Home Microcurrent Devices Market Size

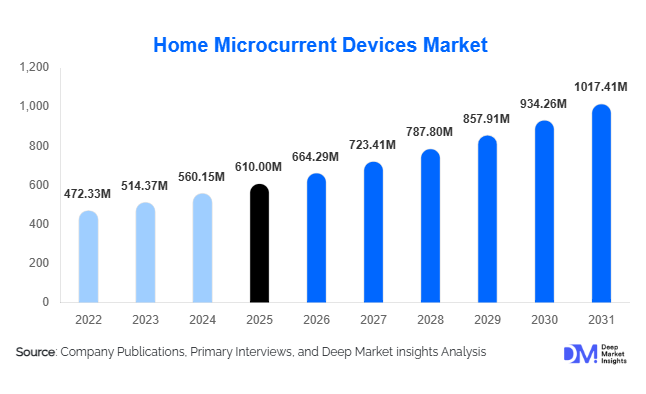

According to Deep Market Insights, the global home microcurrent devices market size was valued at USD 610 million in 2025 and is projected to grow from USD 664.29 million in 2026 to reach USD 1,017.41 million by 2031, expanding at a CAGR of 8.9% during the forecast period (2026–2031). The market growth is primarily driven by increasing consumer preference for non-invasive aesthetic treatments, rising adoption of at-home skincare technologies, and continuous innovation in portable beauty devices. The growing influence of social media, coupled with higher disposable incomes and awareness of anti-aging solutions, is further accelerating demand globally.

Key Market Insights

- Home microcurrent devices are gaining traction as non-invasive alternatives to clinical aesthetic procedures, offering convenience and cost efficiency.

- Online retail dominates distribution channels, accounting for nearly 65% of global sales, driven by direct-to-consumer strategies and influencer marketing.

- North America leads the global market, supported by high consumer awareness and strong purchasing power.

- Asia-Pacific is the fastest-growing region, fueled by rising middle-class income and expanding e-commerce penetration.

- Mid-range devices (USD 100–300) hold the largest share, balancing affordability and product functionality.

- Technological advancements, including AI integration and multifunction devices (microcurrent + LED/RF), are reshaping product innovation.

What are the latest trends in the home microcurrent devices market?

Rise of Multifunctional Beauty Devices

Consumers are increasingly favoring multifunctional devices that combine microcurrent technology with complementary features such as LED therapy, radiofrequency, and thermal treatments. These hybrid devices enhance treatment efficacy while offering better value for money, making them highly attractive in the mid-range and premium segments. Manufacturers are focusing on integrating multiple skincare technologies into a single compact device, reducing the need for multiple products. This trend is particularly strong among tech-savvy consumers who seek comprehensive skincare solutions at home, driving higher adoption rates globally.

Smart and Connected Skincare Ecosystems

The integration of smart technologies is transforming the home microcurrent devices market. Devices equipped with mobile app connectivity, AI-driven skin analysis, and personalized treatment recommendations are becoming increasingly popular. These innovations allow users to track progress, customize routines, and optimize results. Brands are also leveraging data analytics to enhance customer engagement and retention through subscription-based skincare ecosystems. This trend aligns with the broader digital health movement, positioning microcurrent devices as part of a connected wellness lifestyle.

What are the key drivers in the home microcurrent devices market?

Growing Demand for Non-Invasive Aesthetic Solutions

The increasing preference for non-surgical cosmetic treatments is a major driver of market growth. Consumers are seeking safer, cost-effective alternatives to procedures such as facelifts and Botox, leading to higher adoption of home microcurrent devices. These devices offer visible improvements in skin tone and elasticity without downtime, making them highly appealing across age groups.

Influence of Social Media and Beauty Influencers

Social media platforms have significantly amplified awareness and adoption of microcurrent devices. Influencers and skincare professionals regularly showcase product usage and results, building consumer trust and driving purchase decisions. This digital exposure has been particularly effective in targeting younger demographics, accelerating market expansion.

What are the restraints for the global market?

Limited Perception of Clinical Effectiveness

Despite growing popularity, some consumers remain skeptical about the long-term efficacy of home microcurrent devices compared to professional treatments. This perception can limit adoption, particularly among older or more conservative user groups.

Pricing Barriers in Emerging Markets

High costs associated with premium devices restrict accessibility in price-sensitive regions. While mid-range options are expanding, affordability remains a challenge, leading to slower penetration in developing economies.

What are the key opportunities in the home microcurrent devices industry?

Expansion into Emerging Markets

Emerging economies such as India, Brazil, and Southeast Asian countries present significant growth opportunities. Rising disposable incomes, increasing beauty awareness, and rapid e-commerce expansion are enabling deeper market penetration. Localized pricing strategies and region-specific marketing campaigns can further accelerate adoption in these regions.

Integration of AI and Personalized Skincare

The incorporation of artificial intelligence and personalized skincare solutions represents a major opportunity for market players. Devices that adapt to individual skin conditions and provide tailored treatment recommendations can enhance user experience and drive brand differentiation. This trend is expected to attract a new segment of tech-oriented consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 610 Million |

| Market Size in 2026 | USD 664.29 Million |

| Market Size in 2031 | USD 1017.41 Million |

| CAGR | 8.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Facial toning devices dominate the home microcurrent devices market, accounting for approximately 42% of the global share in 2025. This segment leads primarily due to its strong positioning as a non-invasive anti-aging solution and its ease of use for everyday consumers. The growing global focus on facial aesthetics, particularly among the 30–55 age demographic, has significantly boosted demand for these devices. Additionally, aggressive marketing by leading brands and endorsements by dermatologists and influencers have reinforced consumer trust in facial toning technology. Anti-aging and wrinkle reduction devices follow closely, benefiting from the rising global aging population and increasing willingness to invest in preventive skincare. Targeted devices for eye and lip treatments are gaining traction as consumers shift toward precision-based skincare routines, while acne-focused microcurrent devices, though niche, are expanding among younger consumers due to increasing awareness of skin health and early intervention trends.

Technology Type Insights

Dual-mode devices that combine microcurrent technology with LED or radiofrequency functionalities lead the market with an estimated 38% share. The primary growth driver for this segment is the increasing consumer demand for multifunctional, value-driven products that deliver salon-like results at home. These devices enhance treatment effectiveness by addressing multiple skin concerns simultaneously, such as wrinkles, pigmentation, and skin tightening. As a result, consumers perceive higher return on investment, which supports premium pricing strategies. Adjustable and programmable microcurrent devices are also gaining momentum, particularly among experienced users, as they allow for personalized skincare routines tailored to individual skin sensitivity and treatment goals. Continuous innovation in hybrid technologies is expected to further strengthen this segment’s dominance.

Application Insights

Facial care remains the leading application segment, accounting for nearly 55% of total market demand in 2025. The dominance of this segment is driven by the high prevalence of facial skincare concerns, including aging, fine lines, and loss of skin elasticity. Increasing consumer awareness around early anti-aging treatments and preventive skincare is a major growth driver. Additionally, the visibility of facial results compared to other body areas encourages repeat usage and sustained demand. Neck and décolletage applications are witnessing steady growth due to rising awareness of holistic skincare routines that extend beyond the face. Meanwhile, body contouring applications are emerging as a niche but promising segment, supported by growing interest in non-invasive body sculpting solutions and expanding product innovation in this area.

Distribution Channel Insights

Online retail channels dominate the market, contributing approximately 65% of total sales. This segment is primarily driven by the rapid expansion of e-commerce platforms, increasing consumer reliance on digital purchasing, and the effectiveness of influencer-led marketing strategies. Direct-to-consumer (D2C) models adopted by major brands have significantly improved accessibility, pricing transparency, and customer engagement. The ability to compare products, read reviews, and access promotional offers further strengthens online channel dominance. Offline channels, including specialty beauty stores, dermatology clinics, and pharmacies, continue to play a critical role in premium product sales, particularly where professional consultation and product demonstrations are valued. However, their share is gradually being challenged by the convenience and scalability of digital channels.

End-User Insights

Individual consumers represent the largest end-user segment, accounting for over 80% of the market share in 2025. The primary driver for this dominance is the growing preference for at-home treatments that offer convenience, privacy, and cost savings compared to clinical procedures. Increasing awareness of skincare routines and the influence of social media tutorials have further accelerated adoption among this segment. Professional users, including freelance aestheticians and mobile beauty service providers, are emerging as a fast-growing segment. This growth is driven by the increasing trend of personalized at-home beauty services, where professionals use portable microcurrent devices to deliver salon-quality treatments. The expansion of gig-based beauty services is expected to further support demand in this segment.

Explore more data points, trends and opportunities Download Free Sample Report

Home Microcurrent Devices Market Segmentations

By Product Type

- Facial Toning Devices

- Anti-Aging and Wrinkle Reduction Devices

- Skin Tightening Devices

- Eye and Lip Targeted Microcurrent Devices

- Acne Treatment Microcurrent Devices

By Technology Type

- Fixed Frequency Microcurrent Devices

- Adjustable/Programmable Microcurrent Devices

- Dual-Mode Devices

By Application

- Facial Care

- Neck and Décolletage Care

- Body Contouring

By Distribution Channel

- Online Retail

- Brand-Owned Websites

- Specialty Beauty Stores

- Dermatology Clinics and Med Spas

- Pharmacies

By End User

- Individual Consumers

- Professional Users

Regional Insights

North America

North America holds the largest market share at approximately 34% in 2025, with the United States accounting for the majority of regional demand. The region’s leadership is driven by high consumer awareness of advanced skincare technologies, strong purchasing power, and early adoption of beauty-tech innovations. Additionally, the presence of leading market players and robust direct-to-consumer distribution networks has strengthened product availability. The growing trend of preventive anti-aging treatments and the influence of celebrity endorsements further accelerate demand. Regulatory clarity and high standards for product safety also enhance consumer confidence, supporting sustained growth in this region.

Asia-Pacific

Asia-Pacific accounts for around 29% of the global market and is the fastest-growing region, with a CAGR exceeding 10%. Key markets include China, Japan, South Korea, and India. The primary growth drivers include rising disposable incomes, rapid urbanization, and a strong cultural emphasis on skincare and beauty. South Korea and Japan lead in innovation and product development, while China dominates in terms of consumption due to its large population and expanding e-commerce ecosystem. India is emerging as a high-growth market due to increasing digital penetration and growing awareness of at-home beauty solutions. The influence of K-beauty trends and social media platforms is also significantly boosting regional demand.

Europe

Europe represents approximately 22% of the global market, with major demand coming from Germany, the United Kingdom, and France. The region’s growth is driven by an aging population, increasing preference for non-invasive cosmetic treatments, and strong demand for premium skincare products. Consumers in Europe are highly conscious of product quality and safety, leading to increased adoption of clinically validated devices. Sustainability trends and demand for eco-friendly beauty solutions are also shaping purchasing behavior. Additionally, the presence of well-established retail networks and dermatology clinics supports steady market growth.

Latin America

Latin America holds about 8% of the market, with Brazil and Mexico as the leading contributors. The region’s growth is primarily driven by rising middle-class populations, increasing beauty consciousness, and growing exposure to global beauty trends through digital platforms. Brazil, in particular, has a strong culture of aesthetic treatments, which supports demand for at-home alternatives. Expanding e-commerce infrastructure and improved access to international brands are further accelerating market penetration in this region.

Middle East & Africa

The Middle East & Africa region accounts for around 7% of the global market, with the UAE and Saudi Arabia leading demand. Growth in this region is driven by high disposable incomes, increasing demand for premium and luxury beauty products, and a strong preference for technologically advanced skincare solutions. The expansion of high-end retail outlets and beauty clinics is enhancing product visibility and accessibility. Additionally, the region’s young population and growing influence of social media are contributing to rising adoption rates. In Africa, gradual economic development and urbanization are expected to support long-term market growth.