Insulated Products Market Size

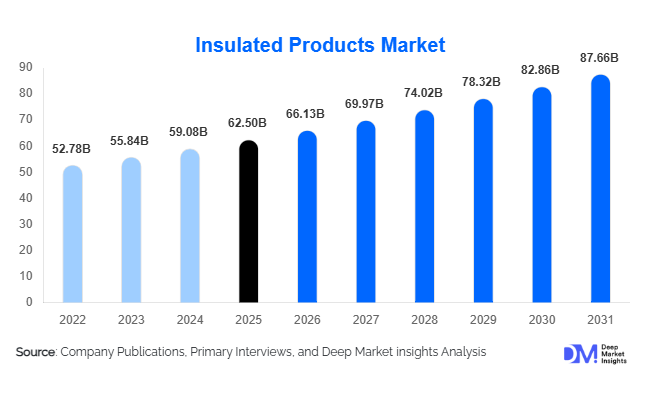

According to Deep Market Insights, the global insulated products market size was valued at USD 62.5 billion in 2025 and is projected to grow from USD 66.13 billion in 2026 to reach USD 87.66 billion by 2031, expanding at a CAGR of 5.8% during the forecast period (2026–2031). The insulated products market growth is primarily driven by rising investments in energy-efficient buildings, increasing demand for industrial thermal management solutions, and growing adoption of advanced insulation materials across construction, transportation, and manufacturing sectors.

Insulated products play a crucial role in reducing heat transfer, improving energy efficiency, and enhancing acoustic and fire protection across buildings, industrial equipment, pipelines, and transportation systems. Increasing global focus on sustainability and carbon emission reduction has significantly accelerated demand for high-performance insulation materials such as mineral wool, polyurethane foam, and advanced aerogel insulation solutions.

Rapid urbanization across emerging economies, combined with strict building energy regulations in developed countries, is driving large-scale adoption of insulation products in both new construction and renovation projects. Additionally, expanding industrial sectors including petrochemicals, power generation, and manufacturing are increasing demand for high-temperature insulation solutions. The growth of cold-chain logistics, electric vehicles, and advanced transportation infrastructure is also creating new application areas for insulation technologies, positioning the market for steady long-term growth.

Key Market Insights

- Energy efficiency regulations and green building initiatives are accelerating insulation adoption across residential, commercial, and industrial construction sectors.

- Thermal insulation products dominate global demand, driven by widespread use in building envelopes, HVAC systems, and industrial process equipment.

- Asia-Pacific leads the global market due to large-scale construction activities and rapid industrialization in China, India, and Southeast Asia.

- Advanced insulation materials such as aerogels and vacuum-insulated panels are gaining traction in high-performance applications, including aerospace and electric vehicles.

- Industrial insulation demand is expanding in sectors such as petrochemicals, power generation, and steel manufacturing.

- Growing investments in cold-chain infrastructure are boosting demand for insulation products used in refrigerated transport and storage systems.

What are the latest trends in the insulated products market?

Growing Adoption of Sustainable Insulation Materials

Sustainability has become a central focus for insulation manufacturers and construction companies worldwide. Governments and regulatory agencies are encouraging the use of environmentally friendly insulation materials that minimize carbon emissions and improve energy efficiency. As a result, manufacturers are increasingly developing products made from recycled or bio-based materials such as cellulose insulation and natural fiber composites. Mineral wool insulation, produced from natural rock and recycled materials, is gaining popularity due to its excellent fire resistance and sustainability profile.

In addition, building developers are prioritizing insulation products with low environmental impact to comply with green building certifications such as LEED and BREEAM. This shift toward sustainable construction practices is expected to drive significant innovation within the insulation materials industry.

Advanced High-Performance Insulation Technologies

Technological innovation is transforming the insulated products market through the development of advanced materials with superior thermal performance. Aerogel insulation, vacuum-insulated panels (VIPs), and microporous insulation materials offer significantly higher thermal resistance compared to traditional insulation products. These technologies are increasingly used in applications where space efficiency and lightweight design are critical.

Industries such as aerospace, automotive, and electronics are adopting high-performance insulation solutions to improve thermal management and operational efficiency. For example, electric vehicle manufacturers are integrating advanced insulation materials to regulate battery temperature and improve energy efficiency. This trend is expected to accelerate the adoption of innovative insulation products across multiple industrial sectors.

What are the key drivers in the insulated products market?

Increasing Global Focus on Energy Efficiency

Energy efficiency remains one of the primary drivers of the insulated products market. Insulation significantly reduces heat transfer between indoor and outdoor environments, enabling buildings and industrial facilities to maintain stable temperatures with lower energy consumption. Governments worldwide are implementing stricter energy performance standards for buildings, encouraging the adoption of advanced insulation materials in residential and commercial construction.

Energy-efficient buildings not only reduce carbon emissions but also lower operational costs for property owners. As global energy prices continue to rise, building developers and facility managers are increasingly investing in insulation upgrades to improve energy performance.

Expansion of the Global Construction Industry

The rapid growth of the global construction industry is another major factor driving demand for insulation products. Urbanization, population growth, and infrastructure development are fueling large-scale construction projects across emerging economies. Residential housing developments, commercial complexes, airports, and industrial facilities all require insulation systems to improve thermal efficiency and acoustic performance.

Countries such as China, India, and Indonesia are investing heavily in housing and urban infrastructure, which is significantly boosting demand for insulation materials used in walls, roofs, and floors.

What are the restraints for the global market?

Volatility in Raw Material Prices

The insulated products industry relies heavily on petrochemical derivatives and mineral resources for manufacturing insulation materials. Fluctuations in crude oil prices directly affect the cost of plastic foam insulation materials such as polyurethane and polystyrene. These price fluctuations can create uncertainty for manufacturers and increase production costs, affecting profitability and pricing strategies.

Environmental and Disposal Concerns

Some insulation materials pose environmental challenges related to recyclability and waste management. Plastic-based insulation materials can be difficult to recycle and may contribute to environmental pollution if not properly disposed of. Increasing regulatory scrutiny regarding chemical additives and flame retardants used in insulation materials is also creating compliance challenges for manufacturers.

What are the key opportunities in the insulated products industry?

Rapid Infrastructure Development in Emerging Economies

Emerging economies across Asia, the Middle East, and Latin America are investing heavily in infrastructure development. Projects such as smart cities, transportation networks, and industrial manufacturing facilities require large volumes of insulation materials. These infrastructure investments present significant opportunities for insulation manufacturers to expand their presence in rapidly growing markets.

Expansion of Cold Chain and Refrigeration Infrastructure

The rapid expansion of global food supply chains and pharmaceutical logistics is creating strong demand for cold-chain infrastructure. Refrigerated warehouses, cold storage facilities, and temperature-controlled transportation systems require high-performance insulation products to maintain stable temperatures. As global demand for frozen foods, vaccines, and temperature-sensitive pharmaceuticals increases, the need for advanced insulation materials in cold-chain applications is expected to rise significantly.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 62.5 Billion |

| Market Size in 2026 | USD 66.13 Billion |

| Market Size in 2031 | USD 87.66 Billion |

| CAGR | 5.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Rigid insulation boards and panels dominate the insulated products market due to their extensive use in building construction and industrial insulation systems. These products offer excellent thermal resistance, high compressive strength, and easy installation, making them suitable for large-scale infrastructure projects. Insulation rolls and batts are widely used in residential buildings for wall and attic insulation, providing cost-effective solutions for improving indoor temperature regulation. Spray foam insulation is gaining popularity due to its ability to fill irregular spaces and provide airtight insulation, making it highly effective for energy-efficient building applications.

Application Insights

Building envelope insulation represents the largest application segment, driven by the need to reduce heating and cooling energy consumption in residential and commercial buildings. HVAC system insulation is another major application area, ensuring efficient temperature control and reducing energy losses in heating and cooling systems. Industrial insulation is widely used in power plants, chemical processing facilities, and manufacturing plants to maintain process temperatures and improve operational efficiency. Transportation insulation is also gaining importance, particularly in electric vehicles and aerospace applications, where thermal management is critical for safety and performance.

Distribution Channel Insights

Direct sales to construction contractors and industrial OEMs dominate the insulated products distribution landscape, as large projects require consistent supply and technical support from manufacturers. Distributor networks play an important role in supplying insulation materials to smaller construction companies and regional contractors. Online procurement platforms are gradually emerging as alternative distribution channels, enabling buyers to compare product specifications and pricing across multiple suppliers. Digital procurement systems are increasingly being adopted by construction firms to streamline purchasing processes and reduce supply chain inefficiencies.

End-Use Industry Insights

The building and construction industry represents the largest consumer of insulation products globally, accounting for a significant portion of market demand. Residential and commercial construction projects require insulation systems to improve energy efficiency and indoor comfort. The industrial manufacturing sector also represents a major end-use segment, particularly in energy-intensive industries such as petrochemicals, steel production, and power generation. Transportation industries, including automotive, aerospace, and railways, are increasingly adopting insulation materials to enhance passenger comfort and improve thermal management. Additionally, the expansion of cold-chain logistics and refrigeration systems is creating new opportunities for insulation product manufacturers.

Explore more data points, trends and opportunities Download Free Sample Report

Insulated Products Market Segmentations

By Insulation Type

- Thermal Insulation

- Acoustic Insulation

- Electrical Insulation

By Material Type

- Mineral Wool

- Plastic Foam Insulation

- Elastomeric Foam

- Aerogel Insulation Materials

- Cellulose Insulation

- Calcium Silicate Insulation

- Microporous Insulation

By Application

- Building Envelope Insulation

- HVAC System Insulation

- Industrial Equipment Insulation

- Pipe and Tank Insulation

- Transportation Insulation

- Electrical and Electronics Insulation

By End-Use Industry

- Building & Construction

- Industrial Manufacturing

- Transportation

- Oil & Gas

- Appliances & Consumer Goods

- Cold Chain & Refrigeration

By Distribution Channel

- Direct OEM Sales

- Distributor / Contractor Networks

- Online Industrial Procurement Platforms

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global insulated products market, accounting for approximately 40% of the total market share. China represents the largest market in the region due to its extensive construction activities and strong industrial base. Government initiatives aimed at improving building energy efficiency are further boosting insulation demand. India is emerging as one of the fastest-growing markets, driven by rapid urbanization, infrastructure development, and increasing housing demand. Japan and South Korea also contribute significantly to regional demand due to their advanced manufacturing sectors and strict energy efficiency regulations.

North America

North America holds approximately 25% of the global insulated products market. The United States is the dominant market in the region, supported by strict building energy codes and strong adoption of insulation in residential construction. Retrofitting older buildings with modern insulation systems is a major growth driver. Canada also represents an important market due to its cold climate conditions, which require extensive building insulation to maintain indoor temperature stability.

Europe

Europe accounts for nearly 23% of global insulation demand, driven by strong regulatory frameworks aimed at reducing carbon emissions from buildings. Countries such as Germany, France, the United Kingdom, and Italy are investing heavily in energy-efficient building renovation projects. Industrial insulation demand is also strong in Europe due to the region’s large manufacturing sector.

Latin America

Latin America represents a smaller share of the insulated products market but is gradually expanding due to infrastructure development and industrial growth. Brazil and Mexico are the largest markets in the region, driven by construction activity and growing manufacturing sectors.

Middle East & Africa

The Middle East and Africa region is experiencing increasing demand for insulation materials due to rapid infrastructure development and extreme climate conditions. Countries such as the United Arab Emirates and Saudi Arabia require high-performance thermal insulation to improve energy efficiency in buildings and industrial facilities.

Key Players in the Insulated Products Market

- Saint-Gobain

- Owens Corning

- Rockwool International

- Kingspan Group

- BASF

- Johns Manville

- Knauf Insulation

- Armacell International

- Aspen Aerogels

- Morgan Advanced Materials

- Dow

- Paroc Group

- Autex Industries

- Promat (Etex Group)

- Superglass Insulation