Home Beer Brewing Machine Market Size

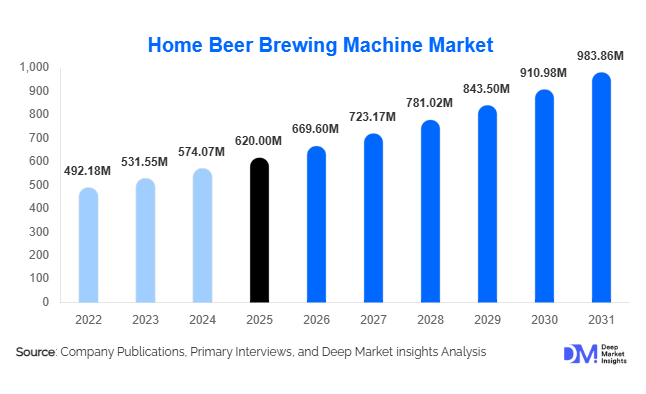

According to Deep Market Insights, the global home beer brewing machine market size was valued at USD 620 million in 2025 and is projected to grow from USD 669.60 million in 2026 to reach USD 983.86 million by 2031, expanding at a CAGR of 8.0% during the forecast period (2026–2031). The market growth is primarily driven by the rising popularity of craft beer culture, increasing consumer interest in personalized beverage production, and the rapid adoption of automated and smart brewing technologies. Growing disposable incomes in North America and Europe, coupled with expanding urban middle-class populations in the Asia-Pacific, are further accelerating demand.

Key Market Insights

- Automated all-in-one brewing systems dominate the market, accounting for over 50% of global revenue in 2025 due to ease of use and precision brewing features.

- Online retail channels lead distribution, contributing nearly 57% of total sales, supported by D2C models and subscription-based ingredient kits.

- North America holds the largest regional share, driven by a strong craft beer culture and permissive home brewing regulations.

- Asia-Pacific is the fastest-growing region, with rising demand in China, Japan, South Korea, and Australia.

- Smart/IoT-enabled brewing machines are gaining traction, supported by mobile app integration and recipe customization features.

- Recurring revenue models through ingredient pods and brewing kits are improving manufacturer margins and customer retention.

What are the latest trends in the home beer brewing machine market?

Smart & IoT-Enabled Brewing Ecosystems

Manufacturers are increasingly integrating IoT connectivity, AI-driven brewing analytics, and mobile app control into home brewing systems. Smart brewing machines allow users to monitor fermentation, adjust temperature settings remotely, and access cloud-based recipe libraries. Subscription platforms offering curated brewing kits and seasonal ingredients are creating recurring revenue streams. This trend is particularly appealing to younger, tech-savvy consumers who value personalization and digital engagement.

Compact & Sustainable Brewing Solutions

Urbanization and apartment living are influencing product design. Compact countertop brewing machines with reduced water and energy consumption are gaining popularity. Sustainable brewing cartridges, recyclable pods, and energy-efficient heating elements are becoming differentiating factors. Consumers increasingly prefer machines that align with environmental values while maintaining high-quality output, encouraging brands to invest in ESG-aligned innovations.

What are the key drivers in the home beer brewing machine market?

Expansion of Global Craft Beer Culture

The rapid growth of craft beer worldwide has fueled interest in experimental and small-batch brewing at home. Consumers seek unique flavors, ingredient control, and customization beyond commercially available beers. This cultural shift toward artisanal production is a primary driver supporting consistent market growth.

Technological Simplification & Automation

Earlier brewing processes required significant expertise and manual intervention. Modern automated systems with pre-programmed brewing cycles, digital interfaces, and fermentation control have lowered the barrier to entry. This democratization of brewing has expanded the consumer base beyond hobbyists to include beginners and lifestyle users.

What are the restraints for the global market?

High Initial Equipment Costs

Premium automated brewing machines range between USD 400 and USD 1,500, limiting accessibility for price-sensitive consumers. Although long-term savings may offset initial costs, the upfront investment remains a barrier in emerging markets.

Regulatory Constraints on Alcohol Production

Home alcohol production regulations vary across countries. In certain regions, licensing requirements, taxation policies, or import restrictions on brewing equipment may hinder market expansion.

What are the key opportunities in the home beer brewing machine industry?

Emerging Market Penetration

Asia-Pacific and Latin America present significant untapped demand. Rapid urbanization, rising disposable incomes, and increasing exposure to Western drinking culture are expanding the addressable market. Strategic pricing and localized marketing can unlock growth potential in China, India, Brazil, and Mexico.

Subscription-Based Brewing Models

Ingredient kit subscriptions, seasonal brewing flavors, and limited-edition collaborations with craft breweries provide recurring revenue opportunities. Companies investing in integrated ecosystems, combining hardware, software, and consumables, are better positioned for long-term profitability and customer retention.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 620 Million |

| Market Size in 2026 | USD 669.60 Million |

| Market Size in 2031 | USD 983.86 Million |

| CAGR | 8.0% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Automated all-in-one brewing systems account for approximately 52% of total market revenue in 2025, making them the dominant product category globally. The primary driver behind this leadership is the increasing demand for convenience, precision, and consistency in home brewing. These systems integrate mashing, boiling, fermenting, and temperature control into a single unit, significantly reducing manual intervention and the risk of brewing errors. Built-in digital interfaces, programmable brewing cycles, and automated cleaning functions further enhance user appeal. The rapid expansion of beginner hobbyists entering the market, particularly in North America and Europe, has accelerated adoption, as consumers prefer plug-and-play systems over complex manual setups. Semi-automated systems continue to attract experienced brewers seeking partial customization and ingredient control, while manual systems remain relevant in entry-level and price-sensitive segments. However, manual machines are gradually losing share as automation becomes more affordable and widely accessible.

Batch Capacity Insights

Medium-capacity brewing machines (5–20 liters) dominate the market with nearly 46% share in 2025, primarily driven by their practicality for household use. This capacity range offers an optimal balance between production efficiency and storage feasibility, making it ideal for regular consumption without requiring excessive storage space. The segment’s growth is further supported by social brewing trends, where consumers brew for small gatherings or hobby clubs. Small-capacity systems (up to 5 liters) are popular among urban apartment dwellers and first-time users experimenting with craft flavors. Large-capacity systems (above 20 liters) are witnessing steady growth among prosumers and small commercial users, including micro-pubs and experimental craft setups, where small-batch innovation is essential for product testing and seasonal offerings.

Connectivity & Technology Insights

Smart and IoT-enabled brewing machines account for approximately 38% of total revenue in 2025 and represent the fastest-growing technology segment. The key growth driver is increasing consumer demand for digital integration and personalization. App-based monitoring, cloud-stored recipe libraries, fermentation alerts, and AI-powered brewing analytics enhance user engagement and reduce brewing errors. Manufacturers are leveraging connectivity to introduce subscription-based ingredient ecosystems and software updates, creating recurring revenue streams. This segment is expanding rapidly in tech-forward markets such as the United States, Germany, Japan, and South Korea, where consumers are receptive to smart home appliance integration.

Distribution Channel Insights

Online retail dominates the global market, contributing nearly 57% of total sales in 2025. The leading driver for this segment is the direct-to-consumer (D2C) sales model adopted by major manufacturers, enabling competitive pricing, bundled ingredient kits, and subscription offerings. E-commerce platforms provide broader geographic reach, transparent product comparisons, and access to global brewing communities. Influencer marketing, digital brewing tutorials, and social media engagement have further accelerated online purchases. While offline specialty brewing stores continue to serve dedicated enthusiast communities, particularly in Germany, the United Kingdom, and the United States, their share is gradually declining due to convenience advantages offered by digital platforms.

End-Use Insights

Residential consumers represent the largest end-use segment, contributing approximately 82% of total market revenue in 2025. The leading growth driver is the expanding DIY culture and increasing consumer preference for personalized, home-crafted beverages. The shift toward experiential home entertainment, particularly after pandemic-driven lifestyle changes, has reinforced demand. Meanwhile, the small commercial/prosumer segment is the fastest-growing category, supported by brew clubs, micro-pubs, and hospitality establishments experimenting with in-house craft offerings. Educational brewing workshops and community-based brewing initiatives are also contributing to incremental demand within this segment.

Explore more data points, trends and opportunities Download Free Sample Report

Home Beer Brewing Machine Market Segmentations

By Product Type

- Automated All-in-One Brewing Systems

- Semi-Automated Brewing Systems

- Manual Brewing Systems

By Batch Capacity

- Up to 5 Liters

- 5–20 Liters

- Above 20 Liters

By Connectivity

- Smart/IoT-Enabled Brewing Machines

- Conventional (Non-Connected) Brewing Machines

By Distribution Channel

- Online Retail

- Offline Retail

By End-Use

- Residential Consumers

- Small Commercial/Prosumers

Regional Insights

North America

North America holds approximately 38% of the global market share in 2025, with the United States alone accounting for nearly 32% of global demand. The primary growth driver is the deeply entrenched craft beer culture and permissive home brewing regulations. High disposable income levels, strong DIY consumer behavior, and widespread adoption of smart appliances further support market expansion. Additionally, the presence of leading manufacturers and established distribution networks enhances product availability. Canada also contributes meaningfully due to rising interest in artisanal beverage production and expanding online retail penetration.

Europe

Europe accounts for roughly 30% of global revenue, led by Germany, the United Kingdom, and Belgium. Regional growth is driven by centuries-old brewing traditions and a strong community of hobbyist brewers. Germany’s engineering-driven preference for precision equipment supports demand for premium automated systems. The United Kingdom’s vibrant craft beer scene and growing home improvement culture are accelerating adoption. Additionally, sustainability awareness across European markets is increasing demand for energy-efficient and environmentally friendly brewing machines.

Asia-Pacific

Asia-Pacific represents approximately 22% of the market in 2025 and is the fastest-growing region, with a CAGR of around 10.5%. Growth is fueled by rising urban middle-class populations, westernization of consumer preferences, and increasing exposure to global craft beer trends. China is emerging as a high-potential market due to rapid urbanization and growing premium beverage consumption. Japan and South Korea show strong adoption of compact and technologically advanced brewing systems, supported by tech-savvy consumers. Australia’s mature craft beer culture also contributes significantly to regional demand.

Latin America

Latin America holds nearly 6% of the global market share, with Brazil and Mexico leading regional demand. Growth drivers include expanding urbanization, rising middle-class incomes, and increasing exposure to North American craft beer trends. The region is witnessing the gradual adoption of mid-range brewing machines, particularly through online channels. Although regulatory complexities in alcohol production pose moderate constraints, growing youth demographics and social brewing communities are expected to sustain long-term growth.

Middle East & Africa

The Middle East & Africa region contributes around 4% of global revenue. South Africa leads regional demand, supported by an established craft beer ecosystem and relatively favorable regulations. The UAE represents a niche premium market driven by high-income expatriate populations and luxury lifestyle preferences. However, stricter alcohol regulations across several Middle Eastern countries limit broader market penetration. Despite regulatory barriers, premium and expatriate-driven demand continues to create selective growth opportunities within urban hubs.

Key Players in the Home Beer Brewing Machine Market

- PicoBrew

- Brewie

- Speidel Braumeister

- Grainfather

- Klarstein

- BrewArt

- iGulu

- WilliamsWarn

- Coopers DIY Beer

- Brooklyn Brew Shop

- Mr. Beer

- BrewZilla

- Northern Brewer

- Ss Brewtech

- Brewferm