Green Screen Production Kit Market Size

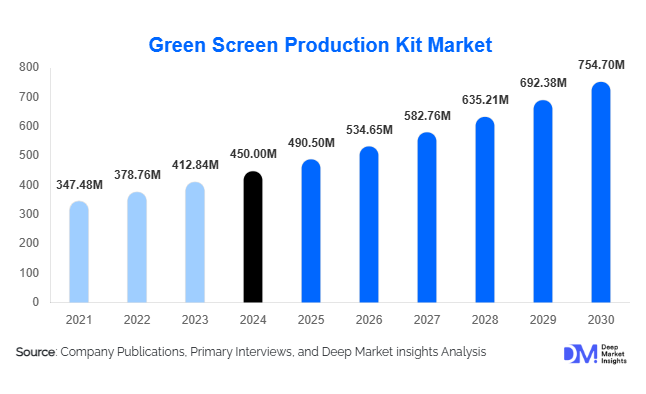

According to Deep Market Insights, the global green screen production kit market size was valued at USD 450 million in 2025 and is projected to grow from USD 490.5 million in 2026 to reach USD 754.70 million by 2031, expanding at a CAGR of 9% during the forecast period (2026–2031). The green screen production kit market growth is primarily driven by the rising demand for professional-quality content creation, the expansion of live streaming and influencer-driven media, and technological advances in chroma key software and portable kit designs.

Key Market Insights

- Professional-grade kits dominate global revenue due to their use in film, television, and commercial studio applications, accounting for over 30% of the market in 2025.

- Collapsible fabric green screens remain the material of choice, capturing nearly 40% of global demand because of their portability, durability, and superior chroma key performance.

- Content creators, streamers, and influencers represent the fastest-growing end-user segment, contributing around 25–30% of 2025 revenue and expanding rapidly with social media and gaming platforms.

- Online and e-commerce channels hold about 50% of the distribution share, driven by ease of access, competitive pricing, and global reach.

- North America dominates the market with nearly 40% of the global share in 2025, supported by strong film and streaming industries, while Asia-Pacific is the fastest-growing region, fueled by India and China’s content economies.

- Sustainability and eco-friendly materials are emerging as differentiators, with brands experimenting with recycled fabrics and low-VOC backdrops.

Green Screen Production Kit Market Trends

Integration with Virtual Production and AR/VR

Green screen kits are increasingly being integrated with real-time rendering engines and AR/VR tools. While LED walls dominate high-end virtual production, green screens offer a cost-effective alternative for small studios and indie creators. Bundled solutions combining hardware, tracking systems, and software plugins are emerging, helping bridge the affordability gap in immersive content creation. This trend is particularly relevant for advertising, gaming, and streaming industries, which require quick turnaround on visually rich content.

Expansion into Education and Corporate E-Learning

Educational institutions and businesses are adopting green screen kits to enhance virtual classrooms, training sessions, and corporate presentations. Universities and schools are setting up media labs for digital education, while enterprises use green screens to create polished webinars and hybrid events. The growing adoption of e-learning, accelerated during the pandemic, continues to fuel this segment, with simplified, modular kits designed for non-professional users gaining traction.

Portable and Collapsible Kit Innovation

Manufacturers are focusing on lightweight, collapsible, and portable kit designs for influencers, traveling professionals, and mobile studios. Foldable backdrops, LED lighting kits, and quick-setup stands are addressing the needs of small creators with limited space. This portability trend is also feeding into the rental and subscription economy, offering flexible access to production-quality equipment without the upfront cost burden.

Green Screen Production Kit Market Drivers

Rising Demand for Digital Content Creation

The surge in video-based platforms such as YouTube, TikTok, and Twitch has accelerated the adoption of green screen kits. Content creators seek tools to improve visual storytelling, allowing seamless background replacement and immersive effects. Influencer marketing and the creator economy are critical growth engines, with millions of small-scale users demanding affordable kits.

Advancements in Materials, Lighting, and Software

Wrinkle-resistant fabrics, collapsible designs, and LED lighting systems with adjustable temperature settings are making green screens more user-friendly. AI-powered chroma key software has reduced the complexity of background removal, enabling high-quality results even for non-professional users. Together, these innovations are reducing technical barriers and broadening adoption.

Hybrid Work and Virtual Events Boom

Post-pandemic, green screen kits are widely used in remote work, hybrid events, webinars, and digital corporate communications. Businesses demand higher-quality video production for marketing, HR training, and product demos. This driver is creating new commercial demand outside the entertainment sector.

Green Screen Production Kit Market Restraints

High Cost of Professional Setups

While entry-level kits are affordable, professional-grade kits with advanced lighting, durable fabrics, and large backdrops remain costly, often running into thousands of dollars. This pricing limits accessibility for small creators and budget-sensitive markets, slowing adoption in emerging economies.

Technical Skills Barrier

Effective green screen use requires knowledge of lighting, spacing, and post-production editing. Poor setup can cause shadowing, color spill, and low-quality output. The steep learning curve and availability of alternatives such as AI-driven background removal software act as restraints for market penetration.

Green Screen Production Kit Market Opportunities

Emerging Market Expansion

India, China, and Brazil are rapidly expanding their creator economies. Affordable kits distributed through e-commerce platforms in these regions can unlock mass adoption. Localization of training and after-sales support is an untapped opportunity for manufacturers.

Sustainable Product Development

Eco-friendly kits using recycled fabrics, biodegradable frames, and low-emission manufacturing are gaining appeal among environmentally conscious buyers. Sustainability certifications can differentiate brands in premium markets such as Europe and North America, creating long-term competitive advantage.

Rental and Subscription Models

Equipment rental services and subscription-based access to kits are lowering entry barriers for smaller users. These models allow creators to access high-quality kits on a flexible basis, supporting wider adoption in both professional and amateur segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 450 Million |

| Market Size in 2026 | USD 490.5 Million |

| Market Size in 2031 | USD 754.70 Million |

| CAGR | 9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Professional green screen kits dominate the market, accounting for around 30–35% of 2025 revenue. These kits are widely used in film, television, and high-end studio applications where durability, chroma consistency, and advanced lighting setups are critical. Collapsible fabric kits, while less expensive, are experiencing fast growth, appealing to mobile content creators and influencers. Lighting kits and accessories also represent a strong sub-segment, as proper illumination remains essential for effective chroma keying.

Application Insights

Live streaming and digital content creation accounted for nearly 35% of global revenue in 2025. This segment is expanding rapidly with the proliferation of gaming, influencer marketing, and short-form video content. Film and television production remains a significant application, particularly in North America and Europe, but the fastest growth is coming from streaming, e-learning, and corporate virtual events. Advertising agencies are increasingly leveraging green screens for creative campaigns, further diversifying use cases.

Distribution Channel Insights

Online and e-commerce platforms dominate the distribution landscape, representing about 50% of global sales in 2025. Platforms such as Amazon, B&H, and manufacturer-direct channels have become the go-to for small and medium buyers. Specialty photography and video stores maintain relevance for professional buyers, while rental services are growing as an alternative access point in major cities. Direct-to-consumer models are rising as brands strengthen their digital presence and expand globally through online marketing.

End-User Insights

Content creators, streamers, and influencers are the fastest-growing end-user group, accounting for around 25–30% of 2025 demand. Professional studios still generate the highest revenue share, particularly in developed regions, but the sheer volume of small creators globally is reshaping the market. Educational institutions and corporate users represent emerging growth areas, supported by hybrid work and remote learning trends.

Explore more data points, trends and opportunities Download Free Sample Report

Green Screen Production Kit Market Segmentations

By Kit Type

- Portable

- Studio

- Chroma-key Fabric

- Paint

By User

- Pro Studios

- Indie Creators

- Education

By Accessory

- Backdrops

- Lighting

- Software Bundles

Regional Insights

North America

North America held approximately 40% of the global market in 2025, led by the United States. Strong demand from Hollywood, streaming platforms, and influencer-driven industries ensures stable growth. Universities and businesses also contribute to sustained adoption, supported by high disposable incomes and advanced distribution networks.

Europe

Europe accounts for 15–20% of global demand, with the U.K., Germany, and France leading. The region emphasizes sustainability and high-quality products, with buyers increasingly looking for eco-friendly kits. Growth is steady, supported by established media industries and corporate adoption.

Asia-Pacific

Asia-Pacific represents 25–30% of the market in 2025 and is the fastest-growing region. China, India, Japan, and South Korea drive demand, supported by booming creator economies, rising internet penetration, and government initiatives to support media industries. APAC is projected to grow at a double-digit CAGR through 2031.

Latin America

Latin America holds 5–8% of global demand, with Brazil and Mexico being key markets. Content creation and influencer-driven adoption are increasing, though price sensitivity remains a challenge. Growing e-commerce availability is accelerating adoption across the region.

Middle East & Africa

MEA accounts for 5–7% of demand, led by the UAE, Saudi Arabia, and South Africa. Investments in creative industries and growing digital content ecosystems are supporting adoption. While smaller in scale, this region is experiencing steady growth in green screen kit demand, particularly for corporate and event applications.

Key Players in the Green Screen Production Kit Market

- Elgato

- Neewer

- Savage Universal

- Westcott

- Lastolite (Manfrotto)

- Fotodiox

- Fovitec

- Impact Studio Lighting

- Andoer

- Kate Backdrop

- HamiltonBuhl

- Emart

- LimoStudio

- Julius Studio

- UBeesize

Recent Developments

- In March 2025, Elgato launched an upgraded collapsible green screen with wrinkle-resistant fabric and an integrated frame, targeting streamers and home studios.

- In February 2025, Neewer introduced an LED lighting bundle with chroma key compatibility, aiming to simplify setup for amateur creators.

- In January 2025, Westcott announced an eco-friendly green screen series made with recycled fabrics, targeting sustainability-conscious buyers in Europe and North America.