Home Use Wi-Fi Router Market Size

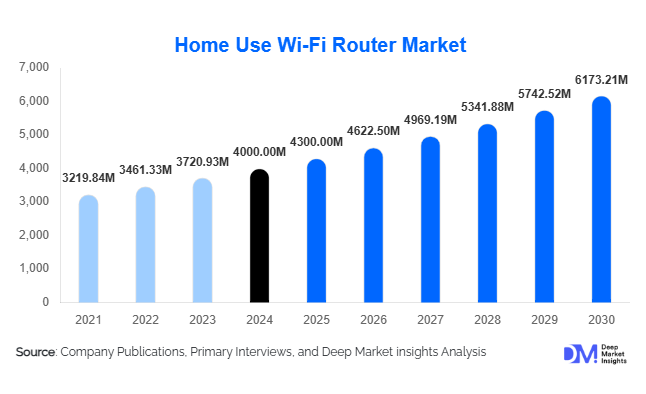

According to Deep Market Insights, the global home use Wi-Fi router market size was valued at USD 4,000 million in 2025 and is projected to grow from USD 4,300 million in 2026 to reach USD 6,173.21 million by 2031, expanding at a CAGR of 7.5% during the forecast period (2026–2031). The market growth is primarily driven by the rapid expansion of broadband connectivity, the proliferation of smart home and IoT devices, and the rising consumer shift toward high-speed Wi-Fi 6 and Wi-Fi 7 technologies.

Key Market Insights

- Wi-Fi 6 and Wi-Fi 6E routers lead global adoption, accounting for nearly 45% of the 2025 market share, as consumers upgrade to next-generation wireless standards.

- Mesh Wi-Fi systems and whole-home coverage solutions are experiencing strong growth due to rising demand for seamless connectivity across larger homes.

- Asia-Pacific dominates global shipments, holding around 35% of the 2025 market, driven by rapid digitalization and increasing broadband penetration in India, China, and Southeast Asia.

- North America remains a mature yet high-value market, with consumers prioritizing premium routers that support smart-home and gaming applications.

- Online retail channels now account for over 40% of sales as consumers increasingly purchase routers through e-commerce platforms.

- Integration of AI, cloud management, and cybersecurity features is transforming the competitive landscape, favoring technologically advanced vendors.

Home Use Wi-Fi Router Market Trends

Smart Home Connectivity Driving Router Upgrades

The surge in smart home adoption is significantly shaping router design and sales. Homes today integrate an expanding array of connected devices, security cameras, smart TVs, thermostats, and voice assistants, all of which demand stable and high-bandwidth connections. As a result, router manufacturers are incorporating IoT-centric features such as device prioritization, parental control dashboards, and automated network management. The convergence of routers with smart-home hubs (e.g., compatibility with Alexa, Google Home, and Apple HomeKit) has become a core differentiator, encouraging consumers to upgrade legacy devices to more intelligent systems.

Wi-Fi 6E and Wi-Fi 7 Technologies Gaining Momentum

Next-generation Wi-Fi 6E and emerging Wi-Fi 7 routers are reshaping consumer expectations, delivering ultra-low latency and multi-gigabit speeds across multiple bands, including the 6 GHz spectrum. Manufacturers are racing to introduce devices with advanced MU-MIMO, OFDMA, and beamforming technologies to handle dense device environments. Early adopters, particularly gamers, streamers, and remote professionals, are driving the adoption curve, while falling chipset costs are accelerating mainstream penetration. By 2031, Wi-Fi 6/7 routers are expected to represent nearly 70% of total global shipments.

Home Use Wi-Fi Router Market Drivers

Expanding Broadband Infrastructure

Governments and private ISPs worldwide are aggressively deploying high-speed broadband and fiber-to-the-home (FTTH) networks. The availability of gigabit internet services increases consumer demand for routers that can support such bandwidths, thereby fueling replacement cycles. National broadband programs in India, China, the U.S., and parts of Europe are directly stimulating router sales.

Growth in Smart Homes and IoT Devices

With the average household now hosting over 15 connected devices, the need for robust wireless coverage and network management has surged. The rise of connected entertainment systems, wearables, and home security applications necessitates routers with improved signal strength, bandwidth allocation, and cybersecurity features, creating consistent demand for mid- to high-end routers.

Remote Work and Digital Learning Adoption

The global shift toward hybrid work models has elevated home networks to mission-critical infrastructure. Consumers increasingly invest in premium routers capable of supporting video conferencing, VPNs, and low-latency streaming. This trend continues to drive consistent year-on-year growth in the residential networking segment.

Home Use Wi-Fi Router Market Restraints

Price Sensitivity in Emerging Economies

Although developing regions are key growth markets, affordability remains a major challenge. Consumers in price-sensitive markets often prefer low-cost routers or delay upgrades, limiting penetration of high-end devices. Competitive pricing pressures also squeeze manufacturer margins, particularly in entry-level categories.

Rapid Technological Obsolescence

Frequent upgrades in Wi-Fi standards, transitioning rapidly from Wi-Fi 5 to Wi-Fi 7, can lead to shorter product lifecycles and hesitant purchase behavior. Consumers may postpone upgrades, waiting for the next-generation model, slowing replacement cycles in mature markets.

Home Use Wi-Fi Router Market Opportunities

Smart Home and IoT Integration

The explosion of connected home devices opens avenues for routers embedded with AI-driven device management, energy-efficient modes, and security firewalls tailored for IoT networks. Vendors integrating router hardware with home-automation platforms stand to capture a substantial share in this emerging niche.

Expansion in Emerging Markets

Massive broadband rollout projects and rising disposable incomes across Asia, Africa, and Latin America present untapped potential. Affordable, feature-rich routers localized for these regions, coupled with ISP bundling partnerships, can generate long-term growth and brand loyalty.

Partnerships with Service Providers

Collaborations between router manufacturers and ISPs offer recurring revenue through subscription models and lease-bundled routers. Such partnerships allow continuous firmware upgrades, cybersecurity updates, and value-added services, enhancing customer retention and long-term profitability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4000 Million |

| Market Size in 2026 | USD 4300 Million |

| Market Size in 2031 | USD 6173.21 Million |

| CAGR | 7.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Mid-speed routers (100 Mbps–1 Gbps) currently dominate, holding nearly 50% of the 2025 market share due to their affordability and suitability for typical household broadband speeds. Mesh Wi-Fi systems are rapidly growing as consumers demand consistent coverage across multi-room homes, while premium gaming routers cater to niche high-performance users seeking ultra-low latency and advanced QoS control. The market is also witnessing growing adoption of hybrid router-AP hubs designed for smart-home ecosystems.

Application Insights

General home usage remains the largest segment, representing approximately 55% of global demand in 2025. However, applications tied to smart home and IoT connectivity are growing fastest, driven by integration with intelligent appliances and home-automation systems. Gaming and work-from-home routers form emerging sub-segments focused on high throughput and network reliability. As broadband penetration deepens, use cases are diversifying to include entertainment streaming, cloud gaming, and virtual collaboration environments.

Distribution Channel Insights

Online retail platforms such as Amazon, Flipkart, and JD.com dominate distribution, accounting for roughly 40% of global router sales. E-commerce provides transparent pricing, rapid delivery, and access to global brands. ISP bundling is the second-largest channel, where routers are included with broadband plans. Physical retail electronics chains still play an important role in mature markets, especially for premium and gaming routers requiring in-store demonstration.

End-Use Insights

The smart-home and IoT end-use segment is projected to grow at over 10% annually through 2031 as households integrate intelligent lighting, appliances, and home monitoring systems. Remote work and digital learning segments also drive sustained demand, particularly in North America and Europe. Export-driven growth from manufacturing hubs such as China, Taiwan, and Vietnam continues to support global router supply and price stability.

Explore more data points, trends and opportunities Download Free Sample Report

Home Use Wi-Fi Router Market Segmentations

By Product Type

- Single Band Routers

- Dual Band Routers

- Tri Band Routers

- Mesh Wi-Fi Systems

By Connectivity Technology

- Wi-Fi 5 (802.11ac)

- Wi-Fi 6 (802.11ax)

- Wi-Fi 6E

- Wi-Fi 7

By Application

- Smart Homes

- Home Entertainment & Streaming

- Remote Work & Learning

- Gaming

By Distribution Channel

- Online Retail (E-commerce Platforms)

- Electronics Stores

- Supermarkets & Hypermarkets

- Telecom Provider Stores

By Price Range

- Budget (Below USD 100)

- Mid-Range (USD 100–250)

- Premium (Above USD 250)

Regional Insights

North America

North America holds about 30% of the 2025 market. High broadband penetration, strong consumer purchasing power, and preference for premium Wi-Fi 6/6E routers define this region. U.S. consumers are early adopters of mesh systems and gaming routers, while Canada shows strong demand for smart-home integration.

Europe

Europe represents a mature but stable market led by the U.K., Germany, and France. Demand is driven by the replacement of legacy Wi-Fi 5 routers with Wi-Fi 6 devices. Consumers favor energy-efficient and data-secure routers, reflecting the region’s focus on digital privacy and green electronics.

Asia-Pacific

Asia-Pacific is the fastest-growing market, accounting for approximately 35% of the global share in 2025. Rising broadband subscriptions, government digitization programs, and rapid urbanization in India, China, Japan, and South Korea are boosting router demand. Local brands such as Xiaomi, Huawei, and TP-Link dominate the regional supply landscape.

Latin America

Latin America, led by Brazil and Mexico, is witnessing steady growth as broadband infrastructure expands. Consumers are transitioning from entry-level to mid-tier routers, supported by increasing online retail availability and ISP partnerships.

Middle East & Africa

This region is in an early growth stage but offers strong potential. Broadband expansion in GCC nations and government-led digital transformation programs are creating demand for next-generation home networking equipment. Africa’s growing internet user base is also stimulating entry-level router demand.

Key Players in the Home Use Wi-Fi Router Market

- TP-Link Technologies Co., Ltd.

- Netgear Inc.

- ASUSTeK Computer Inc.

- D-Link Corporation

- Linksys (Belkin International, Inc.)

- Huawei Technologies Co., Ltd.

- Xiaomi Corporation

- Ubiquiti Inc.

- Google LLC (Nest Wi-Fi)

- Eero (Amazon Inc.)

- Buffalo Inc.

- Zyxel Communications Corporation

- Tenda Technology Co., Ltd.

- Synology Inc.

- Arris / CommScope

Recent Developments

- In May 2025, TP-Link launched its new Archer BE900 Wi-Fi 7 router with quad-band support, targeting high-end smart-home users seeking multi-gig connectivity.

- In April 2025, Netgear introduced firmware upgrades across its Orbi line to enhance mesh stability and cybersecurity protection for IoT devices.

- In February 2025, ASUS announced the expansion of its ROG Rapture gaming router portfolio with advanced cooling and AI-driven QoS optimization.