Hydration Products Market Size

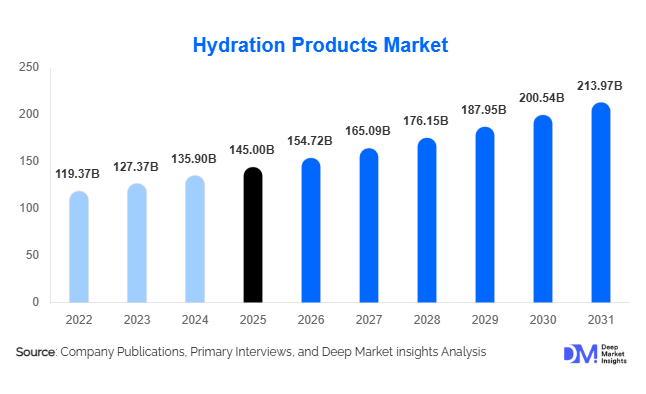

According to Deep Market Insights, the global hydration products market size was valued at USD 145.0 billion in 2025 and is projected to grow from USD 154.72 billion in 2026 to reach USD 213.97 billion by 2031, expanding at a CAGR of 6.7% during the forecast period (2026–2031). The hydration products market growth is primarily driven by rising health awareness, increasing participation in sports and fitness activities, and the global shift toward functional and low-sugar beverages. The transition from traditional sugary drinks to electrolyte-rich, plant-based, and performance-enhancing hydration solutions is significantly reshaping consumer preferences worldwide.

Key Market Insights

- Functional hydration products are gaining strong traction, with consumers prioritizing electrolyte balance, immunity, and energy-boosting benefits.

- Bottled water remains the dominant category, accounting for over 40% of total consumption globally.

- Asia-Pacific dominates the market, driven by population growth, urbanization, and rising disposable incomes.

- Premium and clean-label hydration products are expanding rapidly, especially in North America and Europe.

- E-commerce and direct-to-consumer channels are accelerating market penetration, enabling niche and emerging brands to scale globally.

- Sustainability trends, including recyclable and biodegradable packaging, are reshaping product innovation and brand positioning.

What are the latest trends in the hydration products market?

Rise of Functional and Personalized Hydration

The hydration products market is increasingly shifting toward functional and personalized solutions tailored to individual health needs. Consumers are seeking beverages enriched with electrolytes, vitamins, adaptogens, and nootropics to support performance, recovery, and immunity. Personalized hydration, enabled by wearable devices and health-tracking apps, is emerging as a key trend, particularly among urban and fitness-focused populations. Companies are leveraging AI-driven recommendations and customized formulations to enhance consumer engagement. This trend is also driving innovation in product formats such as hydration powders, tablets, and liquid concentrates that offer convenience and portability.

Sustainable Packaging and Clean-Label Innovation

Environmental sustainability has become a central focus in the hydration products market. Manufacturers are increasingly adopting recyclable PET, aluminum cans, biodegradable materials, and refillable packaging systems to reduce environmental impact. Clean-label formulations, free from artificial additives and excessive sugar, are gaining popularity among health-conscious consumers. Brands are also emphasizing transparency in sourcing and production processes, aligning with global sustainability goals. These initiatives are not only helping companies comply with regulatory standards but also enhancing brand loyalty among environmentally aware consumers.

What are the key drivers in the hydration products market?

Growing Health and Fitness Awareness

The increasing global emphasis on health and wellness is a major driver of the hydration products market. Rising gym memberships, sports participation, and outdoor recreational activities are fueling demand for electrolyte-rich beverages and performance hydration solutions. Consumers are actively replacing carbonated drinks with healthier alternatives, contributing to sustained market growth. This trend is particularly strong among younger demographics and urban populations.

Product Innovation and Premiumization

Continuous innovation in flavors, ingredients, and packaging is driving market expansion. Premium hydration products with added functional benefits, such as immunity support and energy enhancement, are witnessing strong demand in developed markets. Companies are investing in R&D to introduce differentiated offerings, including plant-based hydration drinks and low-calorie formulations. Premiumization is also enabling higher profit margins and brand differentiation.

What are the restraints for the global market?

Fluctuating Raw Material and Packaging Costs

Volatility in raw material prices, particularly for plastic, aluminum, and natural ingredients, poses a significant challenge for manufacturers. These cost fluctuations can impact profit margins and lead to price increases, especially in price-sensitive markets. Supply chain disruptions further exacerbate these challenges, affecting production efficiency and distribution.

Regulatory and Health Compliance Challenges

Stringent regulations related to sugar content, labeling, and environmental impact are increasing compliance costs for market participants. Governments worldwide are implementing stricter policies to address health concerns and sustainability issues, requiring companies to continuously adapt their product formulations and packaging strategies.

What are the key opportunities in the hydration products industry?

Expansion in Emerging Markets

Emerging economies in Asia-Pacific, Africa, and Latin America present significant growth opportunities due to rising disposable incomes, urbanization, and improving retail infrastructure. Increasing awareness of safe drinking water and hydration benefits is driving demand for bottled water and electrolyte solutions. Companies investing in localized production and affordable product lines can capture substantial market share in these regions.

Integration of Technology and Personalized Nutrition

The integration of digital health technologies and personalized nutrition solutions is creating new growth avenues. Smart hydration systems, wearable devices, and mobile apps are enabling consumers to monitor hydration levels and receive tailored recommendations. This convergence of technology and nutrition is expected to redefine consumer engagement and drive innovation in the market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 145 Billion |

| Market Size in 2026 | USD 154.72 Billion |

| Market Size in 2031 | USD 213.97 Billion |

| CAGR | 6.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Bottled water continues to dominate the global hydration products market, accounting for approximately 42% of total market share in 2025. Its leadership is primarily driven by its essential nature, universal accessibility, and strong consumer perception as a safe and reliable hydration source. Rapid urbanization and concerns over drinking water quality in emerging economies further reinforce its dominance. However, the segment is gradually evolving with the rise of functional bottled water, enriched with electrolytes, vitamins, and minerals, catering to health-conscious consumers seeking added wellness benefits.

Sports drinks and electrolyte-based hydration products represent the fastest-growing segment, driven by increasing participation in fitness activities, gym culture, and endurance sports. The growing emphasis on performance hydration, recovery, and energy replenishment has significantly expanded demand. Additionally, product innovation in low-sugar and natural formulations is accelerating adoption across younger demographics. Plant-based hydration beverages such as coconut water and aloe vera drinks are also witnessing strong growth due to their natural positioning, clean-label appeal, and perceived health benefits, particularly in North America and Europe. Key Growth Driver (Segment Level): The global shift toward preventive healthcare, fitness-led lifestyles, and functional nutrition is the primary driver accelerating demand across sports drinks and functional hydration categories.

Distribution Channel Insights

Supermarkets and hypermarkets dominate the distribution landscape with approximately 38% market share, owing to their extensive product assortment, strong retail penetration, and consumer preference for physical product comparison before purchase. These channels remain particularly strong in both developed and emerging markets due to their accessibility and promotional pricing strategies.

However, online retail is the fastest-growing distribution channel, driven by digital transformation, increasing smartphone penetration, and rising preference for convenience-based shopping. Subscription-based hydration delivery services and direct-to-consumer (D2C) brand strategies are further reshaping purchasing behavior. Pharmacies and specialty stores also play a critical role in distributing medical-grade hydration products, electrolyte solutions, and premium wellness beverages, especially in urban markets. Key Growth Driver (Segment Level): The expansion of e-commerce ecosystems, coupled with personalized subscription models and digital health awareness, is significantly accelerating online hydration product sales globally.

End-Use Insights

General consumers represent the largest end-use segment, contributing nearly 60% of total market demand in 2025. This dominance is attributed to the widespread daily consumption of bottled water and packaged hydration products across households, workplaces, and urban populations. Rising awareness of hydration’s role in overall health has further strengthened this segment’s growth.

The sports and fitness segment is the fastest-growing end-use category, expanding at over 8% annually. Growth is fueled by increasing gym memberships, rising participation in endurance sports, and the global fitness movement. Healthcare applications, particularly oral rehydration solutions (ORS), are also contributing significantly due to rising incidences of dehydration-related conditions and increasing focus on preventive healthcare systems. Key Growth Driver (Segment Level): The global expansion of fitness culture and preventive healthcare awareness is the primary factor driving strong demand for functional hydration products across sports and medical applications.

Explore more data points, trends and opportunities Download Free Sample Report

Hydration Products Market Segmentations

By Product Type

- Bottled Water

- Sports Drinks

- Electrolyte Drinks & Powders

- Oral Rehydration Solutions

- Plant-Based & Natural Hydration Drinks

- Hydration Supplements

By Application

- General Consumer Hydration

- Sports & Fitness Performance

- Medical & Clinical Use

- Workforce & Outdoor Hydration

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Pharmacies & Drug Stores

- Online Retail & E-commerce

- Specialty Stores

Regional Insights

Asia-Pacific

Asia-Pacific leads the global hydration products market with approximately 35% share in 2025, making it the largest regional contributor. China and India are the primary growth engines, supported by large population bases, rapid urbanization, and rising disposable incomes. India is among the fastest-growing country markets due to increasing bottled water consumption, expanding retail infrastructure, and growing health consciousness among urban consumers. Rapid urban population growth, increasing heat stress conditions, expanding middle-class income levels, and strong demand for affordable packaged hydration solutions are driving regional expansion.

North America

North America accounts for approximately 28% of the global market share, led by the United States. The region is characterized by high consumption of sports drinks, premium hydration products, and functional beverages. Strong fitness culture, advanced retail penetration, and continuous product innovation are key growth contributors. Rising health consciousness, strong gym and fitness culture, high adoption of functional beverages, and demand for low-sugar premium hydration products are driving sustained growth in the region.

Europe

Europe represents around 22% of the global market, with Germany, the United Kingdom, and France being major demand centers. The region shows a strong preference for sustainable, organic, and clean-label hydration products. Strict environmental regulations and consumer awareness regarding packaging waste are shaping product innovation. Strong sustainability regulations, high demand for eco-friendly packaging, and increasing preference for natural and organic beverages are driving market expansion in Europe.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth due to extreme climatic conditions, high temperatures, and water scarcity challenges. Countries such as the UAE and Saudi Arabia are major consumers of bottled water and electrolyte-based hydration solutions, supported by strong tourism and expatriate populations. Water scarcity, extreme climatic conditions, rising tourism inflow, and increasing dependency on packaged hydration solutions are key factors driving regional demand.

Latin America

Latin America is an emerging hydration products market, led by Brazil and Mexico. Rising urbanization, increasing disposable incomes, and growing awareness of sports and fitness nutrition are driving demand for bottled water and flavored hydration beverages. Expanding urban populations, improving retail infrastructure, and rising adoption of sports and flavored hydration drinks are fueling market growth across the region.

Key Players in the Hydration Products Market

- PepsiCo

- Coca-Cola Company

- Nestlé

- Danone

- Suntory Holdings

- Red Bull

- Keurig Dr Pepper

- Unilever

- Tata Consumer Products

- Bisleri International

- Nongfu Spring

- Tingyi Holding

- Otsuka Holdings

- Primo Water Corporation

- National Beverage Corp