Hats and Caps Market Size

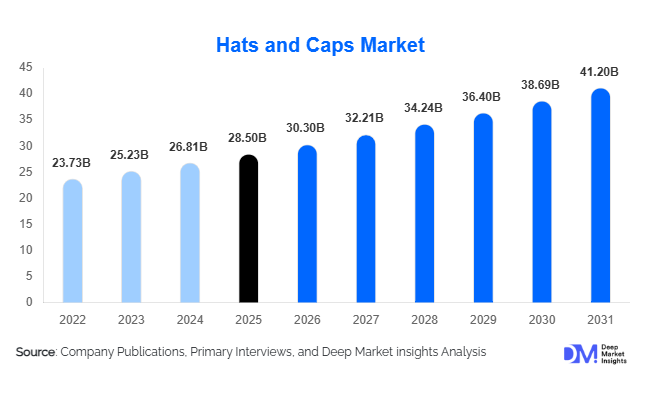

According to Deep Market Insights, the global hats and caps market size was valued at USD 28.5 billion in 2025 and is projected to grow from USD 30.30 billion in 2026 to reach USD 41.2 billion by 2031, expanding at a CAGR of 6.3% during the forecast period (2026–2031). The hats and caps market growth is primarily driven by the rising influence of fashion trends, increased sports and athleisure adoption, and growing e-commerce penetration that has enabled global reach and direct-to-consumer sales.

Key Market Insights

- Hats and caps are increasingly considered fashion and lifestyle statements, with consumers embracing designer collaborations, limited editions, and branded collections.

- Performance and sports caps are seeing strong growth, particularly in running, cycling, golf, and outdoor activity segments, driven by rising health consciousness and fitness participation.

- Asia-Pacific dominates manufacturing and consumption, led by China, India, and Japan, benefiting from large populations, growing middle-class income, and expanding e-commerce infrastructure.

- North America remains a significant market, with the U.S. and Canada accounting for high demand in premium and branded headwear, driven by streetwear and sports culture.

- Europe is witnessing strong growth in fashion-driven and seasonal segments, particularly in Germany, the UK, and France, with consumers favoring branded and sustainable products.

- Technological integration, including moisture-wicking fabrics, UV-protection, and smart customization platforms, is reshaping product functionality and consumer engagement.

What are the latest trends in the hats and caps market?

Fashion and Premiumization Trends

Hats and caps are transitioning from functional items to fashion essentials. Designer collaborations, celebrity endorsements, and influencer-led campaigns are driving premiumization. Limited-edition releases and branded collections attract urban consumers willing to pay higher prices, particularly for baseball caps, bucket hats, and fedoras. Streetwear and casual fashion trends have amplified the popularity of versatile headwear that complements everyday and athleisure outfits. Seasonal fashion rotations and social media-driven visibility are further shaping consumer purchasing behavior.

Performance and Technical Innovation

Technological advances in materials and functionality are a key trend. Caps with moisture-wicking fabrics, UV protection, and antimicrobial treatments are increasingly in demand for sports, outdoor, and fitness applications. Some brands are exploring smart caps with embedded sensors or wearables for activity tracking, while sustainable fabrics such as recycled polyester and organic cotton are gaining traction. These innovations enhance both utility and lifestyle appeal, making headwear relevant across multiple use cases.

What are the key drivers in the hats and caps market?

Rise of Athleisure and Sports Culture

Growing interest in fitness, outdoor activities, and sports participation has accelerated demand for functional headwear. Caps designed for running, cycling, golf, and outdoor sports are driving volume sales globally. Athleisure trends also support crossover usage, where performance caps are adopted for casual wear and lifestyle purposes, expanding the consumer base and creating higher recurring demand.

Fashion Influence and Social Media

Streetwear culture, celebrity endorsements, and social media trends have transformed hats and caps into must-have fashion accessories. Seasonal and limited-edition drops create high consumer engagement, particularly among younger demographics. Branded and premium products benefit from visibility on digital platforms, reinforcing brand value and driving repeat purchases.

E-Commerce and Omnichannel Expansion

Online retail channels have become central to market growth, offering global reach and direct-to-consumer sales models. Brands leverage e-commerce for product customization, limited releases, and global shipping. Digital marketing, influencer campaigns, and social commerce are amplifying reach, particularly in emerging markets such as India, Southeast Asia, and Latin America.

What are the restraints for the global market?

Price Sensitivity in Emerging Markets

While premium and fashion-oriented segments grow, price sensitivity remains a key restraint in developing regions. Consumers in these markets prefer affordable, mid-range products, limiting revenue potential and affecting margin expansion for global brands. Manufacturers must balance cost competitiveness with product innovation to capture these markets.

Seasonality and Demand Fluctuations

Demand for seasonal products, such as woolen beanies in winter or straw hats in summer, creates cyclical revenue patterns. This affects inventory management and operational efficiency, requiring manufacturers to anticipate trends and optimize production to avoid overstock or shortages.

What are the key opportunities in the hats and caps market?

Premium and Branded Fashion Integration

Expanding luxury and designer collaborations represents a major opportunity. Consumers are increasingly adopting hats and caps as fashion statements. Limited-edition releases, urban streetwear trends, and celebrity endorsements can command higher price points, enhancing margins and brand recognition globally. Premiumization is particularly effective in North America, Europe, and APAC urban centers where disposable income supports fashion-forward spending.

Technological and Material Innovation

Integration of technical fabrics and sustainable materials provides differentiation. Products featuring UV protection, moisture-wicking, or eco-friendly fibers appeal to both performance-driven and environmentally conscious consumers. Smart customization platforms, where consumers can personalize embroidery, colors, and styles, also present growth opportunities for direct-to-consumer brands. Sustainability innovations help brands comply with regulations and attract eco-conscious consumers.

Expansion in Emerging Markets via Digital Channels

Rapid urbanization and rising middle-class income in countries such as India, Brazil, and Vietnam present opportunities for market penetration. E-commerce enables brands to reach new customers without heavy investment in offline retail. Social media campaigns and influencer-led marketing accelerate adoption, particularly among younger demographics seeking both fashion and functional headwear. This also opens doors for export-driven demand from APAC manufacturing hubs to North America and Europe.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 28.5 Billion |

| Market Size in 2026 | USD 30.30 Billion |

| Market Size in 2031 | USD 41.2 Billion |

| CAGR | 6.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Baseball caps dominate the global hats and caps market, accounting for approximately 32% of total market share in 2025. Their leadership is driven by unmatched versatility across multiple applications, including casual wear, sports, and promotional branding. The widespread use of baseball caps in corporate marketing campaigns and team merchandise further strengthens their volume demand globally. Additionally, their compatibility with customization, such as logo embroidery and personalized designs, has made them the preferred product type for both individual consumers and institutional buyers.

Bucket hats and beanies are witnessing accelerated growth, supported by evolving streetwear trends and strong influence from celebrity and social media culture. Bucket hats, in particular, have seen a resurgence in younger demographics due to retro fashion revival, while beanies maintain consistent demand in colder regions due to seasonal utility. Performance caps are also gaining traction, particularly in sports such as running, cycling, and golf. This growth is fueled by the increasing integration of athleisure into everyday fashion, where consumers seek functional yet stylish headwear. Technological enhancements such as sweat-wicking linings and lightweight materials are further boosting adoption in this segment.

Material Insights

Cotton-based hats lead the material segment, holding around 38% of the market share in 2025, primarily due to their comfort, breathability, and cost-effectiveness. Cotton’s adaptability across climates and its suitability for mass production make it the preferred choice for both manufacturers and consumers. Its dominance is particularly evident in emerging markets, where affordability and comfort are key purchasing factors. Polyester and blended fabrics represent the second-largest segment, driven by their durability, lightweight properties, and moisture management capabilities. These materials are especially popular in sports and performance applications, where functionality is critical. Wool and straw materials cater to niche segments, with wool dominating winter headwear in colder regions and straw being preferred in tropical and summer environments for sun protection.

A significant emerging trend is the adoption of sustainable materials such as recycled polyester, organic cotton, and biodegradable fibers. This shift is driven by increasing environmental awareness among consumers and regulatory pressures on manufacturers. Brands are leveraging sustainability as a differentiator, particularly in premium markets, where eco-friendly products command higher price points and stronger brand loyalty.

Distribution Channel Insights

Offline retail continues to dominate the market, accounting for approximately 58% of total sales in 2025. This dominance is particularly strong in developing economies where consumers prefer physical product evaluation before purchase. Specialty stores, sports retail chains, and hypermarkets remain key distribution channels, offering a wide range of products and immediate availability. However, online retail is the fastest-growing distribution channel, driven by increasing internet penetration, smartphone usage, and the convenience of home delivery. E-commerce platforms enable brands to reach a global audience while offering extensive product variety and competitive pricing. Customization options available on brand-owned websites further enhance consumer engagement and drive direct-to-consumer sales.

Marketplaces such as Amazon and Alibaba play a critical role in expanding reach, particularly in Asia-Pacific and North America. Additionally, the rise of social commerce and influencer-driven marketing has significantly influenced purchasing behavior among younger consumers. Live-stream shopping and digital campaigns are increasingly becoming key tools for brand promotion and customer acquisition.

End-User Insights

Men represent the largest end-user segment, accounting for approximately 52% of the global market share in 2025. This dominance is attributed to higher adoption rates in sports, outdoor activities, and casual wear. Men's headwear demand is also driven by brand-conscious purchasing and strong association with sports teams and merchandise. The women’s segment, however, is the fastest-growing, fueled by increasing integration of headwear into fashion and lifestyle categories. Fashion-forward designs, seasonal collections, and designer collaborations are encouraging higher adoption among female consumers. The kids’ segment is also expanding steadily, supported by rising parental spending on lifestyle products and growing influence of youth fashion trends.

In terms of application, casual wear dominates the market with approximately 40% share, reflecting the shift of hats and caps into everyday fashion. Sports and fitness applications contribute significantly, driven by rising health awareness and participation in outdoor activities. Promotional and corporate branding segments also play a crucial role, with bulk demand from businesses for marketing purposes. Emerging applications include industrial and safety headwear, where caps are used for both protective and branding purposes.

Explore more data points, trends and opportunities Download Free Sample Report

Hats and Caps Market Segmentations

By Product Type

- Baseball Caps

- Snapback Caps

- Trucker Caps

- Beanies (Knit Caps)

- Bucket Hats

- Visors

- Berets

- Fedoras & Fashion Hats

- Performance/Sports Caps

By Material

- Cotton

- Polyester

- Wool

- Blended Fabrics

- Leather

- Straw

- Technical & Sustainable Fabrics

By End-User

- Men

- Women

- Kids

By Distribution Channel

- Online Retail

- Supermarkets/Hypermarkets

- Specialty Stores

- Sports Retail Chains

- Brand-Owned Stores

By Application

- Casual Wear

- Sports & Fitness

- Fashion & Luxury

- Workwear/Industrial Use

- Promotional/Corporate Branding

Regional Insights

Asia-Pacific

Asia-Pacific is the largest regional market, accounting for approximately 36% of global demand in 2025. China leads both production and consumption due to its strong manufacturing ecosystem, cost advantages, and export capabilities. India is one of the fastest-growing markets, driven by a large youth population, rising disposable income, and rapid expansion of e-commerce platforms. Southeast Asian countries such as Indonesia and Vietnam are also emerging as key growth hubs due to increasing urbanization and retail penetration. The primary drivers of growth in this region include low manufacturing costs, high population density, expanding middle-class demographics, and increasing influence of Western fashion trends. Additionally, strong export demand from North America and Europe supports large-scale production in the region, making APAC both a consumption and supply powerhouse.

North America

North America holds approximately 28% of the global market share, with the United States contributing around 22%. The region’s growth is driven by a well-established sports culture, high disposable income, and strong presence of global brands. Streetwear trends and celebrity endorsements play a significant role in shaping consumer preferences. Key growth drivers include high spending on branded and premium products, widespread adoption of athleisure, and advanced e-commerce infrastructure. The presence of major sports leagues and merchandising opportunities further boosts demand for caps and headwear. Canada contributes through steady demand in both fashion and seasonal segments, particularly winter headwear.

Europe

Europe accounts for approximately 22% of the global market, with Germany, the UK, France, and Italy as major contributors. The region is characterized by strong fashion orientation and seasonal demand patterns, particularly for winter and luxury headwear products. Growth in Europe is driven by increasing consumer preference for sustainable and ethically produced products. Regulatory emphasis on environmental compliance is encouraging manufacturers to adopt eco-friendly materials. Additionally, the popularity of designer brands and premium fashion accessories supports high-value sales. Younger demographics are also driving demand through streetwear and influencer-led trends.

Middle East & Africa

The Middle East & Africa region accounts for approximately 7% of global demand. Key markets include the UAE, Saudi Arabia, South Africa, and Nigeria. The region’s demand is influenced by climatic conditions, with high adoption of caps for sun protection. Growth drivers include increasing urbanization, rising disposable income in Gulf countries, and expanding retail infrastructure. The growing popularity of international fashion brands and sports culture is also supporting demand. In Africa, improving economic conditions and increasing participation in sports are driving adoption, particularly in South Africa and Kenya.

Latin America

Latin America contributes around 7% to the global market, led by Brazil and Mexico. The region shows steady growth, supported by strong sports culture and increasing adoption of casual and outdoor wear. Key growth drivers include rising middle-class income, expanding e-commerce penetration, and growing demand for promotional products. Sports events and team merchandising significantly influence sales, particularly in Brazil. Additionally, increasing awareness of global fashion trends and availability of affordable products are boosting market expansion across the region.