Grain-Free Pet Foods Market Size

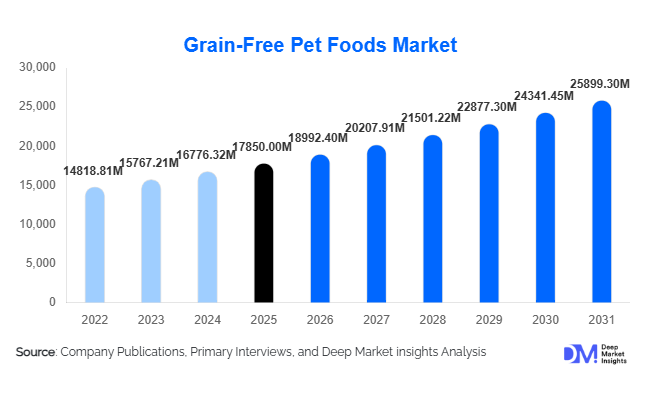

According to Deep Market Insights, the global grain-free pet foods market size was valued at USD 17,850 million in 2025 and is projected to grow from USD 18,992.40 million in 2026 to reach USD 25,899.30 million by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The grain-free pet foods market growth is primarily driven by rising pet humanization, growing awareness of dietary sensitivities in companion animals, and increasing demand for premium and functional pet nutrition. Pet owners are actively seeking high-protein, limited-ingredient, and allergen-conscious formulations, positioning grain-free products as a core segment within the broader premium pet food industry.

Key Market Insights

- Dogs account for nearly 65% of total market revenue, driven by higher consumption volumes and stronger adoption of premium diets.

- North America leads with approximately 38% market share in 2025, supported by strong premiumization and high pet ownership rates.

- Asia-Pacific is the fastest-growing region, expanding at an estimated CAGR of over 8%, fueled by rising middle-class pet adoption.

- Dry grain-free food dominates product type share (about 48%), owing to convenience and shelf stability.

- Online retail and D2C channels are rapidly expanding, with e-commerce accounting for more than 25% of premium pet food sales in developed markets.

- Animal-based protein formulations lead with around 62% share, reflecting consumer preference for high-protein diets.

What are the latest trends in the grain-free pet foods market?

Functional and Limited-Ingredient Formulations

Grain-free pet food is increasingly being combined with functional health claims such as digestive support, joint mobility, weight management, and skin and coat enhancement. Limited-ingredient diets (LID) are gaining traction among pet owners concerned about allergies and food sensitivities. Manufacturers are incorporating probiotics, omega fatty acids, glucosamine, and natural antioxidants to enhance perceived health benefits. The integration of novel proteins such as duck, venison, bison, and even insect-based proteins is also expanding product differentiation. These innovations are helping brands command premium price points while strengthening consumer loyalty.

Premiumization and Clean-Label Positioning

Consumers are increasingly scrutinizing ingredient labels, favoring products that are non-GMO, organic-certified, and free from artificial preservatives. Clean-label positioning has become a competitive differentiator, particularly in North America and Europe. Transparency in sourcing and sustainable packaging is influencing purchase decisions, especially among millennial and Gen Z pet owners. Brands are leveraging storytelling around ethical sourcing and traceability, positioning grain-free diets as a natural and holistic feeding solution.

What are the key drivers in the grain-free pet foods market?

Rising Pet Humanization

Pets are increasingly viewed as family members, resulting in higher per-pet spending on nutrition. Premium and super-premium products now account for a significant portion of total pet food expenditure in developed markets. Grain-free diets are strongly associated with premium positioning, reinforcing steady demand growth globally. Higher disposable incomes and lifestyle changes in urban households are further accelerating adoption.

Growth in E-Commerce and Subscription Models

The expansion of online retail has significantly improved accessibility to specialized grain-free products. Subscription-based feeding plans and direct-to-consumer models allow companies to build recurring revenue streams while gathering consumer insights for targeted innovation. This digital shift is especially impactful in the United States, the United Kingdom, and China, where online pet care purchases are expanding at double-digit rates.

What are the restraints for the global market?

Regulatory Scrutiny and Nutritional Debates

Regulatory agencies in some regions have examined potential links between grain-free diets and canine heart conditions. Although scientific conclusions remain inconclusive, consumer concerns and increased labeling requirements have created uncertainty. Brands must invest in clinical research and transparent communication to mitigate reputational risks.

Higher Price Sensitivity in Emerging Markets

Grain-free pet foods typically retail 15–35% higher than conventional products due to premium protein ingredients. In developing markets such as India and parts of Southeast Asia, price sensitivity can limit widespread adoption. Companies must balance premium positioning with localized pricing strategies to capture broader demand.

What are the key opportunities in the grain-free pet foods industry?

Emerging Market Penetration

Countries such as China, Brazil, Mexico, and India present significant growth potential. Urbanization, increasing disposable income, and rising companion animal adoption are driving premium pet food demand. Companies that localize flavor profiles and optimize price tiers can secure early-mover advantages in these high-growth markets.

Therapeutic and Veterinary-Backed Nutrition

Integration of veterinary science into grain-free formulations presents a high-margin opportunity. Specialized diets targeting weight control, renal health, or digestive sensitivities can capture a growing segment of health-conscious pet owners. Partnerships with veterinary clinics and pet hospitals enhance brand credibility and recurring demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 17850 Million |

| Market Size in 2026 | USD 18992.40 Million |

| Market Size in 2031 | USD 25899.30 Million |

| CAGR | 6.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Dry grain-free pet food remains the leading product segment, accounting for approximately 48% of total market revenue in 2025. Its dominance is primarily driven by cost efficiency, longer shelf life, bulk packaging advantages, and ease of storage and transportation. For manufacturers and retailers, dry formats offer better inventory management and lower logistics costs compared to wet alternatives. Additionally, dry grain-free kibble is increasingly formulated with high-protein and functional additives such as probiotics and omega fatty acids, further strengthening its value proposition. The segment’s growth is also supported by subscription-based online sales, where larger bag sizes are preferred by dog owners seeking convenience and recurring deliveries.

Wet grain-free food holds the second-largest share, driven by superior palatability and higher moisture content, making it particularly suitable for senior pets and cats. Demand for wet formats is growing in urban households where smaller pet sizes and premium feeding habits are more prevalent. Meanwhile, semi-moist and grain-free treats are expanding steadily, especially in premium and super-premium tiers. The humanization trend has fueled demand for indulgent yet health-oriented snacks, boosting treat innovation with functional claims such as dental care and joint support.

Pet Type Insights

Dogs dominate the grain-free pet foods market with approximately 65% share in 2025, making them the leading revenue-generating segment. The primary driver of this dominance is higher per-pet consumption volume compared to cats and other animals. Dogs also exhibit a higher incidence of reported food sensitivities, encouraging owners to shift toward grain-free formulations. Larger breed sizes in North America and Europe further amplify consumption volumes. In addition, premiumization is more pronounced among dog owners, who are willing to pay for high-protein and limited-ingredient diets.

Cats represent the second-largest segment, supported by increasing urban adoption and rising demand for wet grain-free formulations. The growth of apartment living, particularly in Asia-Pacific and Europe, has contributed to higher cat ownership rates. Smaller mammals and exotic pets remain niche segments but are gradually expanding as specialty retailers broaden their grain-free product offerings.

Distribution Channel Insights

Pet specialty stores account for roughly 30% of global sales in 2025, making them the leading distribution channel. Their dominance is driven by knowledgeable staff, premium product assortments, and consumer trust in curated nutrition guidance. Specialty stores often introduce new grain-free SKUs earlier than mass retailers, strengthening their competitive positioning.

However, online retail is the fastest-growing channel and is projected to outpace all other channels through 2031. Growth drivers include convenience, subscription-based replenishment models, competitive pricing, and access to a broader product range. E-commerce penetration is particularly high in the United States, China, and the United Kingdom. Veterinary clinics are also emerging as a key channel for therapeutic grain-free diets, particularly those targeting allergies, obesity, and digestive disorders.

Price Tier Insights

Premium grain-free products hold approximately 40% of the total market share in 2025, positioning this tier as the leading revenue contributor. The growth driver for this segment is its ability to balance advanced nutritional claims with relative affordability compared to super-premium offerings. Consumers increasingly perceive premium grain-free products as offering better ingredient transparency and health benefits.

The super-premium and holistic segments are expanding at a faster rate, particularly in North America and Western Europe. These products emphasize organic certifications, novel proteins, and sustainable sourcing, appealing to affluent consumers willing to pay higher prices. Meanwhile, mid-range offerings are gaining traction in emerging markets, where price sensitivity remains a key consideration.

Explore more data points, trends and opportunities Download Free Sample Report

Grain-Free Pet Foods Market Segmentations

By Product Type

- Dry Grain-Free Pet Food

- Wet Grain-Free Pet Food

- Semi-Moist Grain-Free Food

- Grain-Free Treats & Snacks

By Pet Type

- Dogs

- Cats

- Small Mammals

- Birds

- Reptiles & Exotic Pets

By Distribution Channel

- Pet Specialty Stores

- Supermarkets & Hypermarkets

- Veterinary Clinics

- Online Retail / E-commerce

- Direct-to-Consumer (D2C)

By Price Tier

- Economy

- Mid-Range

- Premium

- Super-Premium / Holistic

By Ingredient Source

- Animal-Based Protein

- Novel Protein

- Plant-Based / Vegan

- Limited-Ingredient Formulas

Regional Insights

North America

North America leads the global grain-free pet foods market, accounting for approximately 38% of total revenue in 2025. The United States represents the dominant contributor, driven by high pet ownership rates, strong premiumization trends, and advanced retail infrastructure. Consumer awareness regarding pet allergies and ingredient transparency is particularly high, supporting sustained demand for grain-free diets. The region also benefits from robust e-commerce penetration and subscription-based pet food models. Canada exhibits strong per-capita spending on pet nutrition, further reinforcing regional growth. Continued product innovation and R&D investments by major manufacturers are expected to sustain North America's leadership position.

Europe

Europe accounts for approximately 28% of the global market share, led by the United Kingdom, Germany, and France. Growth in the region is driven by strict labeling standards, high consumer preference for natural and clean-label products, and increasing cat ownership in urban centers. Western European consumers demonstrate a strong interest in sustainable and ethically sourced ingredients, encouraging innovation in grain-free formulations. Additionally, rising demand for premium wet cat food is supporting segment expansion across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at an estimated CAGR of over 8% during the forecast period. China is the primary growth engine, fueled by rapid urbanization, rising disposable incomes, and expanding e-commerce channels. Premium imported brands are particularly popular among Chinese consumers seeking quality assurance. Japan and Australia represent mature markets characterized by high product quality expectations and established premium segments. India and Southeast Asian countries are emerging growth pockets, driven by rising pet adoption and growing awareness of specialized nutrition.

Latin America

Latin America holds a modest but expanding share of the global market, with Brazil and Mexico as leading contributors. Growth drivers include rising middle-class income levels, increasing dog ownership, and the gradual premiumization of pet food consumption. Modern retail expansion and greater availability of imported premium brands are supporting the adoption of grain-free formulations. While price sensitivity remains a constraint, urban markets are demonstrating stronger uptake of premium offerings.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth, led by the United Arab Emirates and South Africa. Increasing disposable incomes, expansion of organized pet retail chains, and growing awareness of pet health are key growth drivers. The UAE, in particular, benefits from a high expatriate population with strong purchasing power. In South Africa, rising urbanization and increasing availability of international brands are supporting the gradual adoption of grain-free diets. Although the region’s overall share remains smaller compared to North America and Europe, long-term growth potential is supported by improving retail infrastructure and evolving consumer preferences.

Key Players in the Grain-Free Pet Foods Market

- Mars Petcare

- Nestlé Purina PetCare

- Hill's Pet Nutrition

- General Mills

- The J.M. Smucker Company

- Blue Buffalo

- WellPet

- Diamond Pet Foods

- Canidae

- Champion Petfoods

- Colgate-Palmolive

- Spectrum Brands

- United Petfood

- Farmina Pet Foods

- Nature's Variety