Hypoallergenic Pet Foods Market Size

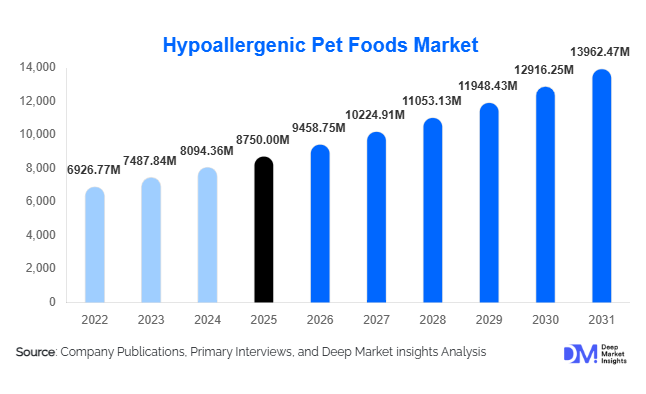

According to Deep Market Insights, the global hypoallergenic pet foods market size was valued at USD 8,750 million in 2025 and is projected to grow from USD 9,458.75 million in 2026 to reach USD 13,962.47 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The hypoallergenic pet foods market growth is primarily driven by rising incidences of food allergies and dermatological conditions in pets, increasing pet humanization trends, and strong premiumization across global pet care spending.

Growing veterinary awareness, higher adoption of prescription-based diets, and expanding e-commerce distribution are accelerating global demand. Dogs account for the largest consumption share due to higher allergy diagnosis rates, while hypoallergenic cat food is steadily gaining traction. North America currently dominates market revenue, while Asia-Pacific is emerging as the fastest-growing region, supported by urban pet adoption and rising disposable incomes.

Key Market Insights

- Dogs account for nearly 65% of total revenue, driven by higher allergy diagnosis rates and greater per-pet expenditure.

- Limited ingredient diets (LID) lead the ingredient segment, contributing approximately 32% of the 2025 market.

- Dry hypoallergenic food dominates with nearly 48% share due to cost efficiency and longer shelf life.

- North America holds approximately 38% of global revenue, supported by strong veterinary penetration and pet insurance adoption.

- Asia-Pacific is the fastest-growing region, expanding at nearly 10% CAGR through 2031.

- The top five players collectively account for about 52% ofthe global market share, indicating moderate consolidation.

What are the latest trends in the hypoallergenic pet foods market?

Shift Toward Novel and Alternative Proteins

Pet owners are increasingly demanding novel protein sources such as venison, duck, rabbit, salmon, and insect protein to reduce allergenic reactions. Insect-based protein, in particular, is gaining regulatory acceptance in Europe and North America, offering both hypoallergenic and sustainability advantages. This trend reduces reliance on traditional chicken and beef proteins, which are commonly associated with food intolerances. Manufacturers are investing in alternative protein processing facilities to ensure traceability, digestibility, and compliance with labeling standards.

Growth of Personalized and Prescription Nutrition

Integration of veterinary diagnostics with dietary recommendations is reshaping the hypoallergenic pet foods landscape. Hydrolyzed protein diets, typically prescribed for elimination trials, are expanding beyond clinical settings into premium retail channels. Digital subscription models now allow pet owners to receive customized diets aligned with veterinary assessments. This personalization trend improves customer retention and supports premium pricing models, with prescription diets generating gross margins between 18% and 25% globally.

What are the key drivers in the hypoallergenic pet foods market?

Rising Incidence of Pet Allergies

Approximately 10–15% of canine dermatological cases globally are linked to food-related allergies. Increased awareness among pet owners and veterinarians has significantly expanded demand for limited-ingredient and hydrolyzed protein diets. Growing access to veterinary care and pet insurance, particularly in North America and Europe, is further strengthening this driver.

Premiumization and Pet Humanization

Pets are increasingly viewed as family members, leading owners to invest in specialized nutrition. Super-premium and veterinary prescription diets account for nearly 38% of overall revenue. Consumers are seeking clean-label formulations free from artificial additives, soy, wheat, and corn, reinforcing long-term premium demand growth.

What are the restraints for the global market?

High Product Pricing

Hypoallergenic pet foods are typically 25–60% more expensive than standard pet food formulations due to specialized protein processing and clinical validation requirements. This price premium limits adoption in price-sensitive emerging markets.

Regulatory and Compliance Complexities

Strict labeling standards, hydrolyzed protein definitions, and veterinary claim regulations vary across regions. Compliance costs and ingredient traceability requirements increase operational complexity, particularly for smaller manufacturers entering international markets.

What are the key opportunities in the hypoallergenic pet foods industry?

Expansion in Emerging Urban Markets

Urban centers in China, India, Brazil, and Mexico are witnessing rapid growth in companion animal ownership. Penetration of hypoallergenic diets remains below 10% in many of these markets, presenting substantial headroom for premium product expansion. Government support for domestic pet food manufacturing in countries such as India and Brazil is also strengthening supply-side economics.

Sustainable and Functional Ingredient Innovation

Sustainability-driven consumers are encouraging brands to invest in plant-based, insect-based, and ethically sourced proteins. These innovations reduce exposure to volatile meat supply chains while aligning with environmental goals. Functional additions such as probiotics, omega fatty acids, and dermatology-support blends are further differentiating product portfolios.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8750 Million |

| Market Size in 2026 | USD 9458.75 Million |

| Market Size in 2031 | USD 13962.47 Million |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Limited Ingredient Diets (LID) represent the leading product type, contributing approximately 32% of the global hypoallergenic pet foods market in 2025. Their leadership is primarily driven by strong clean-label appeal, transparency in ingredient sourcing, and accessibility without mandatory veterinary prescriptions. Pet owners increasingly prefer simplified formulations with single animal protein sources and minimal additives, particularly for elimination diet trials and mild allergy management. The growing consumer shift toward “natural,” “grain-free,” and minimally processed pet nutrition has significantly strengthened this segment’s retail penetration across North America and Europe.

Hydrolyzed protein diets dominate the veterinary prescription sub-segment and command premium price points due to clinically validated allergen reduction benefits. These products are extensively recommended for severe dermatological and gastrointestinal allergies, particularly in dogs. Their growth is supported by rising veterinary diagnostics and increased pet insurance coverage, especially in developed markets.

Application Insights

Dogs remain the dominant application segment, accounting for approximately 65% of total global revenue in 2025. The segment’s leadership is driven by higher incidence rates of food allergies and dermatological disorders in dogs compared to cats. Additionally, per-pet spending is significantly higher in canine nutrition, particularly in developed markets such as the United States and Germany. Veterinary-prescribed elimination diets and hydrolyzed protein foods are predominantly recommended for dogs, reinforcing this segment’s revenue dominance.

Cats represent the second-largest segment and are steadily expanding due to increasing awareness of feline digestive sensitivities and protein intolerances. Indoor cat ownership growth, particularly in urban Asia-Pacific markets, is supporting demand for specialized formulations. Premium cat hypoallergenic diets are witnessing higher adoption among millennial pet owners seeking preventive health management solutions. Other companion animals, including small mammals and birds, form a niche but an emerging segment. Although currently representing a small revenue share, product diversification in this category is expected to expand as specialty pet ownership increases in developed urban markets.

Distribution Channel Insights

Pet specialty stores hold the leading distribution share at approximately 30% of global revenue. Their dominance is driven by knowledgeable in-store staff, broad premium assortments, and strong consumer trust in specialized pet retailers. These outlets play a crucial role in educating pet owners about allergy management and ingredient selection, which supports higher-value product sales. Veterinary clinics represent the fastest-growing distribution channel, expanding at nearly 9% CAGR. Growth in this segment is fueled by rising allergy diagnoses, increasing pet insurance penetration, and the strong recommendation power of veterinarians. Hydrolyzed and prescription-based diets are primarily distributed through this channel, allowing manufacturers to maintain premium pricing and margin stability.

Online retail contributes over 28% of global sales, supported by subscription-based delivery models, auto-replenishment services, and competitive price transparency. Digital platforms are particularly influential among younger pet owners who prioritize convenience and product reviews. E-commerce growth is strongest in North America and China, where logistics infrastructure supports fast delivery of specialized diets.

Price Tier Insights

Super-premium and veterinary prescription products account for approximately 38% of total 2025 revenue, making them the leading price tier. Their dominance is attributed to clinically validated benefits, higher ingredient quality standards, and strong brand loyalty. Consumers are increasingly willing to pay premium prices for targeted allergy relief and long-term preventive health benefits.

The premium tier maintains steady expansion as brands introduce accessible hypoallergenic variants that balance affordability with functional claims. This tier is particularly important in Western Europe and Japan, where quality perception drives purchasing decisions. Mass-premium products are expanding primarily in emerging markets such as Brazil, India, and Southeast Asia, where price sensitivity remains a key purchase determinant. Local manufacturing expansion is helping reduce costs and improve affordability within this segment.

Explore more data points, trends and opportunities Download Free Sample Report

Hypoallergenic Pet Foods Market Segmentations

By Product Type

- Limited Ingredient Diets (LID)

- Hydrolyzed Protein Diets

- Novel Protein-Based Diets

- Grain-Free & Gluten-Free Diets

- Organic & Natural Hypoallergenic Diets

By Application

- Dogs

- Cats

- Other Companion Animals (Small Mammals & Birds)

By Distribution Channel

- Pet Specialty Stores

- Veterinary Clinics & Hospitals

- Online Retail / E-commerce

- Supermarkets & Hypermarkets

By Price Tier

- Mass / Economy Premium

- Premium

- Super-Premium & Veterinary Prescription

Regional Insights

North America

North America leads the global market with approximately 38% share in 2025. The United States accounts for nearly 85% of regional demand, driven by high pet ownership rates, strong pet humanization trends, advanced veterinary infrastructure, and widespread pet insurance adoption. The presence of leading multinational manufacturers and well-developed retail networks further supports growth. Increasing awareness of canine dermatological conditions and the growing popularity of subscription-based pet food services are additional key drivers. Canada demonstrates steady growth near 7% CAGR, supported by rising disposable income and expanding specialty pet retail chains.

Europe

Europe contributes approximately 27% of global revenue, with Germany, the United Kingdom, and France leading consumption. Regional growth is driven by stringent pet food quality regulations, strong consumer preference for clean-label and sustainable ingredients, and increasing acceptance of novel protein sources. Western European consumers are particularly receptive to organic and environmentally friendly hypoallergenic formulations. The region also benefits from high veterinary consultation rates and growing awareness of elimination diets for allergy management.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at nearly 10% CAGR. China dominates regional demand due to rapid urbanization, increasing middle-class income, and strong growth in companion animal adoption. Premium pet nutrition awareness is rising significantly in Tier 1 and Tier 2 Chinese cities. Japan represents a mature, high-value market characterized by aging pet populations requiring specialized diets. India is emerging as both a consumption and production hub, supported by expanding domestic manufacturing, improving distribution networks, and rising pet humanization among urban households.

Latin America

Brazil and Mexico are the leading markets in Latin America. Regional growth is supported by increasing pet ownership, modernization of retail infrastructure, and expanding local manufacturing capabilities. Brazil’s growing middle class and strong domestic pet food production industry are helping reduce product costs and improve access to premium hypoallergenic diets. However, price sensitivity remains a moderating factor in overall adoption rates.

Middle East & Africa

The UAE and South Africa lead regional demand, driven by rising premium pet ownership and increasing reliance on imported high-quality formulations. Growth in the Gulf Cooperation Council (GCC) countries is supported by high disposable incomes, expanding specialty pet retail chains, and growing awareness of specialized pet nutrition. In Africa, South Africa acts as the regional hub due to comparatively advanced veterinary services and retail infrastructure. Although overall market share remains smaller relative to developed regions, steady urbanization and premium lifestyle trends are gradually expanding demand.

Key Players in the Hypoallergenic Pet Foods Market

- Mars Petcare

- Nestlé Purina PetCare

- Hill’s Pet Nutrition

- Blue Buffalo

- Royal Canin

- Diamond Pet Foods

- WellPet

- Champion Petfoods

- Unicharm Corporation

- Farmina Pet Foods

- Merrick Pet Care

- Nature’s Variety

- Zignature

- Dechra Pharmaceuticals

- Colgate-Palmolive