Hand Blenders Market Size

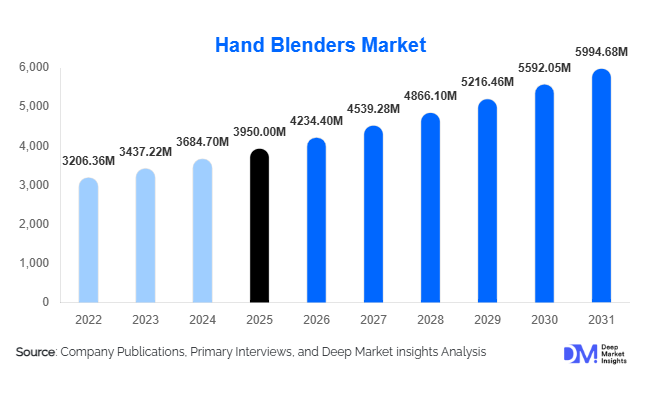

According to Deep Market Insights,the global hand blenders market size was valued at USD 3,950 million in 2025 and is projected to grow from USD 4,234.40 million in 2026 to reach USD 5,994.68 million by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The hand blenders market growth is primarily driven by rising consumer demand for multi-functional and space-saving kitchen appliances, increasing health-conscious cooking practices, and the expansion of premium and commercial-grade hand blender offerings worldwide.

Key Market Insights

- Multi-functional and smart hand blenders are increasingly preferred by consumers, combining blending, chopping, whisking, and food processing in a single appliance.

- Asia Pacific dominates production and demand, led by China and India, where rapid urbanization and rising disposable incomes are accelerating adoption.

- Household use remains the largest segment, accounting for nearly 72% of total market demand, supported by growing home cooking and meal prep trends.

- Commercial food service applications are growing fastest, driven by restaurants, hotels, catering services, and cloud kitchens requiring durable, high-capacity hand blenders.

- Online retail is emerging as a critical distribution channel, enabling direct-to-consumer sales and faster product launches, particularly in emerging markets.

- Technological integration, including variable speed motors, anti-splash designs, turbo modes, and detachable stainless-steel shafts, is enhancing user experience and market appeal.

What are the latest trends in the hand blenders market?

Multi-Functional and Smart Appliances

Manufacturers are increasingly designing hand blenders with multiple attachments, including choppers, whisks, and food processors, to cater to the rising demand for versatile kitchen appliances. Smart appliances featuring variable speed control, turbo modes, and ergonomic designs are gaining traction. These features allow consumers to prepare soups, smoothies, baby food, and protein shakes efficiently. Compact, space-saving designs with detachable stainless-steel shafts are becoming industry standards, appealing to urban households with limited kitchen space.

E-Commerce and Direct-to-Consumer Growth

The surge in online retail platforms has significantly enhanced market reach. Consumers increasingly rely on e-commerce for price comparisons, product reviews, and convenient doorstep delivery. Online channels are also enabling manufacturers to engage directly with customers, reducing dependency on traditional retail and accelerating product launches. Markets in Asia, Latin America, and Europe are seeing rapid growth in online appliance sales, providing manufacturers with a scalable, cost-effective distribution solution.

What are the key drivers in the hand blenders market?

Growing Demand for Convenient Cooking Solutions

Busy lifestyles and dual-income households are driving demand for time-saving kitchen appliances. Hand blenders provide direct blending in containers, reducing preparation and cleaning time. This convenience positions hand blenders as essential kitchen tools in urban households.

Health-Conscious Food Preparation

Rising consumer awareness of healthy diets has increased the demand for fresh smoothies, soups, and baby food. Hand blenders allow for easy preparation of nutritious meals at home, aligning with trends toward wellness and homemade diets.

Emerging Market Penetration

Developing countries such as India, China, Brazil, and Southeast Asian nations are experiencing growing adoption of kitchen appliances due to increasing disposable incomes and rising urban populations. Government initiatives supporting domestic appliance manufacturing further enhance accessibility and affordability.

What are the restraints for the global market?

Competition from Alternative Appliances

High-capacity countertop blenders and food processors offer more power and volume capacity than hand blenders, limiting their adoption in commercial or high-demand household settings. Consumers requiring bulk preparation may prefer conventional blenders over immersion models.

Price Sensitivity in Developing Markets

Consumers in price-sensitive regions may prefer low-cost local brands, creating pricing pressure for global manufacturers. While demand is rising, discretionary spending remains limited among certain demographics, challenging growth for premium hand blender segments.

What are the key opportunities in the hand blenders industry?

Expansion of Multi-Functional Attachments

Opportunities exist in designing modular hand blenders with interchangeable attachments, allowing a single appliance to replace multiple kitchen tools. Smart features, ergonomic designs, and energy-efficient motors offer significant differentiation. Companies investing in these innovations can capture a premium consumer base and expand their market presence globally.

Growth in Commercial Food Service Applications

Restaurants, hotels, and catering services require durable hand blenders for high-volume food preparation. Heavy-duty immersion blenders with stainless steel shafts and high-power motors are increasingly adopted. Manufacturers can tap this growing commercial segment, particularly in urbanized regions where quick-service restaurants and cloud kitchens are proliferating.

Rising E-Commerce Adoption

Online retail growth presents a strategic opportunity for manufacturers to reach a wider consumer base. Direct-to-consumer sales enable faster feedback, improved brand visibility, and lower distribution costs. Emerging markets in Asia and Latin America are particularly promising due to increasing internet penetration and digital payment adoption.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3950 Million |

| Market Size in 2026 | USD 4234.40 Million |

| Market Size in 2031 | USD 5994.68 Million |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The multi-functional hand blender segment leads the global market and accounts for approximately 48% of total demand. The strong performance of this segment is primarily driven by the growing consumer preference for versatile kitchen appliances that can perform multiple functions using a single compact device. Multi-functional hand blenders typically include attachments for blending, chopping, whisking, pureeing, and food processing, making them highly suitable for modern households that prioritize convenience, space efficiency, and time-saving cooking solutions. As urban consumers increasingly prepare diverse meals at home, demand for appliances capable of supporting a wide range of cooking applications continues to grow. Manufacturers are also introducing technologically advanced multi-functional models with variable speed controls, powerful motors, ergonomic designs, and detachable stainless-steel shafts, further strengthening their appeal among consumers.Basic hand blenders continue to maintain a stable presence in the market, particularly among price-sensitive consumers and households that primarily require simple blending functions such as preparing soups, sauces, or smoothies. These products are widely adopted in emerging economies where affordability remains a key purchasing factor. In addition, their compact size and ease of operation make them attractive for small kitchens and occasional use.

Commercial-grade hand blenders represent a smaller but rapidly expanding segment, driven by increasing demand from restaurants, hotels, catering services, bakeries, and institutional kitchens. These high-performance appliances are designed with powerful motors, heavy-duty blades, and enhanced durability to handle large-volume food preparation tasks. The expansion of the food service industry, combined with the growth of cloud kitchens and quick-service restaurants, is contributing significantly to the rising adoption of commercial hand blenders.From a material perspective, stainless-steel hand blenders account for approximately 42% of the market share and are increasingly preferred due to their superior durability, resistance to corrosion, and improved hygiene standards. Stainless steel components are also easier to clean and maintain, making them particularly suitable for both household and commercial food preparation. As consumers become more conscious about product longevity and food safety, manufacturers are prioritizing stainless-steel construction and premium materials in their product offerings.

Application Insights

The household segment dominates the global hand blender market, accounting for nearly 72% of total demand. The leadership of this segment is primarily driven by the increasing trend of home cooking, growing interest in healthy meal preparation, and the rising popularity of homemade beverages such as smoothies, protein shakes, and soups. Hand blenders provide a convenient and efficient solution for preparing a variety of foods including sauces, baby food, purees, and dressings, making them an essential appliance in modern kitchens. The growing adoption of compact kitchen appliances among urban households, particularly among working professionals and nuclear families, further supports the expansion of the household segment.Additionally, the increasing focus on nutrition and wellness has encouraged consumers to prepare fresh meals and beverages at home, boosting the use of hand blenders for blending fruits, vegetables, and protein supplements. The rising number of parents preparing homemade baby food is another key factor contributing to sustained demand in this segment.

Commercial applications represent the fastest-growing segment within the market. Restaurants, hotels, catering services, bakeries, cafes, and institutional kitchens rely on hand blenders for efficient food preparation processes such as blending soups, sauces, batters, and beverages. The global expansion of the food service industry, along with the growth of food delivery services, quick-service restaurants, and cloud kitchens, is creating new opportunities for commercial-grade hand blender adoption. These environments require durable, high-performance appliances capable of operating continuously under heavy workloads.Emerging applications are also contributing to market expansion. Hand blenders are increasingly used for preparing protein shakes, nutritional beverages, and specialty drinks among health-conscious consumers and fitness enthusiasts. Additionally, the growth of home-based food businesses and small-scale culinary entrepreneurs is driving demand for versatile kitchen equipment that can support various food preparation activities efficiently.

Distribution Channel Insights

Offline retail channels currently dominate the global hand blender market, accounting for approximately 60% of total sales. Supermarkets, hypermarkets, appliance retail chains, and specialty kitchen equipment stores remain the primary points of purchase for consumers. The continued dominance of offline channels can be attributed to consumers’ preference to physically evaluate kitchen appliances before purchase, particularly for aspects such as product quality, weight, ergonomics, and brand reputation. Retail stores also provide in-store demonstrations, promotional offers, and customer assistance, which help influence purchasing decisions.Large retail networks also enable manufacturers to maintain strong product visibility through shelf displays, seasonal promotions, and bundled offers. Additionally, in developing markets, offline retail channels remain the most accessible distribution method for consumers who may have limited access to e-commerce platforms.

However, online retail is emerging as the fastest-growing distribution channel in the hand blender market. The rapid expansion of e-commerce platforms, increasing internet penetration, and growing consumer familiarity with digital shopping are accelerating the shift toward online purchasing. Online platforms offer several advantages, including wider product selection, competitive pricing, detailed product descriptions, customer reviews, and convenient home delivery services.Manufacturers are increasingly leveraging direct-to-consumer sales through brand websites as well as major e-commerce marketplaces to expand their reach. Digital platforms also provide opportunities for targeted marketing campaigns, product education, influencer collaborations, and rapid product launches. As consumer purchasing behavior continues to evolve toward digital channels, online sales are expected to play an increasingly significant role in overall market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Hand Blenders Market Segmentations

By Product Type

- Basic Hand Blenders

- Multi-Functional Hand Blenders

- Commercial / Heavy-Duty Hand Blenders

- Cordless Hand Blenders

- Smart / Digital Hand Blenders

By Application

- Household / Residential Use

- Restaurants & Food Service

- Hotels & Hospitality

- Catering & Cloud Kitchens

- Institutional Kitchens (Hospitals, Schools)

By Distribution Channel

- Online Retail (E-commerce Platforms)

- Supermarkets & Hypermarkets

- Electronics & Appliance Stores

- Department Stores

- Direct-to-Consumer Brand Websites

By Power Rating

- Below 200 Watts

- 200–400 Watts

- 400–700 Watts

- Above 700 Watts

By Material Type

- Plastic Body Hand Blenders

- Stainless Steel Hand Blenders

- Hybrid Metal-Plastic Hand Blenders

Regional Insights

North America

North America accounts for approximately 21% of the global hand blender market and remains a significant consumer market characterized by strong purchasing power and high adoption of premium kitchen appliances. The United States represents the largest contributor within the region, supported by high disposable income levels, well-developed retail infrastructure, and a strong culture of home cooking and culinary experimentation. Consumers in North America increasingly prefer multi-functional and technologically advanced kitchen appliances that provide convenience, efficiency, and durability.

Another key driver of regional growth is the rising interest in healthy eating habits, which encourages consumers to prepare fresh smoothies, soups, and nutritional beverages at home. The popularity of fitness and wellness lifestyles also contributes to the increasing use of hand blenders for protein shakes and meal preparation. Additionally, the presence of established appliance manufacturers, continuous product innovation, and the strong penetration of e-commerce platforms support the expansion of the market in this region. Canada also demonstrates steady demand for both mid-range and premium hand blenders, supported by urban lifestyles and consumer preference for durable kitchen equipment.

Europe

Europe holds approximately 29% of the global hand blender market and represents one of the most mature markets for small kitchen appliances. Major countries including Germany, France, the United Kingdom, Italy, and Spain contribute significantly to regional demand. Consumers across Europe place strong emphasis on product quality, durability, and design aesthetics, which has led to increasing demand for premium stainless-steel hand blenders and energy-efficient models.One of the major drivers of growth in the European market is the strong consumer focus on sustainability and environmentally responsible products. Many households prefer appliances that offer long operational life, energy efficiency, and recyclable materials. As a result, manufacturers are introducing eco-friendly designs and energy-saving technologies to align with regional sustainability standards and regulatory requirements.The region also benefits from well-established retail and distribution networks, with both online and offline channels contributing significantly to sales. Additionally, Europe is known for its strong culinary culture, which encourages frequent home cooking and experimentation with diverse recipes, further supporting the adoption of versatile kitchen appliances such as hand blenders.

Asia-Pacific

Asia-Pacific dominates the global hand blender market in terms of both production and consumption, accounting for approximately 37% of the total market share. China serves as the primary manufacturing hub for hand blenders due to its extensive electronics manufacturing ecosystem, cost-efficient production capabilities, and strong export infrastructure. Chinese manufacturers supply a large portion of the global demand, making the country a key contributor to global supply chains.India is emerging as one of the fastest-growing consumer markets for hand blenders in the region. Rapid urbanization, increasing disposable income, and expanding middle-class populations are driving the adoption of modern kitchen appliances. The growing popularity of home cooking, combined with the rising number of working professionals seeking convenient meal preparation solutions, is further boosting demand.In developed Asia-Pacific markets such as Japan, South Korea, and Australia, consumers increasingly prefer premium and technologically advanced hand blenders with enhanced functionality, ergonomic designs, and durable materials. The rapid expansion of e-commerce platforms across the region also plays a critical role in expanding product accessibility and enabling manufacturers to reach a broader consumer base. Additionally, the growing influence of health-conscious lifestyles and home-based food businesses is supporting continued market expansion across the Asia-Pacific region.

Latin America

Latin America accounts for approximately 6% of the global hand blender market, with Brazil and Mexico representing the largest demand centers in the region. The market is gradually expanding as urbanization continues to increase and middle-class populations grow across major economies. Consumers are increasingly adopting small kitchen appliances that simplify food preparation and reduce cooking time.Another important driver of regional growth is the gradual expansion of modern retail infrastructure, including supermarkets, hypermarkets, and online marketplaces, which improve product accessibility. In addition, the increasing influence of global kitchen appliance brands is encouraging product awareness and adoption among consumers. Niche market players are also focusing on introducing eco-friendly and multi-functional hand blenders targeted at premium consumer segments, particularly in urban areas with higher purchasing power.

Middle East & Africa

The Middle East and Africa region represents approximately 7% of the global hand blender market and is witnessing steady growth supported by rising urbanization and increasing consumer purchasing power. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa serve as major demand centers due to their relatively strong retail infrastructure and high-income consumer segments.One of the key drivers of growth in the region is the increasing demand for premium imported kitchen appliances, particularly among affluent households and expatriate populations. Consumers in urban areas are increasingly adopting modern kitchen technologies that enhance cooking efficiency and convenience. The expansion of hospitality industries, including hotels and restaurants, also contributes to growing demand for commercial-grade hand blenders.Furthermore, the rapid development of e-commerce platforms and digital retail channels across the Middle East is improving product availability and enabling international appliance brands to enter the market more effectively. As consumer awareness of modern kitchen appliances continues to increase, the adoption of hand blenders is expected to grow steadily across the region.