Hair Loss & Growth Treatment Market Size

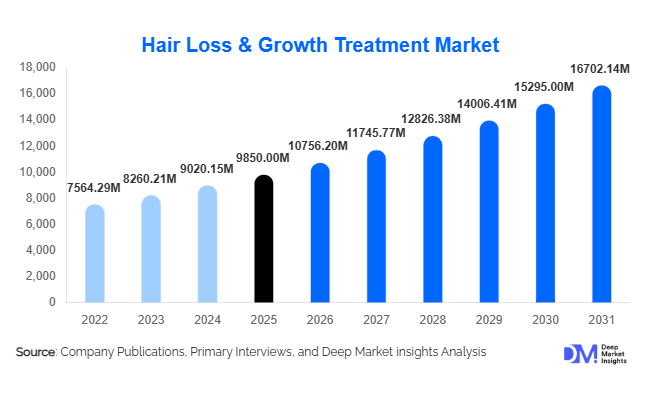

According to Deep Market Insights, the global hair loss & growth treatment market size was valued at USD 9,850 million in 2025 and is projected to grow from USD 10,756.20 million in 2026 to reach USD 16,702.14 million by 2031, expanding at a CAGR of 9.2% during the forecast period (2026–2031). The market growth is primarily driven by the increasing prevalence of alopecia, rising aesthetic awareness among consumers, and rapid advancements in pharmaceutical and regenerative treatment technologies. Growing demand for minimally invasive procedures, combined with the expansion of over-the-counter (OTC) solutions and digital health platforms, is further accelerating adoption globally.

Key Market Insights

- Pharmaceutical treatments dominate the market, driven by widespread adoption of clinically proven solutions such as Minoxidil and Finasteride.

- Regenerative therapies are emerging as high-growth segments, particularly PRP and stem cell-based treatments.

- North America leads the global market, supported by high treatment awareness and strong healthcare infrastructure.

- Asia-Pacific is the fastest-growing region, driven by rising disposable incomes and expanding medical tourism.

- E-commerce channels are rapidly transforming distribution, enabling direct-to-consumer access and personalized treatment plans.

- Technological advancements, including AI diagnostics and home-use laser devices, are reshaping treatment accessibility and outcomes.

What are the latest trends in the hair loss & growth treatment market?

Shift Toward Regenerative and Personalized Treatments

The market is witnessing a strong transition toward regenerative medicine, including platelet-rich plasma (PRP), stem cell therapy, and exosome-based solutions. These treatments focus on restoring natural hair growth mechanisms rather than merely slowing hair loss. Personalized treatment plans based on genetic profiling and scalp diagnostics are also gaining traction, allowing clinicians to tailor therapies for improved outcomes. This trend is particularly strong in developed markets where consumers are willing to invest in premium, long-term solutions.

Rise of At-Home and Digital Treatment Solutions

Home-use devices such as low-level laser therapy (LLLT) systems and app-based treatment platforms are gaining popularity. Consumers increasingly prefer convenient, non-invasive solutions that can be used without clinical visits. Tele-dermatology platforms and subscription-based treatment models are enabling remote consultations, automated product delivery, and continuous monitoring, significantly enhancing customer engagement and retention.

What are the key drivers in the hair loss & growth treatment market?

Increasing Prevalence of Hair Loss Disorders

The rising incidence of androgenetic alopecia and other hair loss conditions is a major driver of market growth. Lifestyle changes, stress, hormonal imbalances, and aging populations are contributing to higher prevalence rates globally. With over half of the male population and a growing percentage of women affected, the demand for effective treatments continues to rise steadily.

Growing Acceptance of Aesthetic and Cosmetic Procedures

Hair restoration treatments are becoming mainstream due to increasing social acceptance and influence from the media and celebrity endorsements. Consumers are more willing to undergo procedures such as hair transplants and PRP therapy, driving demand across clinical and surgical segments. This trend is particularly evident among younger demographics seeking early intervention.

What are the restraints for the global market?

High Cost of Advanced Treatments

Hair transplant procedures and regenerative therapies remain expensive, limiting accessibility for a large segment of the population. The high cost of equipment, skilled professionals, and multiple treatment sessions contributes to pricing challenges, particularly in emerging markets.

Regulatory and Clinical Uncertainties

Many advanced therapies, especially in regenerative medicine, face regulatory hurdles and lack long-term clinical validation. This creates uncertainty among both providers and patients, slowing adoption rates and delaying market expansion in certain regions.

What are the key opportunities in the hair loss & growth treatment industry?

Expansion into Emerging Markets

Emerging economies such as India, China, Brazil, and the UAE present significant growth opportunities due to rising disposable incomes, urbanization, and increasing awareness of hair loss treatments. These markets remain underpenetrated, offering strong potential for both pharmaceutical and cosmetic product manufacturers to expand their presence.

Integration of Digital Health Platforms

The adoption of telemedicine and AI-driven diagnostics is creating new opportunities for market players. Direct-to-consumer models, subscription-based treatment plans, and personalized digital solutions are enabling companies to reach a broader audience while reducing operational costs. This trend is particularly appealing to younger, tech-savvy consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9850 Million |

| Market Size in 2026 | USD 10756.20 Million |

| Market Size in 2031 | USD 16702.14 Million |

| CAGR | 9.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Pharmaceutical treatments continue to dominate the hair loss & growth treatment market, accounting for approximately 38% of global revenue in 2025. This leadership is primarily driven by strong clinical validation, regulatory approvals, and widespread physician recommendations of products such as topical Minoxidil and oral Finasteride. These treatments serve as first-line therapies for androgenetic alopecia, offering cost-effective and accessible solutions for long-term management. Their dominance is further reinforced by high patient compliance, availability across multiple distribution channels, and continuous product innovation, including combination therapies and improved formulations.

Medical devices and procedures, including hair transplant surgeries (FUE and FUT) and low-level laser therapy (LLLT), represent a high-value segment due to their premium pricing and long-term efficacy. This segment is gaining traction as consumers increasingly seek permanent or semi-permanent solutions. The rise in minimally invasive procedures and advancements in robotic hair transplant technologies are further strengthening this segment’s growth trajectory.

Cosmetic and OTC products are experiencing strong demand among early-stage users and preventive care consumers. These include shampoos, serums, and nutritional supplements, which are widely adopted due to affordability and ease of use. Meanwhile, regenerative medicine, encompassing platelet-rich plasma (PRP), stem cell therapy, and exosome treatments, is emerging as the fastest-growing niche. Although currently a smaller segment, it is gaining significant momentum due to its potential to offer biologically driven and long-lasting hair restoration outcomes.

Application Insights

Androgenetic alopecia remains the dominant application segment, contributing nearly 62% of the global market, primarily due to its high prevalence and chronic progression. The condition affects a large portion of both male and female populations, leading to sustained demand for long-term treatment solutions. The segment’s leadership is supported by continuous product innovation, strong clinical research backing, and increasing awareness about early intervention.

Other applications, such as alopecia areata and telogen effluvium, are also gaining prominence, particularly in clinical settings where specialized treatments are required. The rising incidence of stress-induced hair loss, post-COVID telogen effluvium, and hair thinning linked to lifestyle disorders is expanding the addressable patient pool. Additionally, increasing awareness campaigns and improved diagnostic capabilities are enabling earlier detection and treatment, further driving growth across these segments.

Distribution Channel Insights

Retail pharmacies hold a leading position with approximately 34% market share in 2025, driven by the widespread availability of OTC products and strong consumer trust in pharmacy-based recommendations. Their dominance is supported by established supply chains and accessibility across both urban and semi-urban regions. E-commerce platforms are the fastest-growing distribution channel, fueled by the increasing adoption of digital health solutions and direct-to-consumer (DTC) models. Online platforms offer competitive pricing, subscription-based services, and access to a broader product portfolio, making them highly attractive to younger, tech-savvy consumers. The integration of teleconsultation services and AI-based product recommendations is further accelerating online sales.

Specialty clinics and dermatology centers play a crucial role in delivering advanced treatments such as PRP, laser therapy, and hair transplants. These channels are particularly important for high-value procedures, as they provide professional expertise, personalized treatment plans, and higher patient confidence.

End-User Insights

Dermatology clinics dominate the end-user segment, accounting for approximately 36% of the market, driven by increasing demand for professional diagnosis, evidence-based treatments, and access to advanced therapeutic options. The growing preference for clinically supervised treatments, especially for moderate to severe hair loss conditions, continues to support this segment’s leadership.

Hair transplant clinics are witnessing rapid expansion, particularly in medical tourism hubs such as India and Turkey. These clinics benefit from cost advantages, skilled professionals, and increasing international patient inflow, making them key contributors to procedural volume growth. Technological advancements in transplantation techniques are also enhancing success rates and patient satisfaction. The home care segment is emerging as a significant growth area, supported by the rising adoption of OTC products and at-home devices such as laser combs and scalp treatment kits. Consumers are increasingly opting for convenient, cost-effective solutions that can be integrated into daily routines, driving sustained demand in this segment.

Explore more data points, trends and opportunities Download Free Sample Report

Hair Loss & Growth Treatment Market Segmentations

By Product Type

- Pharmaceutical Treatments

- Medical Devices & Procedures

- Cosmetic & OTC Products

- Regenerative Medicine

By Application

- Androgenetic Alopecia

- Alopecia Areata

- Telogen Effluvium

- Other Hair Loss Conditions

By Distribution Channel

- Retail Pharmacies

- Hospital Pharmacies

- E-commerce Platforms

- Specialty Clinics & Dermatology Centers

By End User

- Dermatology Clinics

- Hair Transplant Clinics

- Hospitals

- Homecare Users

Regional Insights

North America

North America holds around 35% of the global market share, with the United States being the dominant contributor. The region’s leadership is driven by high awareness of hair loss treatments, strong healthcare infrastructure, and early adoption of advanced technologies such as regenerative therapies and laser devices. High disposable income and a strong presence of leading pharmaceutical and device manufacturers further support market growth. Additionally, increasing acceptance of aesthetic procedures and the availability of reimbursement frameworks for certain treatments are key regional growth drivers.

Europe

Europe accounts for approximately 25% of the global market, led by countries such as Germany, the UK, and France. Growth in this region is driven by an aging population, rising focus on personal grooming, and increasing demand for non-invasive treatments. Strong regulatory frameworks ensure product safety and efficacy, enhancing consumer confidence. Additionally, growing adoption of natural and organic hair care solutions, along with expanding dermatology services, is contributing to steady market expansion across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 11%, driven by large population bases and rising disposable incomes in countries such as China and India. Increasing awareness of hair loss treatments, coupled with rapid urbanization and lifestyle changes, is fueling demand. India is emerging as a global hub for affordable hair transplant procedures, attracting international patients and boosting medical tourism. In China, the expansion of e-commerce platforms and domestic pharmaceutical manufacturing is accelerating market penetration. Government initiatives supporting healthcare infrastructure development also play a critical role in regional growth.

Latin America

Latin America, led by Brazil and Mexico, is experiencing moderate growth due to a strong cultural emphasis on aesthetics and increasing demand for cosmetic procedures. Rising middle-class income levels and expanding access to dermatological services are key growth drivers. Additionally, the growing presence of international brands and increasing availability of OTC products are improving market accessibility across the region.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth, particularly in countries such as the UAE and Saudi Arabia. High disposable incomes, increasing demand for premium aesthetic treatments, and growing medical tourism are key drivers in the Middle East. In Africa, improving healthcare infrastructure, rising awareness of hair loss treatments, and increasing urbanization are contributing to market expansion. Government investments in healthcare and the gradual adoption of advanced treatment technologies are expected to further support long-term growth in this region.

Key Players in the Hair Loss & Growth Treatment Market

- Johnson & Johnson

- Merck & Co.

- Cipla

- Dr. Reddy’s Laboratories

- Sun Pharmaceutical Industries

- Aclaris Therapeutics

- Revian Inc.

- Lexington International

- Apira Science

- Venus Concept

- Follica Inc.

- Histogen Inc.

- DS Healthcare Group

- Taisho Pharmaceutical

- Rohto Pharmaceutical