Gummy Supplements Market Size

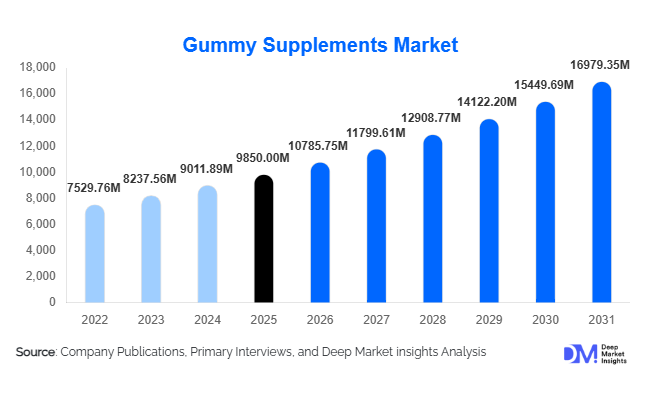

According to Deep Market Insights, the global gummy supplements market size was valued at USD 9,850 million in 2025 and is projected to grow from USD 10,785.75 million in 2026 to reach USD 16,979.35 million by 2031, expanding at a CAGR of 9.4% during the forecast period (2026–2031). The gummy supplements market growth is primarily driven by rising preventive healthcare spending, increasing consumer preference for convenient and palatable supplement formats, and strong innovation in functional nutrition targeting immunity, beauty, gut health, and cognitive wellness.

Once limited to children’s multivitamins, gummy supplements have evolved into a mainstream delivery format across all age groups. Adult-focused formulations now account for the majority of sales, with condition-specific products such as sleep support, stress relief, collagen, and probiotic gummies gaining rapid traction. Clean-label formulations, vegan alternatives using pectin instead of gelatin, and low-sugar innovations are reshaping product development strategies globally. Digital commerce channels, particularly subscription-based direct-to-consumer models, are accelerating penetration in both mature and emerging markets.

Key Market Insights

- Multivitamin gummies dominate with approximately 34% share of the 2025 market, driven by broad consumer applicability.

- Adults (20–59 years) represent the largest consumer segment, accounting for nearly 48% of global revenue.

- North America leads with 38% market share in 2025, supported by high supplement penetration rates.

- Asia-Pacific is the fastest-growing region, expanding at over 11% CAGR due to rising middle-class demand.

- Online retail accounts for 29% of total sales, making it the fastest-growing distribution channel.

- The top five players control approximately 42% of global revenue, indicating moderate market concentration.

What are the latest trends in the gummy supplements market?

Personalized and Condition-Specific Gummies Gaining Momentum

Personalized nutrition is transforming the gummy supplements market. Brands are leveraging digital health assessments, microbiome testing, and AI-based recommendations to develop customized vitamin packs delivered via subscription models. Condition-specific gummies targeting sleep support (melatonin), immunity (elderberry and vitamin C), gut health (probiotics), and beauty-from-within (biotin and collagen) are witnessing double-digit growth. Consumers increasingly prefer tailored solutions over generic multivitamins, encouraging manufacturers to introduce specialized SKUs that command premium pricing and higher margins.

Clean-Label and Sugar-Reduced Innovation

Health-conscious consumers are demanding lower sugar content, plant-based ingredients, and transparent labeling. Manufacturers are reformulating products using natural sweeteners and pectin-based matrices to cater to vegan and diabetic populations. Vegan gummies now account for approximately 22% of global revenue and are growing faster than traditional gelatin-based formats. Clean-label positioning, free from allergens and artificial colors, is becoming a core differentiator in retail and e-commerce platforms, particularly in Europe and North America.

What are the key drivers in the gummy supplements market?

Rising Preventive Healthcare Awareness

Consumers globally are prioritizing preventive care to reduce long-term medical costs and improve quality of life. Increased awareness around immunity, metabolic health, and mental wellness has significantly expanded supplement adoption. Post-pandemic behavior shifts have reinforced daily vitamin consumption habits, particularly in North America and the Asia-Pacific.

Improved Compliance and Consumer Convenience

Gummy supplements offer superior taste and ease of consumption compared to tablets and capsules, improving adherence rates across children and elderly populations. This sensory advantage translates into higher repeat purchase rates and stronger brand loyalty. The format’s portability and chewable convenience align with modern on-the-go lifestyles.

What are the restraints for the global market?

High Sugar Content and Regulatory Scrutiny

Traditional gummy formulations contain added sugars, raising concerns among health regulators and consumers. Stricter labeling requirements and potential sugar taxation policies in certain regions may impact product pricing and margins. Reformulation requires additional R&D investment and manufacturing upgrades.

Stability and Bioavailability Challenges

Maintaining active ingredient potency in gelatin or pectin matrices over an extended shelf life remains technically challenging. Probiotics and omega-3 formulations are particularly sensitive to moisture and temperature, increasing production complexity and cost.

What are the key opportunities in the gummy supplements industry?

Emerging Market Expansion

Asia-Pacific and Latin America present significant untapped potential. Countries such as China, India, Brazil, and Indonesia are experiencing rising disposable incomes and growing awareness of preventive healthcare. Local manufacturing partnerships and regulatory harmonization can accelerate penetration in these high-growth markets.

Beauty-From-Within and Functional Hybrids

The intersection of nutraceuticals and cosmetics is creating opportunities in collagen, hyaluronic acid, and antioxidant-infused gummies. The global beauty supplements segment is growing at over 12% CAGR, with gummies serving as a preferred delivery format. This crossover appeal expands the consumer base beyond traditional vitamin buyers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9850 Million |

| Market Size in 2026 | USD 10785.75 Million |

| Market Size in 2031 | USD 16979.35 Million |

| CAGR | 9.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Multivitamin gummies lead the global market, accounting for approximately 34% of the total 2025 revenue. Their dominance is driven by broad-spectrum health coverage, convenience of once-daily dosing, and strong cross-demographic appeal. Multivitamins serve as entry-level supplements for new consumers and remain staple products for long-term users, ensuring high repeat purchase rates and strong retail penetration. Additionally, aggressive brand marketing, pediatric endorsements, and pharmacy shelf visibility contribute to sustained category leadership. In mature markets such as North America and Europe, multivitamin gummies benefit from established preventive healthcare habits and a strong OTC supplement consumption culture.

Probiotic and specialty functional gummies represent the fastest-growing product categories, expanding at double-digit rates. Rising awareness of gut microbiome health, stress management, sleep disorders, and immune resilience has accelerated demand for condition-specific formulations such as melatonin, collagen, biotin, and elderberry gummies. These products command premium pricing due to targeted functionality and clinically positioned ingredients. Their growth is further supported by influencer marketing, beauty-from-within trends, and increasing consumer willingness to self-manage minor health concerns. Herbal and botanical gummies, including elderberry and ashwagandha formulations, are witnessing strong uptake in North America and Europe as consumers shift toward plant-based and adaptogenic wellness solutions. The clean-label movement and preference for naturally derived ingredients are key drivers behind this segment’s expansion.

Consumer Group Insights

Adults (20–59 years) account for nearly 48% of global revenue, making them the dominant consumer segment. Growth in this demographic is primarily driven by rising stress levels, sedentary lifestyles, and increased focus on immunity, beauty, and cognitive performance. Working professionals increasingly prefer convenient supplement formats that align with busy schedules, making gummies particularly attractive. The expansion of direct-to-consumer subscription models targeting millennials and Gen Z further strengthens adult segment dominance. The children’s segment remains stable and structurally important, supported by parental focus on immunity, growth, and nutritional gap-filling. Pediatricians often recommend chewable formats for compliance, ensuring steady baseline demand.

The geriatric population (60+ years) is an emerging high-potential segment. Rising global aging populations, particularly in Japan, Europe, and North America, are driving demand for calcium, vitamin D, magnesium, and joint-support gummies. Ease of chewing compared to tablets enhances adoption in this age group, positioning it as a medium-term growth driver.

Distribution Channel Insights

Online retail represents approximately 29% of global sales in 2025 and is the fastest-growing distribution channel. Growth is driven by subscription-based vitamin programs, personalized nutrition platforms, transparent pricing models, and access to product reviews. Direct-to-consumer brands are leveraging social media marketing and influencer partnerships to scale rapidly without traditional retail constraints. The pandemic-induced shift toward e-commerce has permanently altered buying behavior, particularly in the U.S., China, and India. Pharmacies and drug stores continue to play a critical role in North America and Europe due to consumer trust and professional recommendations. Meanwhile, supermarkets and hypermarkets contribute significantly to impulse purchases and brand visibility, particularly for multivitamins and children’s gummies.

Ingredient Source Insights

Vegan and plant-based formulations hold around 22% of the global market share and are expanding faster than synthetic alternatives. Growth is driven by rising vegan populations, dietary restrictions, halal and kosher compliance considerations, and sustainability preferences. European markets, particularly Germany and the UK, demonstrate strong demand for pectin-based gummies as consumers actively avoid animal-derived gelatin. Additionally, ethical sourcing and clean-label transparency are influencing purchasing decisions, encouraging manufacturers to reformulate portfolios accordingly.

Explore more data points, trends and opportunities Download Free Sample Report

Gummy Supplements Market Segmentations

By Product Type

- Multivitamin Gummies

- Single Vitamin Gummies

- Mineral Gummies

- Omega-3 & Fatty Acid Gummies

- Probiotic & Prebiotic Gummies

- Herbal & Botanical Gummies

- Specialty Functional Gummies

By Consumer Group

- Children (2–12 Years)

- Teenagers (13–19 Years)

- Adults (20–59 Years)

- Geriatric (60+ Years)

- Prenatal & Postnatal Women

By Distribution Channel

- Pharmacies & Drug Stores

- Supermarkets & Hypermarkets

- Specialty Health Stores

- Online Retail

- Direct-to-Consumer

By Ingredient Source

- Synthetic Ingredients

- Naturally Derived Ingredients

- Vegan/Plant-Based Formulations

By Dosage Functionality

- General Wellness

- Therapeutic/Condition-Specific

- Preventive Care

Regional Insights

North America

North America accounts for approximately 38% of global revenue in 2025, with the United States contributing nearly 32% of total global demand. The region’s dominance is driven by high per capita supplement consumption, strong preventive healthcare awareness, and mature retail infrastructure. The U.S. benefits from an established dietary supplement regulatory framework under DSHEA, enabling rapid product innovation. High disposable incomes, strong DTC brand presence, and aggressive marketing strategies further support growth. Canada represents a steady-growth market supported by pharmacy chains and increasing clean-label demand. Innovation in sugar-free and plant-based gummies is particularly strong across this region.

Europe

Europe holds roughly 26% market share, led by Germany, the U.K., France, and Italy. Growth is driven by stringent regulatory standards that enhance consumer trust, alongside strong adoption of vegan and clean-label formulations. The European aging population significantly contributes to the demand for bone health and immunity supplements. Germany remains the largest importer and consumer market within the region due to high nutraceutical penetration. Sustainability-conscious purchasing behavior and demand for ethically sourced ingredients act as primary regional growth drivers.

Asia-Pacific

Asia-Pacific commands 24% of global share and is the fastest-growing region at over 11% CAGR. China and India are primary growth engines due to expanding middle-class populations, increasing digital commerce penetration, and growing awareness of preventive health. Government health campaigns promoting immunity and nutritional supplementation further support regional expansion. Japan’s aging population drives demand for functional and bone-support gummies, while Australia shows strong uptake of premium and organic formulations. Cross-border e-commerce platforms in China are accelerating imports of North American and European gummy brands.

Latin America

Latin America represents around 7% of global demand, with Brazil and Mexico leading consumption. Rising urbanization, improving healthcare awareness, and growing middle-income populations are supporting market expansion. Increasing penetration of modern retail chains and online marketplaces is enhancing product accessibility. However, pricing sensitivity remains a constraint, encouraging the growth of mid-range and locally manufactured gummy supplements.

Middle East & Africa

The Middle East & Africa region accounts for nearly 5% of global sales. Growth is primarily driven by rising disposable incomes in the UAE and Saudi Arabia, expanding modern retail infrastructure, and government-led wellness initiatives. High expatriate populations in Gulf countries contribute to the demand for imported premium supplement brands. In Africa, South Africa represents the largest market due to relatively advanced retail networks and increasing consumer awareness of nutritional supplementation. Long-term growth in this region will depend on regulatory harmonization and distribution expansion.

Key Players in the Gummy Supplements Market

- Church & Dwight Co., Inc.

- Bayer AG

- Pharmavite LLC

- Nature's Way Products, LLC

- Nestlé S.A.

- Haleon plc

- Unilever PLC

- Glanbia plc

- Herbaland Naturals Inc.

- Jamieson Wellness Inc.

- Life Science Nutritionals

- Vitafusion

- SmartyPants Vitamins

- Olly Public Benefit Corporation

- Nature Made