Household Cleaning Products Market Size

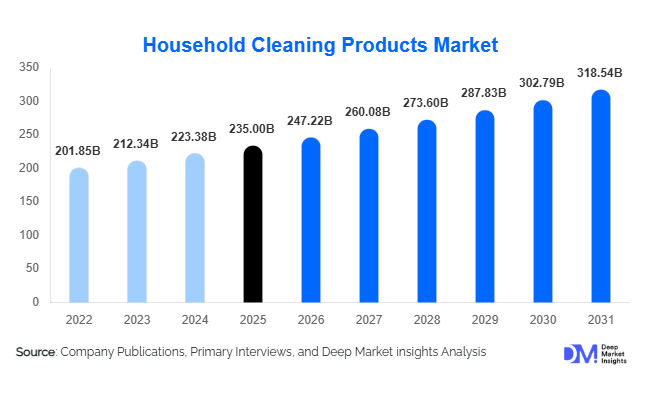

According to Deep Market Insights, the global household cleaning products market size was valued at USD 235.0 billion in 2025 and is projected to grow from USD 247.22 billion in 2026 to reach USD 318.54 billion by 2031, expanding at a CAGR of 5.2% during the forecast period (2026–2031). The market growth is primarily driven by rising global hygiene awareness, increasing adoption of premium and eco-friendly products, and the expansion of e-commerce and direct-to-consumer distribution channels. Post-pandemic shifts in consumer behavior, urbanization, and technological innovations in formulations are also contributing to sustained demand for household cleaning solutions across residential and commercial segments.

Key Market Insights

- Eco-friendly and biodegradable products are gaining significant traction as consumers increasingly prioritize sustainability, and regulatory compliance influences product design.

- Online and e-commerce channels are rapidly expanding, providing greater accessibility, personalized offerings, and subscription-based models for consumers.

- North America maintains a strong market presence, driven by high per capita consumption, premium product adoption, and strong institutional demand.

- Asia-Pacific is the fastest-growing regional market, supported by rising urbanization, expanding middle-class population, and increasing hygiene awareness in China, India, and Southeast Asia.

- Technological advancements in cleaning formulations, such as enzyme-based products, concentrated liquids, and smart dispensing systems, are reshaping the competitive landscape.

What are the latest trends in the household cleaning products market?

Sustainability and Green Product Adoption

Consumers are increasingly demanding eco-friendly alternatives, such as plant-based detergents, biodegradable cleaners, and refillable packaging options. Manufacturers are responding with green formulations, reducing environmental impact while maintaining cleaning efficacy. Regulatory pressures, particularly in Europe and North America, further drive the shift toward non-toxic and low-impact ingredients. Refillable pouches and concentrated products are emerging as popular choices, reducing plastic waste and shipping costs. Sustainability-focused branding is also influencing purchasing decisions, creating opportunities for market differentiation.

Smart and Multi-functional Cleaning Solutions

Technological integration is transforming household cleaning products. Enzyme-based and probiotic formulations enhance efficacy while maintaining environmental safety. Multi-functional products, combining disinfecting, fragrance, and surface protection in a single solution, are increasingly popular in time-constrained households. Automated dispensing systems and smart cleaning devices are also emerging, offering convenience and precise usage, especially in high-income regions. Such innovations cater to digitally savvy consumers and those seeking efficiency without compromising hygiene.

What are the key drivers in the household cleaning products market?

Heightened Hygiene Awareness

The global emphasis on cleanliness, amplified by the COVID-19 pandemic, has permanently influenced consumer behavior. Households and institutions prioritize disinfectants, sanitizers, and multi-purpose cleaning products, creating steady demand growth. This trend extends across residential and commercial applications, including healthcare and hospitality sectors, which maintain stringent sanitation standards.

Urbanization and Rising Disposable Incomes

Urban households, particularly dual-income families, demand convenient, ready-to-use products such as liquid detergents, surface sprays, and dishwashing tablets. Higher disposable incomes allow consumers to invest in premium and multi-functional cleaning solutions. This trend is evident in developed and emerging markets alike, with middle-class growth driving increased household product consumption.

Innovation and Premiumization

Manufacturers are introducing specialty cleaners, eco-friendly formulations, and high-performance products to capture premium segments. Enhanced product features, such as antibacterial action, allergen-free compositions, and fragrance variants, cater to evolving consumer preferences. Premium and green products often command higher profit margins, incentivizing further innovation and product differentiation.

What are the restraints for the global market?

Volatile Raw Material Prices

Fluctuating costs of surfactants, petrochemical derivatives, and other ingredients affect production expenses and retail pricing. This volatility can compress profit margins and necessitate frequent adjustments in pricing strategies, particularly impacting smaller manufacturers with limited hedging capabilities.

Stringent Regulatory Compliance

Increasingly strict regulations governing chemical safety, labeling, and environmental impact require significant investment in R&D and testing. Compliance challenges can delay product launches, particularly for new entrants and smaller players seeking to expand internationally.

What are the key opportunities in the household cleaning products industry?

Expansion of Eco-Friendly and Sustainable Solutions

There is a growing market for biodegradable, plant-based, and non-toxic products. Brands investing in green formulations, carbon-neutral packaging, and refillable options can capture the rapidly expanding premium and environmentally conscious consumer segments. Sustainability trends are especially pronounced in Europe, North America, and parts of Asia-Pacific.

E-Commerce and Direct-to-Consumer Growth

The proliferation of online channels allows brands to reach wider consumer bases with personalized offerings, subscription models, and convenient doorstep delivery. Emerging economies such as India and Brazil are witnessing rapid e-commerce adoption, creating opportunities for both established players and new entrants. Data-driven marketing and product recommendations further enhance customer engagement and retention.

Technological Integration and Product Innovation

Smart cleaning solutions, multi-functional products, and automated dispensing systems offer convenience and efficiency for modern households. Emerging enzyme-based, probiotic, and concentrated formulations provide superior cleaning performance while aligning with sustainability goals. Commercial demand from healthcare, hospitality, and institutional sectors is driving innovation in disinfectants and specialty cleaners.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 235 Billion |

| Market Size in 2026 | USD 247.22 Billion |

| Market Size in 2031 | USD 318.54 Billion |

| CAGR | 5.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Laundry care products continue to dominate the global household cleaning products market, accounting for approximately 38% of the total market share in 2025. This leadership is primarily driven by their essential and high-frequency usage across all household types, making them a non-discretionary category. The rapid shift from powder to liquid detergents, particularly in developed markets, is further strengthening this segment due to superior performance, ease of use, and compatibility with automatic washing machines. Additionally, increasing penetration of washing machines in emerging economies such as India and Southeast Asia is significantly boosting demand. The segment is also benefiting from product innovation, including enzyme-based formulations, fragrance-enhanced detergents, and fabric-specific solutions.

Meanwhile, multi-purpose surface cleaners and specialty cleaning products are witnessing accelerated growth, driven by consumer preference for convenience and time-saving solutions. These products reduce the need for multiple cleaning agents, making them particularly attractive for urban households. Eco-friendly and bio-based cleaning products are also gaining strong momentum within this segment, supported by rising environmental awareness and regulatory pressure. The transition toward sustainable cleaning solutions is expected to further diversify the product landscape while maintaining the dominance of laundry care products globally.

Form Insights

Liquid cleaning products hold the largest share of the market, representing approximately 46% of total consumption. Their dominance is attributed to superior solubility, ease of application, and effectiveness across a wide range of cleaning tasks. Liquid formats are particularly favored in developed regions due to widespread adoption of advanced appliances such as automatic washing machines and dishwashers. Additionally, the growth of concentrated liquid formulas is enabling cost efficiency and reduced packaging waste, aligning with sustainability goals.

Powder-based products continue to maintain strong demand in price-sensitive markets, especially in Asia-Pacific and parts of Latin America, where affordability remains a key purchasing factor. Capsules and tablets are emerging as premium formats, offering precise dosing and convenience, particularly in developed economies. Aerosols and spray-based products are gaining traction in niche applications such as disinfectants and glass cleaners, driven by increased hygiene awareness and the need for targeted cleaning solutions. Overall, the shift toward liquid and unit-dose formats reflects evolving consumer preferences for convenience, efficiency, and sustainability.

Distribution Channel Insights

Supermarkets and hypermarkets dominate the distribution landscape, accounting for approximately 42% of the global market share. Their leadership is driven by extensive product assortments, competitive pricing, and the ability to offer bulk purchasing options, which are particularly appealing for household staples like cleaning products. In-store promotions and brand visibility further enhance consumer engagement in these channels.

However, online and e-commerce channels are the fastest-growing segment, fueled by increasing internet penetration, smartphone usage, and changing consumer buying behavior. Subscription-based purchasing models, doorstep delivery, and personalized product recommendations are key drivers of growth in this channel. The COVID-19 pandemic accelerated the shift toward digital platforms, a trend that continues to sustain momentum. Specialty stores and direct institutional supply channels also play a critical role, particularly in catering to commercial end-users such as hospitals, hotels, and corporate offices, where bulk procurement and customized solutions are essential.

Application Insights

The residential segment remains the largest application area, contributing approximately 78% of total market demand in 2025. This dominance is driven by daily cleaning requirements, rising hygiene awareness, and increased consumption of multi-functional cleaning products. The growing number of nuclear families, urban households, and dual-income consumers is further boosting demand for convenient and efficient cleaning solutions within this segment.

In contrast, the commercial segment is experiencing faster growth, supported by stringent sanitation requirements across industries such as healthcare, hospitality, and food services. Hospitals and healthcare facilities, in particular, are driving demand for high-performance disinfectants and specialized cleaning agents. Emerging applications, including co-living spaces, shared offices, and institutional housing, are also contributing to incremental demand. The increasing emphasis on workplace hygiene and regulatory compliance is expected to sustain growth in the commercial segment over the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

Household Cleaning Products Market Segmentations

By Product Type

- Surface Cleaners

- Dishwashing Products

- Laundry Care Products

- Toilet Care Products

- Specialty Cleaners

- Disinfectants & Sanitizers

By Form

- Liquid

- Powder

- Gel

- Tablets/Capsules

- Sprays/Aerosols

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online/E-commerce

- Specialty Stores

- Direct Sales/Institutional Supply

Regional Insights

North America

North America accounts for approximately 25% of the global market share in 2025, with the United States being the largest contributor. The region’s growth is primarily driven by high per capita consumption, strong purchasing power, and widespread adoption of premium and eco-friendly products. Consumers in this region are highly inclined toward sustainable and non-toxic cleaning solutions, prompting manufacturers to invest heavily in green product innovation. Additionally, the presence of well-established retail infrastructure and the rapid expansion of e-commerce platforms are facilitating easy product accessibility. Institutional demand from healthcare, hospitality, and corporate sectors further strengthens market growth, supported by stringent hygiene regulations and high sanitation standards.

Europe

Europe holds around 22% of the global market share, led by key countries such as Germany, the United Kingdom, and France. The region’s growth is strongly influenced by stringent environmental regulations that promote the use of biodegradable and eco-friendly cleaning products. Consumers in Europe are highly conscious of sustainability, driving demand for green formulations and refillable packaging solutions. Premiumization is another key growth driver, with consumers willing to pay higher prices for high-quality and environmentally responsible products. Additionally, increasing urbanization and the expansion of organized retail and online channels are supporting consistent market growth across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at a CAGR of over 6%, and accounts for approximately 36% of the global market share. China and India are the primary growth engines, driven by rapid urbanization, rising disposable incomes, and expanding middle-class populations. Increasing awareness of hygiene and sanitation, particularly in the post-pandemic era, is significantly boosting product adoption. The growing penetration of washing machines and modern retail formats is further accelerating demand for advanced cleaning products such as liquid detergents and multi-purpose cleaners. E-commerce growth, supported by digital payment systems and aggressive marketing strategies, is also playing a crucial role in market expansion across the region.

Latin America

Latin America represents approximately 9% of the global market, with Brazil and Mexico as the leading contributors. The region’s growth is driven by improving economic conditions, urbanization, and the expansion of the middle-income population. Consumers in this region are increasingly shifting from unbranded or traditional cleaning solutions to branded products, particularly in the mid-range segment. Additionally, the growth of modern retail channels and the increasing penetration of e-commerce platforms are enhancing product accessibility. Price sensitivity remains a key factor, encouraging manufacturers to offer affordable and value-for-money products while maintaining quality.

Middle East & Africa

The Middle East & Africa (MEA) region accounts for around 8% of the global market share, with growth driven by GCC countries and South Africa. Increasing investments in infrastructure, tourism, and hospitality sectors are significantly boosting demand for commercial cleaning products. Government-led sanitation initiatives and rising awareness of hygiene are also contributing to increased consumption of household cleaning products. In the Middle East, high disposable incomes and preference for premium products are supporting market growth, while in Africa, urbanization and improving living standards are driving demand for basic and mid-range cleaning solutions. The expansion of retail networks and local manufacturing capabilities is further strengthening the market outlook in this region.

Key Players in the Household Cleaning Products Market

- Procter & Gamble

- Unilever

- Reckitt Benckiser

- Henkel

- SC Johnson

- Colgate-Palmolive

- Kao Corporation

- Church & Dwight

- Clorox

- Godrej Consumer Products

- Amway

- LG Household & Health Care

- Seventh Generation

- Ecolab

- Diversey Holdings