Golf Shaft Market Size

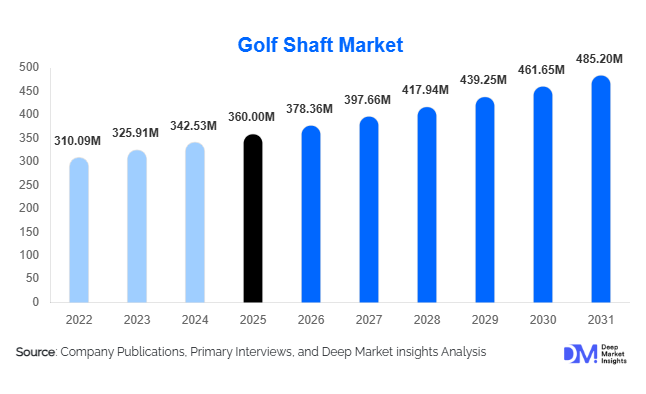

According to Deep Market Insights, the global golf shaft market size was valued at USD 360 million in 2025 and is projected to grow from USD 378.36 million in 2026 to reach USD 485.20 million by 2031, expanding at a CAGR of 5.1% during the forecast period (2026–2031). The golf shaft market growth is primarily driven by the increasing participation in golf worldwide, technological advancements in graphite and carbon composite shaft materials, and rising demand for customized golf equipment that enhances swing speed, accuracy, and ball control.

Golf shafts are one of the most critical performance components in golf clubs, influencing swing dynamics, ball trajectory, and player comfort. As golfers increasingly seek personalized equipment tailored to their playing style, demand for advanced shaft technologies, including lightweight graphite shafts, multi-material composite shafts, and vibration-dampening designs, is growing rapidly. Professional endorsements and the expansion of custom club fitting services are also influencing purchasing decisions in the golf shaft industry.

North America currently dominates the market due to its large base of golfers, established golf infrastructure, and strong retail networks. Meanwhile, the Asia-Pacific is emerging as the fastest-growing region as golf participation rises across countries such as Japan, South Korea, China, and Thailand. Premiumization trends within golf equipment, coupled with innovation in carbon fiber materials and advanced shaft engineering, are expected to support steady market expansion over the coming decade.

Key Market Insights

- Graphite shafts dominate the global market due to their lightweight design, higher swing speed potential, and superior vibration dampening compared to steel shafts.

- North America remains the largest regional market, driven by a strong golf culture, high equipment spending, and widespread availability of professional club fitting services.

- Asia-Pacific is the fastest-growing region, supported by increasing golf participation and rising disposable income in countries such as China, South Korea, and Japan.

- Premium custom shafts are gaining popularity, as golfers increasingly seek personalized performance improvements through advanced shaft fitting technologies.

- Technological innovations in carbon fiber composites are enabling lighter, stronger shafts with improved energy transfer and durability.

- Online retail and direct-to-consumer sales channels are expanding rapidly, allowing golf equipment brands to reach amateur and recreational players globally.

What are the latest trends in the golf shaft market?

Growing Popularity of Custom Club Fitting

Custom club fitting has emerged as one of the most influential trends in the golf shaft market. Modern fitting centers use launch monitors, high-speed cameras, and AI-based swing analytics to recommend shafts tailored to a player’s swing speed, launch angle, and ball spin characteristics. This shift toward personalized equipment has significantly increased demand for premium shafts, particularly among serious amateur golfers and professionals.

Golf retailers and pro shops are investing heavily in advanced fitting technologies to enhance customer experience and improve performance outcomes. By providing precise recommendations on shaft flex, weight, and torque, custom fitting services help golfers maximize distance and accuracy. As awareness of performance benefits continues to grow, custom fitting is expected to become a standard purchasing step for golfers worldwide.

Advancements in Composite Materials and Shaft Engineering

Material innovation is reshaping the golf shaft industry. Carbon fiber composites, nano-resin bonding, and hybrid multi-layer constructions are enabling manufacturers to produce shafts that are lighter, stronger, and more responsive. These materials improve energy transfer during swings while reducing vibration, enhancing both performance and comfort.

Manufacturers are increasingly experimenting with multi-material shaft structures that combine carbon fiber layers with metal reinforcements for optimal stiffness and durability. These technological advancements are particularly popular in premium driver shafts, where even minor performance improvements can significantly impact swing speed and ball distance.

What are the key drivers in the golf shaft market?

Increasing Global Golf Participation

The steady growth of golf participation worldwide is a major driver of the golf shaft market. The sport has expanded significantly beyond traditional markets such as the United States and the United Kingdom into emerging regions including Asia-Pacific and the Middle East. Golf tourism, indoor golf simulators, and driving range facilities are introducing new players to the sport, increasing demand for golf equipment.

As the number of active golfers increases, equipment replacement cycles create recurring demand for golf shafts. Amateur players typically upgrade their clubs every few years, while professional players often experiment with different shaft configurations to optimize performance during tournaments.

Rising Demand for High-Performance Golf Equipment

Golfers are increasingly seeking high-performance equipment that enhances distance, control, and consistency. Modern shafts are engineered to optimize swing dynamics by controlling torque, flex, and kick point characteristics. These innovations enable players to generate greater clubhead speed and improved ball trajectory.

Premium golf shafts, particularly those used in drivers and fairway woods, have gained popularity among amateur enthusiasts seeking tour-level performance. This trend has encouraged manufacturers to invest heavily in research and development to produce technologically advanced shaft designs.

What are the restraints for the global market?

High Cost of Premium Shafts

Premium graphite shafts can cost between USD 150 and USD 350 per unit, making them significantly more expensive than standard shafts included with entry-level golf clubs. This price barrier limits adoption among recreational golfers, who often rely on factory-installed shafts rather than aftermarket upgrades.

While professional players and serious enthusiasts frequently invest in custom shafts, casual golfers may perceive these products as unnecessary luxury purchases. As a result, premium shaft manufacturers must continuously demonstrate measurable performance benefits to justify higher prices.

Limited Market Size Compared to Broader Golf Equipment Industry

The golf shaft segment represents only a small portion of the broader golf equipment industry, which includes golf clubs, balls, apparel, and accessories. Since shafts are often integrated into golf clubs during manufacturing, standalone aftermarket shaft purchases remain limited to advanced players and customization services.

This niche demand structure can constrain overall market growth, making the industry highly dependent on the performance-driven segment of the golf equipment market.

What are the key opportunities in the golf shaft industry?

Expansion of Golf Participation in Emerging Markets

Emerging markets such as China, Thailand, Vietnam, and the United Arab Emirates present significant opportunities for golf shaft manufacturers. These regions are investing heavily in golf tourism infrastructure, including luxury resorts, golf courses, and professional training facilities.

As new golfers enter the sport in these regions, demand for beginner-friendly graphite shafts and mid-range golf equipment is expected to increase. Manufacturers that establish strong distribution networks in these markets can benefit from long-term demand growth.

Integration of Smart Technology in Golf Equipment

The integration of sensor-based technology into golf equipment represents an emerging opportunity for the industry. Smart shafts equipped with motion sensors and wireless connectivity can capture swing data and transmit performance metrics to mobile applications.

These technologies enable golfers to analyze swing mechanics and track improvements over time. As sports analytics and digital coaching tools become more popular, smart shafts could create new revenue streams for manufacturers and enhance product differentiation.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 360 Million |

| Market Size in 2026 | USD 378.36 Million |

| Market Size in 2031 | USD 485.20 Million |

| CAGR | 5.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Material Type Insights

Graphite shafts represent the leading segment in the global golf shaft market, accounting for nearly 58% of total market revenue in 2025. The dominance of graphite shafts is primarily attributed to their lightweight construction and superior energy transfer characteristics, which enable golfers to achieve higher swing speeds and longer ball distances. These shafts are particularly preferred for drivers, fairway woods, and hybrid clubs, where maximizing launch distance and ball speed is critical. Additionally, advancements in carbon fiber layering technology and nano-resin bonding techniques have significantly enhanced graphite shaft durability and torsional stability, making them increasingly popular among both amateur and professional golfers.

Steel shafts continue to maintain a strong presence in the market, particularly in iron clubs, due to their consistent flex profile, durability, and relatively lower cost compared to graphite alternatives. Steel shafts provide greater control and shot accuracy, which is why they remain widely used by professional players and advanced golfers who prioritize precision over swing speed. Meanwhile, hybrid composite shafts are emerging as a promising innovation segment. These shafts integrate multiple materials such as carbon fiber, titanium mesh, and steel reinforcement layers to optimize flex distribution, vibration dampening, and structural strength. As manufacturers continue to invest in advanced materials engineering, hybrid shafts are expected to gain increasing adoption in high-performance golf clubs.

Club Type Insights

Iron shafts currently represent the largest segment within the golf shaft market, accounting for approximately 41% of total global demand in 2025. The leading position of iron shafts is largely driven by the frequent usage of iron clubs during gameplay. Golfers rely on iron clubs for a wide range of shots, including approach shots, fairway play, and short-range accuracy shots, which leads to higher wear and tear and ultimately more frequent replacement cycles. This consistent utilization creates stable demand for iron shafts across both amateur and professional golfer segments.

Driver shafts form the second-largest segment and are experiencing significant growth due to the increasing emphasis on maximizing driving distance and swing efficiency. Premium driver shafts engineered with advanced graphite composites and multi-layer carbon structures are gaining popularity among golfers seeking improved launch angles and enhanced ball speed. Fairway wood and hybrid shafts are also witnessing growing demand as modern golf club designs incorporate versatile hybrid clubs that replace traditional long irons. The rising popularity of hybrid clubs among amateur golfers is further strengthening demand for specialized hybrid shafts designed to balance power, flexibility, and stability.

Flex Category Insights

Regular flex shafts dominate the global golf shaft market with an estimated 36% share of total revenue, primarily because they cater to the largest segment of recreational golfers with moderate swing speeds. Regular flex shafts provide an optimal balance between flexibility and stability, allowing golfers to achieve consistent ball flight and improved distance without sacrificing shot control. As the global base of amateur golfers continues to grow, particularly in emerging markets, the demand for regular flex shafts remains strong.

Stiff flex shafts are widely used by professional golfers and highly skilled players who generate higher swing speeds and require greater shaft stability to control ball trajectory and spin rates. These shafts reduce excessive bending during high-speed swings, enabling more precise shot shaping and accuracy. Meanwhile, senior flex and ladies flex shafts are gaining traction as golf participation expands among older demographics and female players. Manufacturers are increasingly designing lightweight, flexible shafts tailored specifically for these segments, which is contributing to the diversification and growth of the flex category within the market.

Price Tier Insights

Mid-range shafts priced between USD 50 and USD 150 account for the largest share of the golf shaft market, representing nearly 44% of total global sales. This segment is particularly popular among recreational golfers and intermediate players who seek a balance between affordability and improved performance. Mid-range shafts typically incorporate graphite or composite materials with moderate technological enhancements, offering reliable durability and performance improvements over entry-level options.

Premium shafts priced above USD 150 are rapidly gaining popularity among professional players and serious golf enthusiasts who prioritize performance optimization. These shafts often incorporate advanced carbon fiber structures, variable flex profiles, and proprietary engineering technologies designed to maximize swing speed and energy transfer. Although this segment represents a smaller share of total volume, it generates a significant portion of industry revenue due to its higher price points. Entry-level shafts remain widely used in mass-produced golf clubs targeted at beginner and recreational players, especially in starter golf club sets sold through sporting goods retailers.

Distribution Channel Insights

OEM supply to golf club manufacturers remains the dominant distribution channel in the golf shaft market, accounting for approximately 52% of total sales. In this model, shafts are integrated directly into newly manufactured golf clubs by equipment brands such as Callaway, TaylorMade, and Titleist. This channel benefits from large production volumes and long-term supplier relationships between shaft manufacturers and golf club brands.

Sports specialty stores and golf pro shops represent another important distribution channel, particularly for aftermarket shaft upgrades and custom club fitting services. These outlets provide personalized consultation and professional fitting services that allow golfers to select shafts optimized for their swing characteristics. Meanwhile, online retail platforms are experiencing rapid growth as golfers increasingly purchase equipment through e-commerce websites offering product comparisons, customer reviews, and competitive pricing. Direct-to-consumer online channels are also enabling shaft manufacturers to expand their global reach and build stronger brand engagement with amateur golfers.

Explore more data points, trends and opportunities Download Free Sample Report

Golf Shaft Market Segmentations

By Material Type

- Graphite Shafts

- Steel Shafts

- Hybrid Composite Shafts

By Club Type

- Iron Shafts

- Driver Shafts

- Fairway Wood Shafts

- Hybrid Shafts

By Flex Category

- Extra Stiff Flex

- Stiff Flex

- Regular Flex

- Senior Flex

- Ladies Flex

By Price Tier

- Entry-Level Shafts (Below USD 50)

- Mid-Range Shafts (USD 50–150)

- Premium Shafts (Above USD 150)

By Distribution Channel

- OEM Supply to Golf Club Manufacturers

- Sports Specialty Stores & Golf Pro Shops

- Online Retail

- Multi-Brand Sporting Goods Retailers

Regional Insights

North America

North America remains the largest regional market for golf shafts, accounting for approximately 42% of global demand in 2025. The United States dominates the regional market due to its large base of active golfers, well-established golf infrastructure, and strong presence of major golf equipment manufacturers. According to industry estimates, the United States alone hosts more than 15,000 golf courses, creating a strong ecosystem for golf participation and equipment consumption. High disposable income levels and a strong culture of recreational and professional golf encourage frequent equipment upgrades, particularly among avid golfers.

Another key driver for regional growth is the strong presence of custom club fitting services and premium golf retail chains. North American golfers are highly receptive to technologically advanced equipment, which has accelerated the adoption of high-performance graphite shafts and custom-designed shaft products. Additionally, professional tournaments, golf academies, and youth development programs continue to expand the golfer base, supporting long-term demand for golf equipment, including shafts.

Europe

Europe accounts for nearly 30% of the global golf shaft market, with major demand coming from the United Kingdom, Germany, France, Sweden, and Spain. The region benefits from a deeply rooted golf culture, with several historic golf clubs and international tournaments attracting enthusiasts from across the world. Golf tourism is a major driver of equipment demand in Europe, particularly in destinations such as Scotland, Ireland, and Portugal, where championship golf courses attract international visitors.

European golfers tend to favor technologically advanced golf equipment, particularly premium graphite shafts designed to improve launch conditions and swing efficiency. Increasing investments in golf resorts, training academies, and indoor golf simulation facilities are further expanding the golfer base. Additionally, growing interest in professional golf events such as the Ryder Cup and European Tour competitions continues to stimulate demand for high-performance golf equipment across the region.

Asia-Pacific

Asia-Pacific holds approximately 24% of the global golf shaft market and represents the fastest-growing region. Japan and South Korea are among the largest markets due to their long-standing golf culture and strong consumer spending on premium golf equipment. Japanese golfers, in particular, demonstrate high demand for technologically sophisticated shafts and custom golf club fitting services.

China is emerging as a major growth market as golf participation increases among affluent urban populations. The rapid development of golf resorts, training academies, and luxury residential communities featuring golf courses is driving demand for golf equipment. Additionally, rising disposable income levels and growing interest in international golf tournaments are encouraging more consumers to participate in the sport. Southeast Asian countries such as Thailand, Vietnam, and Malaysia are also witnessing growth in golf tourism, which further contributes to regional market expansion.

Latin America

Latin America accounts for approximately 5–6% of the global golf shaft market, with Brazil, Mexico, and Argentina representing the largest markets in the region. Golf participation in Latin America is closely linked to tourism and the development of luxury resort communities. Countries such as Mexico and the Dominican Republic have become popular golf tourism destinations due to their coastal championship courses and resort infrastructure.

The expansion of high-end residential developments featuring private golf clubs is another important growth driver in the region. As affluent consumers invest in luxury real estate projects with integrated golf courses, demand for golf equipment, including shafts, continues to increase. Additionally, international tournaments and golf academies are helping promote the sport among younger demographics in the region.

Middle East & Africa

The Middle East and Africa currently account for approximately 2–3% of global golf shaft demand, but the region is expected to experience strong long-term growth. Countries such as the United Arab Emirates, Saudi Arabia, and Qatar are investing heavily in golf infrastructure as part of broader tourism and sports development strategies.

The UAE has emerged as a key hub for international golf tournaments, including events on the European Tour and DP World Tour. Government initiatives aimed at promoting sports tourism and luxury travel are encouraging the development of world-class golf courses and training facilities. Saudi Arabia is also investing significantly in sports infrastructure through national development programs designed to diversify the economy and attract international tourism. In Africa, South Africa remains the largest golf market, supported by its strong golf heritage and growing golf tourism industry.

Key Players in the Golf Shaft Market

- True Temper Sports

- Fujikura

- Mitsubishi Chemical

- UST Mamiya

- Graphite Design

- Nippon Shaft

- KBS Golf Shafts

- Project X

- Aerotech Golf Shafts

- Paderson Shafts

- LA Golf

- Accra Golf Shafts

- Grafalloy

- FEMCO Steel Technology

- Newton Golf Company