Golf Rangefinders Market Size

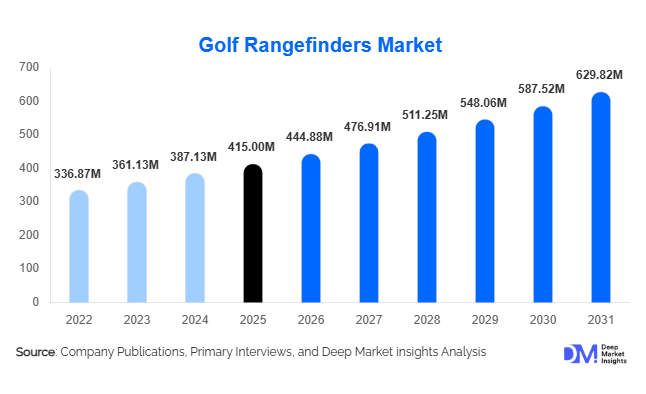

According to Deep Market Insights, the global golf rangefinders market size was valued at USD 415 million in 2025 and is projected to grow from USD 444.88 million in 2026 to reach USD 629.82 million by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). Market growth is primarily driven by increasing global golf participation, rising demand for precision-based performance tools, and rapid technological advancements in laser optics, GPS systems, and AI-enabled analytics.

Golf rangefinders have evolved from niche professional devices into mainstream sporting electronics used by both amateur and competitive golfers. Enhanced features such as slope-adjusted measurement, vibration target-lock systems, OLED displays, Bluetooth connectivity, and smartphone app integration have significantly expanded the product’s appeal. Premiumization trends are also reshaping the industry, with growing demand for devices priced above USD 300 in developed markets. Strong retail penetration, particularly through specialty golf stores and e-commerce platforms, continues to support global distribution. North America remains the dominant market, while Asia-Pacific is emerging as the fastest-growing region due to infrastructure development and rising middle-class participation in golf.

Key Market Insights

- Laser rangefinders dominate product demand, accounting for over 60% of global revenue due to superior accuracy and tournament acceptance.

- Slope-enabled and AI-integrated devices are rapidly gaining traction, reflecting golfer preference for advanced performance analytics.

- North America leads the global market, driven by high per-capita golf equipment spending and a large installed base of golf courses.

- Asia-Pacific is the fastest-growing region, supported by rising participation in Japan, South Korea, and China.

- Mid-range priced devices (USD 150–300) hold the largest share, balancing affordability with premium features.

- Offline specialty golf retail remains dominant, though online sales are expanding rapidly due to direct-to-consumer strategies.

What are the latest trends in the golf rangefinders market?

AI-Enabled Smart Rangefinders and App Integration

Manufacturers are increasingly integrating AI-based features such as wind speed calculation, club recommendation algorithms, and real-time shot tracking. Smart rangefinders now sync with mobile applications to provide post-round analytics, digital scorecards, and performance history tracking. This integration is transforming rangefinders from standalone distance-measurement devices into comprehensive performance ecosystems. Subscription-based analytics platforms are emerging, offering recurring revenue streams for manufacturers while enhancing long-term customer engagement.

Premiumization and Tournament-Compliant Slope Technology

Premium rangefinders with OLED displays, waterproof casing, magnetic cart mounts, and extended battery life are gaining market share. Devices with switchable slope functionality are increasingly accepted in amateur competitions following regulatory clarifications from bodies such as the United States Golf Association (USGA) and The R&A. This shift is accelerating upgrades among amateur and semi-professional players seeking a competitive advantage without violating tournament rules.

What are the key drivers in the golf rangefinders market?

Rising Global Golf Participation

Golf participation has rebounded strongly across North America and Asia-Pacific, supported by lifestyle trends and increased recreational sports spending. Amateur golfers represent nearly 67% of total device demand, creating sustained revenue generation. Growing youth academies and golf training centers further support recurring equipment purchases.

Technological Advancements in Optics and GPS

Advancements in laser accuracy (±1 yard precision), faster target-lock systems, and integrated GPS course mapping are improving user experience. Continuous R&D investments in optics and microelectronics are lowering component costs while enhancing product performance.

What are the restraints for the global market?

Price Sensitivity in Emerging Markets

Premium devices priced above USD 300 remain inaccessible to many golfers in developing economies. High import duties and limited disposable income constrain penetration rates.

Competition from Mobile Golf GPS Applications

Smartphone-based GPS apps offer lower-cost alternatives for casual golfers. Although they lack laser-level precision, their affordability may limit entry-level device adoption.

What are the key opportunities in the golf rangefinders industry?

Expansion into Emerging Golf Economies

Asia-Pacific and Middle Eastern countries are investing in golf tourism infrastructure, presenting significant growth opportunities. Early localization strategies and partnerships with golf academies can accelerate brand penetration.

Hardware-Plus-Software Revenue Models

Manufacturers can expand beyond hardware sales by introducing subscription-based analytics, premium course databases, and integrated wearable connectivity, increasing lifetime customer value and profit margins.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 415 Million |

| Market Size in 2026 | USD 444.88 Million |

| Market Size in 2031 | USD 629.82 Million |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Laser rangefinders continue to dominate the global golf rangefinders market, accounting for approximately 62% of total revenue in 2025. Their leadership position is primarily driven by superior accuracy (often within ±1 yard), faster target acquisition, vibration-based flag lock features, and widespread acceptance in amateur tournaments. Competitive golfers and serious amateurs prefer laser devices because they provide precise, real-time yardage unaffected by course database limitations. In addition, technological improvements in optics, compact form factors, OLED displays, and magnetic cart mounts have enhanced usability and durability, reinforcing their dominance.

GPS rangefinders serve convenience-oriented players who value preloaded course maps, hazard identification, and ease of use without requiring precise target alignment. These devices are popular among casual and senior golfers seeking simplified interfaces. Meanwhile, hybrid rangefinders, which integrate both laser and GPS capabilities, are gaining traction in the premium segment. Although their share remains smaller compared to standalone laser devices, hybrids command higher average selling prices and margins due to their comprehensive performance analytics and app connectivity, making them attractive to performance-focused users.

Technology Insights

Slope-enabled rangefinders account for nearly 55% of global sales in 2025, driven by increasing demand for performance optimization. These devices calculate elevation-adjusted distances, providing golfers with more accurate club selection guidance. Regulatory flexibility from governing bodies such as the United States Golf Association (USGA) and The R&A, particularly for amateur play, has significantly accelerated adoption. The ability to switch slope mode on and off for tournament compliance has further strengthened demand.

Standard distance measurement devices remain relevant for entry-level buyers and strict competitive formats where slope functionality may be restricted. However, the fastest-growing category is AI-enabled and smart-connected rangefinders, expanding at approximately 9% annually. These devices integrate wind speed analysis, club recommendations, shot tracking, and mobile app synchronization. The shift toward data-driven performance improvement and post-round analytics is positioning AI-enabled rangefinders as the next innovation frontier in golf electronics.

Distribution Channel Insights

Offline channels contribute approximately 58% of total market revenue in 2025, led by specialty golf retailers, sporting goods chains, and pro shops. The dominance of offline retail is driven by the importance of product demonstration, hands-on testing, and professional recommendations before purchase. Golfers often prefer to physically evaluate display clarity, weight, grip comfort, and target-lock speed before investing in mid- to high-priced devices.

However, online retail is expanding rapidly, supported by direct-to-consumer (D2C) brand strategies, competitive pricing, bundled promotional offers, and access to customer reviews. E-commerce growth is particularly strong in North America and Asia-Pacific, where digital purchasing behavior is well established. Subscription bundles and online-exclusive product launches are further accelerating digital channel penetration.

End-User Insights

Amateur and recreational golfers dominate demand, accounting for approximately 67% of total revenue in 2025. Growth in this segment is fueled by rising participation rates, lifestyle-driven sports spending, and increasing awareness of performance-enhancing technology. Many amateur golfers are upgrading from basic GPS apps to dedicated laser or hybrid devices for improved accuracy and competitive advantage.

Professional golfers and tournament players represent a high-value niche segment, often driving premium product adoption and brand visibility. Their influence significantly impacts consumer purchasing decisions. Meanwhile, golf academies and training facilities are emerging as a fast-growing institutional segment, as structured coaching programs standardize performance measurement tools and invest in advanced training technologies.

Explore more data points, trends and opportunities Download Free Sample Report

Golf Rangefinders Market Segmentations

By Product Type

- Laser Rangefinders

- GPS Rangefinders

- Hybrid (Laser + GPS) Rangefinders

By Technology

- Standard Distance Measurement

- Slope-Enabled Rangefinders

- AI-Enabled / Smart Connected Rangefinders

By Price Range

- Entry-Level (Below USD 150)

- Mid-Range (USD 150–300)

- Premium (Above USD 300)

By Distribution Channel

- Online Retail

- Specialty Golf Stores

- Sporting Goods Retail Chains

- Pro Shops / Golf Clubs

By End User

- Professional Golfers & Tournament Players

- Amateur & Recreational Golfers

- Golf Academies & Training Facilities

Regional Insights

North America

North America accounts for approximately 42% of global revenue in 2025, maintaining its position as the largest regional market. The United States alone contributes nearly 38% of total global demand, supported by a large installed base of golf courses, high per-capita spending on sporting electronics, and strong brand loyalty toward established manufacturers. The presence of leading companies and strong retail networks further enhances market penetration. Additionally, rising amateur tournament participation and steady replacement demand for upgraded devices are key regional growth drivers. Canada contributes a stable demand due to well-established golf participation rates and growing interest in premium golf equipment.

Europe

Europe holds nearly 24% market share, led by the United Kingdom, Germany, and France. Growth in the region is supported by a mature golf culture, increasing adoption of premium sporting electronics, and strong participation in club-level competitions. Technological adoption and demand for slope-enabled devices are increasing, particularly among younger golfers. Furthermore, cross-border e-commerce growth within the European Union has improved product accessibility and price competitiveness.

Asia-Pacific

Asia-Pacific represents approximately 22% of global revenue and is the fastest-growing region with an estimated CAGR of 9%. Japan and South Korea currently lead regional demand due to high golf participation rates and strong consumer spending on advanced sporting equipment. China is emerging as a high-growth market, supported by golf infrastructure expansion, rising middle-class wealth, and government-backed sports development initiatives. Increasing golf tourism and corporate golf events across Southeast Asia are further contributing to demand growth.

Latin America

Latin America accounts for around 6% of the global market, with Brazil and Mexico serving as primary contributors. Regional growth is driven by expanding golf tourism, rising urban affluence, and growing interest in premium lifestyle sports. However, price sensitivity remains a limiting factor, resulting in stronger demand for mid-range devices compared to premium models.

Middle East & Africa

The Middle East & Africa region contributes approximately 6% of global revenue. The UAE and South Africa are key markets, supported by luxury golf resorts, international tournaments, and strong tourism inflows. Government investments in sports infrastructure, including championship golf courses, are creating sustained equipment demand. High-income consumer segments in the Gulf region are particularly inclined toward premium and hybrid rangefinder models, driving higher average selling prices within the region.

Key Players in the Golf Rangefinders Market

- Bushnell

- Garmin

- Nikon

- Callaway Golf

- Leupold & Stevens

- TecTecTec

- Precision Pro Golf

- Voice Caddie

- SkyCaddie

- Blue Tees Golf

- Shot Scope

- Cobra Golf

- Canon

- Simmons

- GolfBuddy