Gym Equipment Market Size

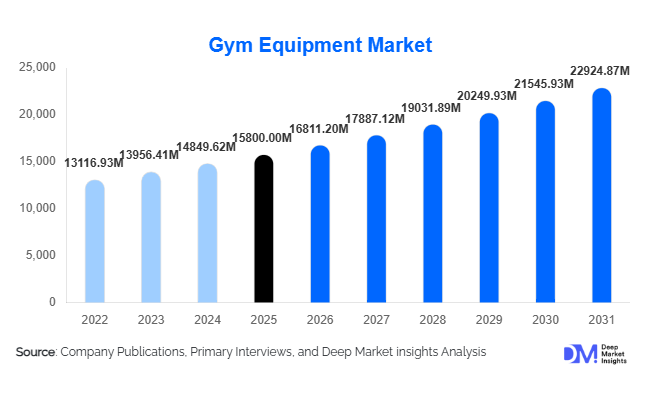

According to Deep Market Insights, the global gym equipment market size was valued at USD 15,800 million in 2025 and is projected to grow from USD 16,811.20 million in 2026 to reach USD 22,924.87 million by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The gym equipment market growth is primarily driven by increasing health awareness, expansion of commercial fitness chains, and rapid adoption of connected and smart fitness equipment across residential and institutional segments.

The industry has evolved beyond conventional strength and cardio machines toward digitally integrated, IoT-enabled ecosystems offering performance analytics, subscription-based training, and AI-driven personalization. Rising obesity rates, preventive healthcare initiatives, and hybrid fitness models combining home workouts with gym memberships are further accelerating demand globally.

Key Market Insights

- Cardiovascular equipment dominates revenue generation, accounting for nearly 42% of the total 2025 market value due to universal adoption across gyms and homes.

- Commercial gyms remain the largest end-user segment, contributing approximately 48% of global demand in 2025 through bulk procurement contracts.

- Connected/smart equipment is the fastest-growing category, expanding at over 9% CAGR, supported by subscription-based digital ecosystems.

- North America leads the global market, accounting for 34% of total revenue, driven by high gym penetration and rapid digital adoption.

- Asia-Pacific is the fastest-growing region, expanding at over 8% CAGR due to urbanization and rising middle-class income.

- The top five companies collectively hold around 38% market share, reflecting moderate consolidation with strong global brands dominating premium segments.

What are the latest trends in the gym equipment market?

Shift Toward Connected & Smart Fitness Ecosystems

Smart gym equipment integrated with AI coaching, cloud analytics, and subscription-based digital content is reshaping the competitive landscape. Connected treadmills, bikes, and strength systems allow users to access virtual training sessions, biometric tracking, and real-time performance dashboards. Manufacturers are increasingly transitioning from one-time hardware sales to recurring revenue models through app subscriptions and digital coaching platforms. This trend is particularly strong in North America and Western Europe, where consumers value immersive, technology-enabled fitness experiences.

Hybrid Fitness Model Driving Residential Demand

The hybrid workout model, combining home-based training and gym memberships, continues to influence purchasing decisions. Residential buyers are investing in compact cardio machines, adjustable dumbbells, and multifunctional strength systems. E-commerce channels are gaining prominence, while direct-to-consumer (D2C) sales are enabling manufacturers to improve margins. The growing popularity of functional training and high-intensity interval training (HIIT) is also boosting demand for kettlebells, resistance bands, and bodyweight systems.

What are the key drivers in the gym equipment market?

Rising Global Health Awareness

Increasing concerns about obesity, cardiovascular diseases, and sedentary lifestyles are driving global fitness participation. Preventive healthcare initiatives and corporate wellness programs are strengthening gym memberships and equipment demand. Governments and insurance providers are encouraging physical activity, creating long-term structural growth.

Expansion of Commercial Fitness Chains

Global and regional fitness chains are expanding aggressively across tier-2 and tier-3 cities. Franchise-based gym models require periodic equipment upgrades every 4–6 years, creating recurring procurement cycles. Boutique studios specializing in CrossFit and functional training are further stimulating demand for strength and cross-training equipment.

What are the restraints for the global market?

High Capital Investment Requirements

Commercial-grade equipment involves significant upfront investment, limiting accessibility for small gym operators in emerging economies. Premium connected machines further increase cost barriers.

Volatility in Raw Material Prices

Steel, aluminum, and electronic components account for a large share of manufacturing costs. Price fluctuations and semiconductor supply chain disruptions can compress margins and influence product pricing.

What are the key opportunities in the gym equipment industry?

Integration with Healthcare & Rehabilitation

Healthcare and rehabilitation centers are increasingly adopting medical-grade fitness equipment for physiotherapy and recovery programs. Aging populations in developed markets are driving demand for low-impact cardio and strength systems integrated with health monitoring tools.

Emerging Market Manufacturing Expansion

Government initiatives such as “Make in India” and “Made in China 2026” are encouraging domestic production. Localized manufacturing reduces import dependency and enhances price competitiveness in fast-growing regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15800 Million |

| Market Size in 2026 | USD 16811.20 Million |

| Market Size in 2031 | USD 22924.87 Million |

| CAGR | 6.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Equipment Type Insights

Cardiovascular training equipment leads the global gym equipment market, accounting for approximately 42% of the 2025 global market value. The segment’s dominance is primarily driven by high utilization rates in commercial gyms, universal consumer familiarity, and its strong positioning in weight management and cardiac health programs. Treadmills remain the single largest revenue contributor within this category, followed by stationary bikes and ellipticals. The leading driver for this segment is the rising global focus on obesity reduction and cardiovascular disease prevention, particularly in North America and Europe. Additionally, the integration of touchscreens, virtual training programs, and performance tracking features has increased average selling prices, further strengthening segment revenue.

Strength training equipment represents approximately 35% of total market revenue in 2025. Growth in this segment is fueled by increasing consumer preference for muscle conditioning, metabolic health improvement, and resistance-based training. The surge in functional fitness formats such as CrossFit and strength-focused boutique studios has driven demand for plate-loaded machines, selectorized systems, and free weights. The primary driver for strength equipment growth is the shift toward long-term metabolic health and muscle preservation, particularly among aging populations and younger demographics focused on physique and athletic performance.

End-User Insights

Commercial gyms & fitness chains dominate the global market with nearly 48% market share in 2025, valued at approximately USD 7,500 million. The leading driver for this segment is structured equipment replacement cycles, typically occurring every 4–6 years, combined with aggressive expansion of franchise-based gym models across urban and semi-urban areas. Large chains negotiate bulk procurement contracts, boosting direct manufacturer revenues and ensuring recurring demand. Residential users represent the fastest-growing end-user segment, expanding at nearly 8% CAGR. The primary growth driver is the sustained hybrid fitness model, where consumers combine home workouts with gym memberships. Rising e-commerce penetration and the availability of compact, multifunctional equipment further accelerate adoption.

Healthcare & rehabilitation centers are emerging as high-growth niches due to aging populations and the increasing emphasis on preventive and recovery-based health programs. Demand is particularly strong for low-impact cardio systems and rehabilitation-focused strength machines. Corporate offices and hospitality segments are steadily expanding, driven by workplace wellness programs and premium hotel fitness infrastructure investments.

Distribution Channel Insights

Direct B2B sales account for roughly 45% of global revenue, driven primarily by commercial gym contracts and institutional procurement. The leading driver for this channel is the need for customized installation, maintenance agreements, and after-sales service, which are critical for commercial operators. Online and e-commerce channels are rapidly expanding within the residential segment, enabling manufacturers to improve margins by reducing intermediary costs. Digital marketing, direct-to-consumer sales models, and installment-based payment options are key growth enablers. Specialty fitness retailers remain important in premium product positioning, while distributor networks dominate developing markets where localized service support is essential.

Technology Insights

Conventional equipment continues to contribute nearly 72% of 2025 revenue due to its affordability and widespread usage across emerging markets. However, connected/smart equipment accounts for approximately 28% of total market revenue and is expanding at over 9% CAGR. The leading driver for this segment is the monetization of digital ecosystems through subscription-based training content, AI-powered personalization, and real-time performance tracking. Connected platforms are enhancing customer retention and increasing average revenue per user (ARPU), making this segment strategically important for manufacturers transitioning toward service-based business models.

Explore more data points, trends and opportunities Download Free Sample Report

Gym Equipment Market Segmentations

By Equipment Type

- Cardiovascular Training Equipment

- Strength Training Equipment

- Functional & Cross-Training Equipment

- Body Composition & Monitoring Equipment

By End-User

- Commercial Gyms & Fitness Chains

- Residential / Home Users

- Healthcare & Rehabilitation Centers

- Corporate Offices & Institutions

- Hospitality

By Distribution Channel

- Direct B2B Sales

- Online / E-commerce

- Specialty Fitness Retailers

- Distributor / Dealer Networks

By Technology

- Conventional (Non-Connected) Equipment

- Connected / Smart Equipment

Regional Insights

North America

North America holds approximately 34% of the global gym equipment market in 2025, making it the largest regional market. The United States alone contributes nearly 29% of global revenue. The primary drivers for regional growth include high gym penetration rates, strong consumer spending capacity, and rapid adoption of connected fitness technologies. The presence of established fitness chains, corporate wellness programs, and preventive healthcare awareness further strengthens demand. Canada supports steady growth through institutional fitness programs and healthcare-linked rehabilitation infrastructure.

Europe

Europe represents around 27% of global revenue. Key markets such as Germany, the United Kingdom, and France drive demand through strong health club memberships and rehabilitation services. The leading growth driver in Europe is the region’s focus on preventive healthcare and government-supported wellness initiatives. Boutique studio expansion, especially in the UK, and aging demographics across Western Europe are accelerating demand for both cardio and strength equipment.

Asia-Pacific

Asia-Pacific accounts for approximately 28% of global demand and is the fastest-growing region, expanding at over 8% CAGR. China and India are primary growth engines due to rapid urbanization, rising disposable incomes, and increasing awareness of lifestyle-related diseases. Expansion of domestic gym chains and government support for sports infrastructure are key drivers. Japan and Australia represent mature markets with high demand for premium and connected equipment. Increasing local manufacturing capacity in China also enhances export competitiveness, strengthening regional supply chains.

Latin America

Latin America holds a smaller but steadily growing market share, led by Brazil and Mexico. Brazil accounts for over 40% of regional demand, supported by a strong fitness culture and expanding mid-tier gym chains. The primary regional driver is growing middle-class participation in organized fitness and increasing penetration of affordable strength and functional training equipment.

Middle East & Africa

The United Arab Emirates and Saudi Arabia are key contributors within this region. Growth is driven by luxury gym infrastructure investments, diversification initiatives focused on wellness tourism, and rising demand for premium fitness facilities. In Africa, South Africa leads demand due to established commercial gym networks. Government-led diversification strategies and urban lifestyle shifts are key drivers supporting long-term market expansion across the region.

Key Players in the Gym Equipment Market

- Technogym

- Life Fitness

- Johnson Health Tech

- Precor

- Nautilus Inc.

- Matrix Fitness

- Cybex International

- Rogue Fitness

- Core Health & Fitness

- Body-Solid

- BH Fitness

- Impulse Fitness

- Shuhua Sports

- Amer Sports

- True Fitness