Household Vacuum Cleaners Market Size

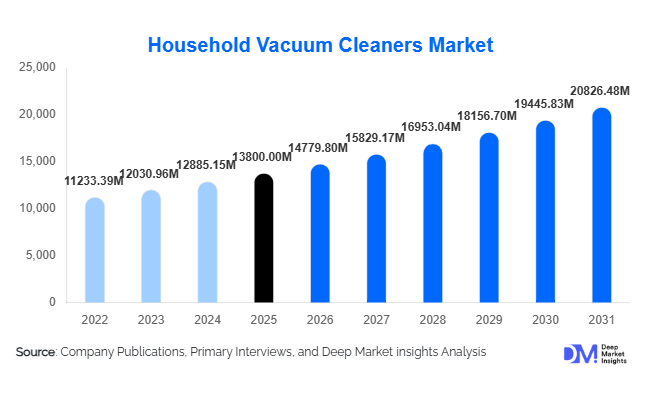

According to Deep Market Insights, the global household vacuum cleaners market size was valued at USD 13,800 million in 2025 and is projected to grow from USD 14.779.80 million in 2026 to reach USD 20,826.48 million by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). The market growth is primarily driven by rising urbanization, increasing consumer awareness regarding hygiene and indoor air quality, and the growing adoption of smart and automated home cleaning solutions. Technological advancements such as robotic vacuum cleaners, cordless systems, and advanced filtration technologies are reshaping the market landscape, while e-commerce expansion is improving accessibility and pricing competitiveness globally.

Key Market Insights

- Robotic and smart vacuum cleaners are gaining rapid traction, driven by increasing adoption of connected home ecosystems and automation technologies.

- Asia-Pacific dominates the global market, supported by large-scale manufacturing and rising middle-class demand in China and India.

- Online retail channels lead distribution, contributing over 50% of global sales due to convenience and competitive pricing.

- Cordless vacuum cleaners are replacing traditional corded systems, driven by portability and improved battery technologies.

- Mid-range products hold the largest market share, balancing affordability with performance and advanced features.

- HEPA filtration systems are increasingly preferred, reflecting growing consumer concerns around allergens and air quality.

What are the latest trends in the household vacuum cleaners market?

Smart and Robotic Cleaning Solutions Transforming Demand

The integration of artificial intelligence, IoT connectivity, and automation is significantly transforming the household vacuum cleaners market. Robotic vacuum cleaners equipped with smart navigation, app-based control, and voice assistant compatibility are becoming mainstream. Consumers are increasingly adopting these devices for their convenience and ability to automate daily cleaning tasks. Advanced features such as LiDAR mapping, obstacle detection, and self-emptying dustbins are enhancing product efficiency and user experience. Additionally, compatibility with smart home ecosystems is positioning robotic vacuum cleaners as essential components of connected households, particularly in developed markets.

Shift Toward Lightweight and Multi-Functional Devices

Consumers are increasingly favoring lightweight, cordless, and multi-functional vacuum cleaners that combine vacuuming with mopping or air purification. This trend is particularly strong in urban environments with compact living spaces, where storage and usability are key considerations. Manufacturers are focusing on ergonomic designs, extended battery life, and improved suction power to meet evolving consumer expectations. Multi-functional devices are also gaining traction in emerging markets, where consumers prefer versatile appliances that deliver greater value for money. This trend is expected to drive innovation and product diversification across all price segments.

What are the key drivers in the household vacuum cleaners market?

Rising Hygiene Awareness and Indoor Air Quality Concerns

Growing awareness of cleanliness and indoor air quality has become a major driver of the household vacuum cleaners market. Post-pandemic behavioral shifts have led consumers to invest more in home cleaning appliances, particularly those equipped with advanced filtration systems such as HEPA filters. These systems effectively capture dust, allergens, and microscopic particles, making them highly desirable in urban environments with increasing pollution levels. The demand for cleaner living spaces is further supported by rising health consciousness and awareness of respiratory conditions.

Technological Advancements and Product Innovation

Continuous innovation in vacuum cleaner technology is driving market growth. Cordless designs, improved battery efficiency, and AI-powered robotic systems have enhanced convenience and performance. Manufacturers are investing heavily in R&D to introduce features such as smart sensors, automated cleaning schedules, and real-time monitoring through mobile applications. These advancements are not only improving product functionality but also attracting younger, tech-savvy consumers who prioritize convenience and automation in household tasks.

What are the restraints for the global market?

High Cost of Advanced Vacuum Cleaners

Premium vacuum cleaners, particularly robotic and high-end cordless models, are relatively expensive, limiting their adoption in price-sensitive markets. While prices are gradually declining due to economies of scale, affordability remains a key barrier, especially in developing regions where consumers may prioritize basic cleaning solutions over advanced appliances.

Availability of Low-Cost Labor Alternatives

In many emerging economies, the availability of affordable domestic help reduces the perceived necessity of investing in vacuum cleaners. This cultural and economic factor acts as a restraint, slowing market penetration despite increasing awareness and urbanization. Overcoming this challenge requires targeted marketing and cost-effective product offerings tailored to these markets.

What are the key opportunities in the household vacuum cleaners industry?

Expansion in Emerging Markets

Emerging economies in the Asia-Pacific, Latin America, and Africa present significant growth opportunities for the household vacuum cleaners market. Rising disposable incomes, rapid urbanization, and expanding housing infrastructure are driving demand for modern home appliances. Companies that focus on affordable, localized product offerings and efficient distribution networks can capture substantial market share in these regions. Government initiatives promoting domestic manufacturing further support market expansion.

Eco-Friendly and Energy-Efficient Product Development

Growing environmental awareness is creating opportunities for manufacturers to develop energy-efficient and eco-friendly vacuum cleaners. Consumers are increasingly seeking products with lower power consumption, recyclable materials, and reduced noise levels. Regulatory frameworks in regions such as Europe are also encouraging sustainable product designs, making this a key area for innovation and differentiation. Companies that align with sustainability trends are likely to gain a competitive advantage.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 13800 Million |

| Market Size in 2026 | USD 14779.80 Million |

| Market Size in 2031 | USD 20826.48 Million |

| CAGR | 7.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Robotic vacuum cleaners represent the fastest-growing and most technologically advanced segment, accounting for approximately 28% of the global market in 2025. This segment is leading due to the rapid adoption of smart home ecosystems, increasing consumer preference for automation, and advancements in AI-driven navigation technologies such as LiDAR mapping and real-time obstacle detection. The ability of robotic vacuums to operate autonomously, integrate with voice assistants, and reduce manual effort makes them particularly attractive in urban households with busy lifestyles. Additionally, declining prices and increased availability across online channels have further accelerated adoption globally.

Upright and canister vacuum cleaners continue to hold a significant combined share due to their high suction power, durability, and cost-effectiveness, especially in traditional markets such as North America and Europe. These products are preferred for deep cleaning carpets and large spaces, making them a staple in households with extensive flooring areas. Stick and handheld vacuum cleaners are gaining strong momentum, driven by their lightweight design, portability, and suitability for compact living spaces, particularly in Asia-Pacific and urban European markets. Central vacuum systems remain a niche but premium segment, primarily installed in high-end residential properties due to their superior performance, low noise levels, and long-term value proposition.

Application Insights

Residential households dominate the household vacuum cleaners market, contributing over 90% of total demand in 2025. This dominance is driven by increasing urbanization, rising disposable incomes, and growing awareness of hygiene and indoor air quality. The expansion of nuclear families and apartment-based living is also increasing the need for efficient and compact cleaning solutions. Additionally, post-pandemic behavioral shifts have reinforced the importance of maintaining clean indoor environments, further boosting adoption.

The small commercial segment, including offices, retail outlets, and service establishments, is emerging as the fastest-growing application segment, with a higher CAGR compared to residential use. Growth in this segment is driven by increasing hygiene regulations, workplace cleanliness standards, and the expansion of commercial infrastructure globally. New application areas such as co-living spaces, short-term rental platforms, and the hospitality industry are also contributing to demand, as these environments require frequent, efficient, and automated cleaning solutions. These evolving applications are expanding the functional scope of vacuum cleaners beyond traditional household use.

Distribution Channel Insights

Online retail channels dominate the distribution landscape, accounting for approximately 52% of global sales in 2025. The leading position of this segment is driven by the rapid growth of e-commerce platforms, which provide consumers with greater product variety, competitive pricing, user reviews, and doorstep delivery convenience. The increasing penetration of smartphones and digital payment systems, particularly in emerging markets, has further strengthened online sales channels. Promotional strategies such as flash sales, bundled offers, and subscription-based purchasing models are also boosting online conversions.

Offline retail channels, including supermarkets, hypermarkets, and specialty electronics stores, continue to play a crucial role, particularly in regions where consumers prefer physical product demonstrations and immediate purchases. These channels are especially relevant for high-value products where tactile experience influences buying decisions. Meanwhile, direct-to-consumer (D2C) channels via brand-owned websites are expanding rapidly, enabling manufacturers to enhance margins, control pricing, and build direct relationships with customers through personalized marketing and after-sales services.

End-User Insights

Residential users form the largest end-user segment, driven by increasing awareness of hygiene, rising living standards, and the growing adoption of modern home appliances. The segment continues to expand as consumers increasingly prioritize convenience and time-saving solutions in their daily routines. The integration of smart technologies into household appliances is further enhancing product appeal in this segment.

The small commercial segment is experiencing rapid growth, particularly in urban areas where offices, retail outlets, and service establishments require consistent and efficient cleaning solutions. The rise of flexible workspaces, co-working hubs, and shared living environments is further boosting demand. Additionally, export-driven demand plays a critical role, with Asia-Pacific countries such as China and Vietnam acting as major manufacturing hubs supplying vacuum cleaners to global markets. This export orientation strengthens production volumes and supports economies of scale for manufacturers.

Explore more data points, trends and opportunities Download Free Sample Report

Household Vacuum Cleaners Market Segmentations

By Product Type

- Upright Vacuum Cleaners

- Canister Vacuum Cleaners

- Stick/Handheld Vacuum Cleaners

- Robotic Vacuum Cleaners

- Central Vacuum Systems

By Technology

- Corded Vacuum Cleaners

- Cordless Vacuum Cleaners

By Filtration System

- HEPA Filtration

- Cyclonic Filtration

- Water Filtration

- Bagged Systems

- Bagless Systems

By Distribution Channel

- Online Retail

- Supermarkets & Hypermarkets

- Specialty Electronics Stores

- Brand Websites (D2C)

By End-User

- Residential Households

- Small Commercial Spaces

Regional Insights

Asia-Pacific

Asia-Pacific leads the global household vacuum cleaners market, accounting for approximately 38% of market share in 2025. The region’s dominance is driven by large-scale manufacturing capabilities, cost advantages, and strong domestic demand. China is the largest contributor, supported by its well-established electronics manufacturing ecosystem and increasing consumer adoption of smart home appliances. India is the fastest-growing market in the region, with a CAGR of around 9%, driven by rapid urbanization, rising disposable incomes, expanding middle-class population, and increasing awareness of hygiene. Additionally, government initiatives such as domestic manufacturing incentives are boosting local production. Japan and South Korea represent mature markets with high penetration of advanced technologies, particularly robotic and cordless vacuum cleaners, driven by tech-savvy consumers and high living standards.

North America

North America accounts for approximately 25% of the global market, with the United States as the primary contributor. Regional growth is driven by high consumer purchasing power, strong adoption of smart home technologies, and a well-established culture of appliance usage. The region has a high penetration of premium products, including robotic and cordless vacuum cleaners, due to consumer preference for convenience and automation. Additionally, the presence of leading market players, continuous product innovation, and strong e-commerce infrastructure further support growth. Replacement demand also plays a key role, as consumers frequently upgrade to newer, more advanced models.

Europe

Europe holds approximately 22% of the global market share, led by key countries such as Germany, the United Kingdom, and France. Growth in this region is primarily driven by stringent energy efficiency regulations, strong environmental awareness, and high demand for sustainable products. Consumers in Europe prefer eco-friendly vacuum cleaners with low power consumption and advanced filtration systems. Government regulations promoting energy labeling and reduced carbon emissions are encouraging manufacturers to innovate in energy-efficient designs. Additionally, high urbanization rates and smaller living spaces are driving demand for compact and cordless vacuum cleaners.

Latin America

Latin America accounts for approximately 8% of the global market, with Brazil and Mexico as the leading countries. Market growth is supported by improving economic conditions, increasing urbanization, and the gradual expansion of the middle-class population. While price sensitivity remains a challenge, demand is shifting toward mid-range and affordable vacuum cleaner models. The growth of organized retail and e-commerce platforms is improving product accessibility across the region. Additionally, increasing awareness of hygiene and modern lifestyles is gradually driving adoption, particularly in urban centers.

Middle East & Africa

The Middle East & Africa region holds approximately 7% of the global market share. Growth in the Middle East is driven by high disposable incomes, rapid urban development, and increasing adoption of premium home appliances, particularly in GCC countries such as the UAE and Saudi Arabia. Modern housing infrastructure and a preference for technologically advanced products are further supporting demand. In Africa, the market is still in the early growth stage but shows strong potential due to rising urbanization, improving economic conditions, and increasing consumer awareness. Expanding retail networks and growing availability of affordable products are expected to drive future growth in the region.