and technologically advanced intraocular lenses offers substantial long-term growth opportunities. Light-adjustable lenses, accommodative implants, and AI-optimized personalized optics are gaining industry attention due to their ability to deliver customized postoperative vision correction. Manufacturers investing in research and development of smart ophthalmic implants are expected to gain competitive advantages as patient demand increasingly shifts toward personalized healthcare solutions. Future innovations integrating digital diagnostics with adaptive lens technologies could redefine premium ophthalmic surgery and create high-margin growth opportunities across developed markets.

Product Type Insights

Monofocal intraocular lenses continue to dominate the global market in terms of procedural volume due to their affordability and widespread reimbursement coverage across public healthcare systems. However, premium lens categories such as multifocal, trifocal, toric, and EDOF lenses are experiencing the fastest revenue growth due to increasing patient preference for spectacle independence and improved visual quality. Multifocal lenses account for a significant share of premium segment revenues because of their ability to provide near and distance vision correction simultaneously. Toric intraocular lenses are also witnessing strong adoption as the prevalence of astigmatism correction procedures increases globally. Accommodative and adjustable intraocular lenses remain relatively niche but are gaining traction in developed markets due to ongoing advancements in customized vision technologies.

Material Insights

Hydrophobic acrylic intraocular lenses dominate the market owing to their superior optical clarity, foldability, and low posterior capsule opacification rates. These lenses are widely preferred by surgeons because they allow minimally invasive implantation through smaller incisions while ensuring excellent long-term stability. Hydrophilic acrylic lenses maintain stable demand in cost-sensitive markets due to lower manufacturing costs and broad accessibility. Silicone intraocular lenses continue to be used selectively in specialized applications, although their adoption remains lower compared with acrylic variants. PMMA lenses are gradually declining in popularity because of their rigid structure and requirement for larger surgical incisions, though they continue to serve lower-income healthcare systems in select regions.

Application Insights

Cataract surgery remains the dominant application segment within the intraocular lens market, accounting for the vast majority of implant procedures globally. Rising incidence of age-related cataracts and increasing surgical accessibility continue to support strong procedural growth. Refractive lens exchange procedures are expanding steadily, particularly among middle-aged patients seeking permanent vision correction alternatives to LASIK surgery. Presbyopia and astigmatism correction applications are also contributing significantly to premium lens demand, particularly for toric and multifocal implants. Pediatric ophthalmic applications remain comparatively niche but represent an important specialty segment requiring customized intraocular lens solutions for congenital cataract treatment.

End-Use Insights

Hospitals account for the largest share of the intraocular lens market due to high cataract surgery volumes, advanced ophthalmic infrastructure, and strong reimbursement support. Large tertiary care hospitals and ophthalmic specialty centers continue to dominate premium lens implantation procedures globally. Ambulatory surgery centers (ASCs) are emerging as the fastest-growing end-use segment, particularly in North America and Europe, due to their ability to offer cost-efficient same-day cataract surgeries with reduced operational expenses. Ophthalmology clinics are also experiencing strong growth across Asia-Pacific and the Middle East as private healthcare investments increase and medical tourism expands. Academic and research institutions continue to support innovation in advanced intraocular lens technologies and surgical techniques.

Distribution Channel Insights

Direct sales channels dominate the intraocular lens market as manufacturers increasingly engage directly with hospitals, ophthalmology clinics, and surgical centers to strengthen surgeon relationships and provide procedural training support. Medical device distributors continue to play a critical role in expanding access across emerging economies and smaller healthcare facilities. Group purchasing organizations (GPOs) are becoming increasingly important in developed markets by enabling hospitals to negotiate competitive procurement contracts. Digital procurement platforms and institutional e-tender systems are also gaining popularity as healthcare systems modernize purchasing operations and prioritize transparent pricing models for ophthalmic implants.

| By Product Type | By Material | By Application | By End User | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America remains the largest regional market for intraocular lenses, accounting for approximately 36% of global revenues in 2025. The United States dominates regional demand due to advanced ophthalmic healthcare infrastructure, high cataract surgery volumes, favorable reimbursement systems, and strong adoption of premium lens technologies. Patients in the U.S. increasingly prefer multifocal and toric intraocular lenses to achieve spectacle independence following cataract procedures. Canada also demonstrates stable growth supported by aging demographics and expanding access to advanced ophthalmic care. The region remains highly attractive for premium intraocular lens manufacturers due to high healthcare spending and strong surgeon adoption of digital ophthalmic technologies.

Europe

Europe represents the second-largest regional market, supported by strong healthcare systems and increasing demand for advanced refractive cataract procedures. Germany, France, the United Kingdom, Italy, and Spain account for the majority of regional demand. Germany remains a leading market due to its advanced ophthalmic device manufacturing ecosystem and high procedural standards. European healthcare providers are increasingly adopting premium trifocal and toric lenses as patient awareness regarding advanced vision correction solutions rises. Growing elderly populations and expanding elective cataract procedures continue to strengthen market growth across Western Europe.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, driven by rapidly increasing cataract surgery volumes, healthcare infrastructure expansion, and rising disposable incomes. China represents one of the largest growth engines globally due to healthcare modernization initiatives, increasing ophthalmologist availability, and expanding access to premium ophthalmic procedures. India is also emerging as a major market due to rising medical tourism, growing private ophthalmology chains, and national blindness prevention programs. Japan continues to maintain high procedural volumes because of its aging population and technologically advanced healthcare system. South Korea and Southeast Asian countries are also witnessing increasing demand for premium intraocular lenses and minimally invasive cataract surgeries.

Latin America

Latin America accounts for a smaller but steadily expanding share of the global intraocular lens market. Brazil and Mexico dominate regional demand due to increasing private healthcare investments and improving ophthalmic infrastructure. Rising awareness regarding cataract treatment and expanding access to ophthalmic surgeries are supporting market growth. Premium intraocular lens adoption remains comparatively lower than developed markets but is gradually increasing among urban middle-class populations seeking advanced refractive correction procedures.

Middle East & Africa

The Middle East & Africa region is witnessing growing demand for intraocular lenses due to healthcare modernization and increasing ophthalmic investments. Saudi Arabia and the UAE are investing heavily in advanced medical infrastructure and premium eye care services as part of broader healthcare diversification initiatives. South Africa remains one of the leading ophthalmic markets in sub-Saharan Africa due to relatively advanced healthcare infrastructure. Government-supported blindness prevention initiatives across Africa are expected to improve cataract treatment accessibility and support long-term intraocular lens market expansion.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Intraocular Lens Market

- Alcon

- Johnson & Johnson Vision

- Bausch + Lomb

- HOYA Corporation

- Carl Zeiss Meditec

- STAAR Surgical

- Rayner

- Lenstec

- HumanOptics

- Ophtec

- SIFI

- Aurolab

- PhysIOL

- NIDEK

- Biotech Vision Care