Golf Tourism Market Size

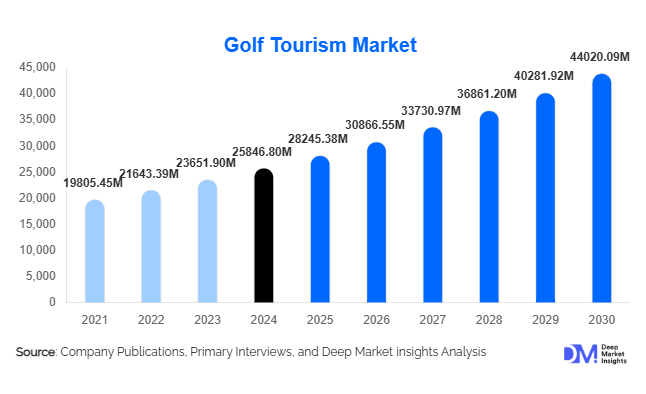

According to Deep Market Insights, the global golf tourism market size was valued at USD 25,846.80 million in 2025 and is projected to grow from USD 28,245.38 million in 2026 to reach USD 44,020.09 million by 2031, expanding at a CAGR of 9.28% during the forecast period (2026–2031). Growth is driven by rising participation in golf among younger demographics, expanding golf resort infrastructure, increasing preference for premium leisure travel, and heightened demand for integrated sports tourism experiences worldwide.

Key Market Insights

- International golf tourism dominates the market, contributing the highest revenue share due to premium spending on long-haul travel, luxury resorts, and tournament attendance.

- Golf resorts and integrated luxury hotels account for over 60% of total accommodation-related spending, supported by bundled packages and high-value amenities.

- North America leads the global golf tourism market with strong domestic participation and outbound travel to Europe and the Asia-Pacific.

- Asia-Pacific remains the fastest-growing region, driven by growing course development in Vietnam, Thailand, Japan, and South Korea.

- Technology integration is reshaping golf tourism through VR course previews, AI-powered itinerary planning, and dynamic online booking platforms.

- Government-backed sports tourism initiatives in the Middle East and Southeast Asia are accelerating infrastructure investment and global tournament hosting.

Golf Tourism Market Trends

Growth of Integrated Golf & Luxury Lifestyle Resorts

Golf tourism is rapidly shifting toward integrated resort ecosystems that combine golf with luxury hospitality, wellness offerings, adventure activities, and curated leisure experiences. Travelers increasingly prefer destinations where golf is seamlessly blended with premium lifestyle amenities such as spas, fine dining, heritage tours, and family-friendly recreation. Countries including Thailand, Vietnam, the UAE, Mexico, and Portugal are heavily investing in multi-course resort hubs that enhance visitor engagement and extend stay durations. This convergence of luxury lifestyle and sports tourism is expanding the appeal of golf travel across affluent households and corporate groups.

Technology-Enhanced Golf Travel Experiences

Digital transformation is redefining consumer engagement in golf tourism. VR-enabled previews allow travelers to “test” courses before booking, while AI-driven booking platforms curate personalized itineraries based on skill level, climate preference, or playing style. Mobile apps offer real-time tee-time updates, weather insights, swing analytics, and GPS course mapping. Resorts are adopting digital check-in, smart carts, and virtual coaching tools, appealing strongly to Millennials and tech-savvy travelers. Blockchain-backed booking systems are also emerging, ensuring transparent pricing and secure payments for international travelers.

Golf Tourism Market Drivers

Rise of Global Sports Tourism

Sports tourism has emerged as one of the fastest-growing sectors in global travel, and golf is at the center of this expansion. Travelers increasingly combine active participation with premium holiday experiences. Major tournaments such as the Ryder Cup, PGA Tour events, and the European Tour attract significant international attendance. Governments and private operators are promoting golf tourism as a strategic component of national tourism branding, fueling both inbound and outbound travel.

Growing Participation Among Younger Golfers

A generational shift is underway, with younger golfers (18–40 years) adopting golf as a recreational lifestyle sport. The popularity of urban golf experiences, indoor golf simulators, TopGolf-style venues, and hybrid entertainment formats has expanded the base of prospective golf travelers. Younger demographics prefer experiential travel, increasing demand for golf holidays integrated with nightlife, adventure, and cultural exploration. This has driven strong growth in hybrid leisure-golf travel packages across Asia, Europe, and North America.

Golf Tourism Market Restraints

High Cost of Golf Travel

Golf tourism remains a premium travel category with substantial costs for flights, green fees, resort stays, and equipment rentals. This restricts accessibility to affluent and upper-middle-income travelers, limiting mass adoption. Seasonal demand peaks also lead to higher airfare and accommodation prices, further amplifying cost barriers. The cost of professional coaching and tournament attendance adds additional expense for specialized travelers.

Seasonality and Climate Challenges

Golf is highly dependent on climate conditions, and major destinations face seasonal variations that impact playability. Unpredictable weather patterns, rising global temperatures, and climatic disruptions reduce course availability during peak periods. Regions with extreme climates, such as the Middle East or Northern Europe, struggle with off-season demand volatility, affecting year-round revenue consistency for operators.

Golf Tourism Market Opportunities

Expansion of Golf Infrastructure in Emerging Destinations

Countries such as Vietnam, Thailand, Saudi Arabia, South Korea, India, and South Africa are aggressively developing new championship courses and integrated golf resorts. Government-led tourism diversification strategies are driving major investments in premium golf infrastructure. Partnerships between international golf brands and local tourism boards are accelerating destination development, creating high-growth markets for inbound golf travelers.

Digitization of Golf Travel and AI-Driven Personalization

Specialized digital platforms represent a significant opportunity to streamline the golf travel planning process. AI-powered systems can customize itineraries based on player skills, preferred terrain, weather preferences, and time availability. Enhanced digital visibility, dynamic pricing tools, and blockchain-secured bookings create transparency and convenience. Travel operators integrating such technologies can significantly expand market reach and improve traveler retention.

Product Type Insights

International golf tourism accounts for the largest share of the industry, representing 58% of the global market in 2025. Premium experiences, high-value spending, and demand for iconic courses in the U.S., Scotland, Spain, Portugal, Japan, and Thailand drive this dominance. Domestic golf tourism remains strong within large golfing nations such as the U.S., Japan, South Korea, and the U.K., fueled by weekend getaways and short-haul regional travel. Hybrid leisure-golf travel options are gaining traction, especially among families and younger tourists seeking multi-activity vacation opportunities.

Application (End-Use) Insights

Leisure golf travel leads market demand with 66% share in 2025, supported by the popularity of golf vacations, resort stays, and amateur recreational playing. Corporate golf travel and MICE events represent the fastest-growing segment, expanding at an estimated 8–9% CAGR through 2031. Professional and semi-professional golfers' travel also contributes significantly, driven by global tournaments and cross-border championship circuits. New applications, such as golf academies, virtual coaching travel, and integrated wellness-golf programs, are emerging as complementary growth avenues.

Distribution Channel Insights

Indirect bookings, including specialized golf travel operators and OTAs, dominate with 62% market share. These channels offer curated packages, equipment rental options, coordinated tee times, and personalized arrangements that appeal to international travelers. Direct-to-consumer (D2C) resort portals are growing steadily as hotels and golf resorts enhance their digital platforms with interactive course maps, AI-driven recommendations, and dynamic pricing models. Social media, influencer marketing, and real-time testimonials increasingly influence booking patterns, especially among younger demographics.

Traveler Type Insights

Leisure golfers form the largest traveler category, driving both domestic and international tourism flows. Business-corporate travelers are expanding their share due to rising demand for executive retreats and incentive-led golfing events. Solo golfers and small groups are increasingly opting for flexible packages and experiential itineraries, including back-to-back course tours and pro-coaching add-ons. Family travelers represent a steady growth segment as integrated resorts add childcare, wellness amenities, and family-friendly recreational activities alongside golf.

Age Group Insights

Travelers aged 35–54 years represent the largest share (49%) of global golf tourism spending, driven by strong purchasing power and affinity for premium travel. The 55+ segment remains highly influential due to higher play frequency and preference for extended stay golf vacations. Younger travelers (18–34 years) are the fastest-growing demographic, catalyzed by entertainment-driven golf formats, social media visibility, and hybrid vacation preferences that blend sport with adventure, nightlife, and cultural exploration.

| By Type of Tourism | By Booking Channel | By Tourist Profile | By Age Group | By Travel Purpose |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds the largest share of the global golf tourism market at 32% in 2025. The United States is the world’s largest golf destination, featuring over 16,000 courses and numerous PGA tournaments that attract domestic and international tourists. Outbound travel to Scotland, Ireland, Spain, Japan, and Thailand remains strong, with U.S. travelers favoring premium multi-course itineraries.

Europe

Europe represents 28% of global golf tourism, anchored by iconic destinations such as Scotland, Portugal, Spain, and Ireland. Europe benefits from favorable weather, historic championship courses, and strong government support for sports tourism. Spain and Portugal account for nearly 40% of Europe’s inbound golf travelers, supported by year-round playability and luxury golf resorts.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at a projected 9.3% CAGR. Japan, South Korea, Vietnam, and Thailand are the leading destinations, with Vietnam showing exceptional growth due to aggressive infrastructure development and global branding efforts. China’s rising middle class is also influencing outbound golf travel to Thailand, Malaysia, and Japan.

Latin America

Latin America is gradually expanding its presence in global golf tourism, with Mexico emerging as a major international destination. Resorts in Cancun, Los Cabos, and the Riviera Maya attract significant U.S. and Canadian tourist inflow. The Dominican Republic also stands out as a fast-growing Caribbean golf hub.

Middle East & Africa

The Middle East, led by the UAE and Saudi Arabia, is investing heavily in golf as part of broader sports tourism strategies. Dubai and Abu Dhabi host internationally recognized courses and tournaments. Africa’s demand is concentrated in South Africa and Mauritius, with strong ties to European outbound travelers.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Golf Tourism Market

- Golfbreaks

- PerryGolf

- Your Golf Travel

- Premier Golf

- Golfasian

- Links Golf Ireland

- Carr Golf

- PGA TOUR Experiences

- Tee Times USA

- Haversham & Baker

- Scotland Golf Travel

- Orchid Golf Tours

- Golf Tours International

- Chaka Travel

- International Golf Travel Partners (IGTP)

Recent Developments

- In 2025, Golfasian announced expansion into new Southeast Asian routes, offering multi-country golf itineraries across Thailand, Vietnam, and Malaysia.

- In 2025, Golfbreaks launched an AI-enabled booking platform integrating real-time tee-time availability, weather forecasts, and dynamic package pricing.

- In 2025, Premier Golf partnered with multiple European resorts to create premium Ryder Cup-themed travel experiences with exclusive course access.