Hydrogel Face Mask Market Size

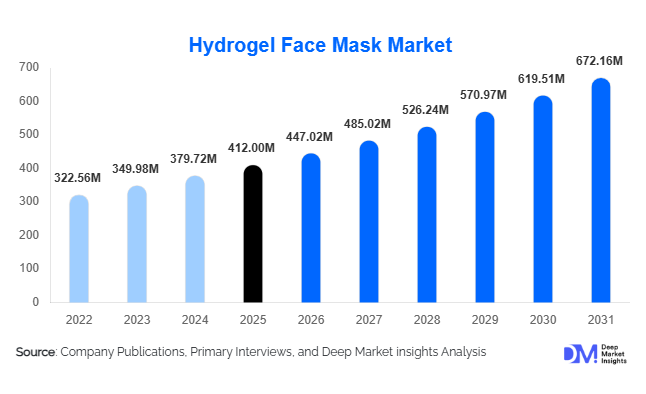

According to Deep Market Insights, the global hydrogel face mask market size was valued at USD 412 million in 2025 and is projected to grow from USD 447.02 million in 2026 to reach USD 672.16 million by 2031, expanding at a CAGR of 8.5% during the forecast period (2026–2031). The hydrogel face mask market growth is primarily driven by rising consumer preference for high-performance skincare, increasing demand for hydration and anti-aging treatments, and expanding adoption of K-beauty-inspired routines across global markets.

Hydrogel masks are formulated using water-soluble gel matrices that enhance ingredient penetration and provide superior skin adherence compared to traditional sheet masks. Their cooling effect, dermatological positioning, and premium appeal have positioned them as a fast-growing category within the broader facial mask industry. Growth is further supported by e-commerce expansion, influencer-driven skincare awareness, and rising disposable incomes in Asia-Pacific and the Middle East.

Key Market Insights

- Sheet hydrogel masks dominate with 58% market share, driven by affordability and widespread consumer familiarity.

- Hyaluronic acid-based masks account for 32% of total revenue, reflecting strong global demand for hydration-focused skincare.

- E-commerce leads distribution with 41% share, supported by cross-border beauty platforms and influencer marketing.

- Asia-Pacific holds 42% of global demand, led by China, South Korea, and Japan.

- Premium products represent 47% of total sales, as consumers increasingly invest in clinically validated skincare.

- Home-use consumers account for 78% of the market, though professional dermatology applications are growing faster.

What are the latest trends in the hydrogel face mask market?

Clean-Label and Sustainable Hydrogel Innovation

Sustainability is emerging as a defining trend in the hydrogel face mask market. Consumers increasingly demand biodegradable hydrogel materials, vegan collagen alternatives, and recyclable packaging. European and North American regulatory frameworks encouraging reduced plastic waste are pushing manufacturers to innovate eco-friendly formulations. Brands are investing in plant-based gel matrices and eliminating synthetic fragrances and parabens. Clean-label positioning, supported by transparent ingredient sourcing and cruelty-free certifications, is enhancing consumer trust and supporting premium pricing strategies.

Dermatology-Backed and Clinical Positioning

Hydrogel masks are increasingly marketed as clinical-grade skincare solutions, particularly for post-procedure recovery and sensitive skin repair. Partnerships with dermatology clinics and aesthetic centers are expanding, positioning hydrogel masks as complementary products following laser treatments and chemical peels. Encapsulated actives and time-release hydrogel technologies are enhancing product efficacy, differentiating premium brands from mass-market competitors. This clinical positioning is elevating consumer perception and driving repeat purchases in developed markets.

What are the key drivers in the hydrogel face mask market?

Rising Demand for Advanced Skincare

Consumers are shifting toward high-performance skincare products that deliver visible results. Hydrogel masks offer superior absorption and longer skin contact time compared to traditional sheet masks, making them attractive for anti-aging, hydration, and brightening applications. Aging populations in North America, Japan, and Europe are contributing significantly to demand for firming and collagen-infused variants.

Growth of Digital Beauty Ecosystems

Social media platforms and online beauty influencers are shaping skincare routines globally. E-commerce channels now represent over 40% of total hydrogel mask sales, supported by subscription models, targeted advertising, and direct-to-consumer strategies. Cross-border online sales from South Korea and China have significantly expanded international availability, accelerating global penetration.

What are the restraints for the global market?

High Product Cost Compared to Sheet Masks

Hydrogel masks are typically priced 20–40% higher than conventional non-woven sheet masks due to advanced materials and ingredient concentration. This pricing gap limits adoption in price-sensitive emerging markets.

Raw Material Price Volatility

Fluctuations in polymer gels, collagen extracts, and active ingredients such as peptides impact production costs and compress margins. Manufacturers must manage sourcing strategies carefully to maintain profitability.

What are the key opportunities in the hydrogel face mask industry?

Expansion in Emerging Asian and Middle Eastern Markets

Rapid urbanization and rising disposable incomes in China, India, Indonesia, the UAE, and Saudi Arabia are creating new demand pools. Climate-specific formulations addressing pollution and humidity-driven skin concerns offer differentiation opportunities. Localization strategies and influencer collaborations can accelerate brand penetration in these markets.

Professional and Medical Aesthetics Integration

The growing global medical aesthetics industry presents a significant opportunity. Professional use currently accounts for roughly USD 91 million but is expanding at nearly 10% CAGR. Hydrogel masks designed for post-laser soothing and skin barrier repair can command higher margins and create recurring institutional demand from dermatology clinics.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 412 Million |

| Market Size in 2026 | USD 447.02 Million |

| Market Size in 2031 | USD 672.16 Million |

| CAGR | 8.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Sheet hydrogel masks dominate the global market, accounting for 58% of total revenue in 2025. Their leadership is primarily driven by ease of application, full-face coverage, and strong alignment with mainstream skincare routines. Consumers prefer sheet formats due to their convenience, single-use hygiene, and compatibility with hydration and anti-aging regimens. The affordability of sheet hydrogel masks compared to specialty formats has enabled mass-market penetration across Asia-Pacific and North America. Additionally, product innovations such as ultra-thin gel matrices, improved adhesion technology, and biodegradable sheet materials have strengthened their competitive advantage. Eye and lip hydrogel masks represent emerging high-margin niches, particularly within anti-aging and brightening categories, where targeted treatment drives premium pricing. Multi-zone hydrogel kits that combine face, neck, and under-eye applications are gaining traction in the luxury segment, increasing average selling prices and basket value. Custom-contoured shapes and hybrid bio-cellulose–hydrogel technologies are further expanding product differentiation and supporting premiumization trends globally.

Ingredient Insights

Hyaluronic acid-based hydrogel masks account for 32% of global revenue, making hydration-focused formulations the leading ingredient category. This dominance is supported by strong dermatological endorsement of hyaluronic acid as a clinically validated moisturizer capable of improving skin barrier function and reducing fine lines. Rising consumer awareness of skin dehydration caused by pollution, air conditioning exposure, and climate variability has reinforced demand for hydrating solutions. Collagen-based masks represent the second-largest segment, driven by aging populations in Japan, Europe, and North America seeking firming and elasticity-enhancing benefits. Peptide-infused and vitamin-enriched hydrogel masks are expanding rapidly within the premium tier, supported by anti-aging and brightening claims. Meanwhile, plant-extract and herbal variants are gaining traction among clean-beauty consumers, particularly in Europe and North America, where demand for vegan, cruelty-free, and botanical-based skincare continues to rise. The shift toward multifunctional ingredients combining hydration, repair, and brightening is shaping future product innovation.

Distribution Channel Insights

E-commerce leads the hydrogel face mask market with a 41% share in 2025, driven by cross-border beauty platforms, influencer marketing, and direct-to-consumer brand strategies. Online retail enables price transparency, product comparison, subscription-based replenishment models, and targeted digital advertising, significantly increasing repeat purchases. Social commerce channels and live-streaming product demonstrations, particularly in China and Southeast Asia, are accelerating impulse buying and new product adoption. Specialty beauty stores and pharmacies continue to play a critical role in consumer trust-building and product trials, especially for dermatology-backed formulations. Professional dermatology and aesthetic clinic channels are expanding steadily in urban centers across Asia-Pacific and North America, supported by rising cosmetic procedures and physician recommendations. Omnichannel integration, combining online engagement with offline experiential retail, is becoming a key competitive differentiator for leading brands.

End-Use Insights

Individual home-use consumers account for 78% of total market demand, valued at approximately USD 321 million in 2025. Growth in this segment is driven by self-care trends, social media-influenced skincare routines, and increasing preference for spa-like treatments at home. Subscription beauty boxes and routine-based skincare regimens have strengthened recurring demand. Meanwhile, professional applications, valued at approximately USD 91 million, are growing at a faster pace due to the expansion of medical aesthetic procedures such as laser resurfacing and chemical peels. Hydrogel masks are widely used post-treatment for soothing and hydration purposes. Export-driven demand from South Korea and China has enhanced global supply chain integration, with these countries serving as major manufacturing and innovation hubs for both consumer and professional-grade hydrogel masks.

Explore more data points, trends and opportunities Download Free Sample Report

Hydrogel Face Mask Market Segmentations

By Product Type

- Sheet Hydrogel Face Masks

- Eye Hydrogel Masks

- Lip Hydrogel Masks

- Neck & Chin Hydrogel Masks

- Multi-zone Hydrogel Kits

By Ingredient Composition

- Hyaluronic Acid-Based

- Collagen-Based

- Peptide & Anti-Aging Complex-Based

- Vitamin-Infused (Vitamin C, E, B3)

- Plant Extract & Herbal-Based

- Charcoal & Detox-Based

By Skin Concern

- Hydration & Moisturization

- Anti-Aging & Firming

- Brightening & Pigmentation Control

- Acne & Oil Control

- Sensitive Skin & Soothing

- Repair & Barrier Strengthening

By Distribution Channel

- E-commerce Platforms

- Specialty Beauty Stores

- Pharmacies & Drugstores

- Supermarkets & Hypermarkets

- Professional Channels

By End-User

- Individual Consumers (Home Use)

- Professional Use

Regional Insights

Asia-Pacific

Asia-Pacific leads the global hydrogel face mask market with a 42% share in 2025 and is projected to remain the fastest-growing region at nearly 9.8% CAGR. China represents the largest consumption base due to strong e-commerce ecosystems, rising middle-class income, and digital beauty culture. South Korea serves as a global innovation hub, exporting advanced hydrogel technologies worldwide and benefiting from strong R&D investment in cosmetic science. Japan’s aging population drives steady demand for anti-aging and collagen-based masks. Regional growth is further supported by expanding urbanization, increasing disposable income in Southeast Asia, and the widespread influence of K-beauty trends.

North America

North America accounts for 24% of global demand, with the United States contributing nearly 85% of regional revenue. Growth is driven by premium skincare adoption, dermatologist-endorsed products, and high consumer spending on beauty and wellness. The increasing popularity of clean-label and cruelty-free skincare formulations further accelerates product innovation. The presence of advanced e-commerce infrastructure and subscription-based beauty services enhances market penetration. Rising medical aesthetic procedures across the U.S. are also contributing to demand in professional channels.

Europe

Europe holds 19% of the global market share, led by France, Germany, the UK, and Italy. Growth drivers include stringent cosmetic regulations promoting ingredient transparency, strong demand for sustainable packaging, and increasing consumer focus on clean beauty standards. Western European consumers are particularly receptive to plant-based and dermatologically tested hydrogel masks. Additionally, rising aging demographics and higher per-capita skincare expenditure in countries such as Germany and France are supporting premium segment expansion.

Middle East & Africa

The Middle East & Africa region represents 8% of the global market, with the UAE and Saudi Arabia leading luxury skincare demand. High disposable incomes, strong preference for premium imported cosmetics, and rapid expansion of beauty retail infrastructure are key growth drivers. Beauty tourism in Dubai and increasing social media influence across the Gulf Cooperation Council (GCC) countries are accelerating adoption. In Africa, South Africa leads regional consumption, supported by growing urban retail channels and international brand penetration.

Latin America

Latin America accounts for 7% of global demand, dominated by Brazil and Mexico. Market growth is supported by expanding online retail infrastructure, increasing beauty awareness among younger consumers, and rising penetration of international skincare brands. Brazil’s strong domestic cosmetics culture and Mexico’s improving digital payment ecosystem are enhancing accessibility. Although price sensitivity remains a constraint, growing middle-income urban populations are supporting steady demand growth for mass and mid-premium hydrogel masks.

Key Players in the Hydrogel Face Mask Market

- Amorepacific Corporation

- LG Household & Health Care

- Estée Lauder Companies

- L'Oréal Group

- Shiseido Company

- Johnson & Johnson

- Unilever

- Procter & Gamble

- Beiersdorf AG

- The Face Shop

- Innisfree

- Dr. Jart+

- JM Solution

- Mediheal

- Watsons Group