Gas Barbecue Grills Market Size

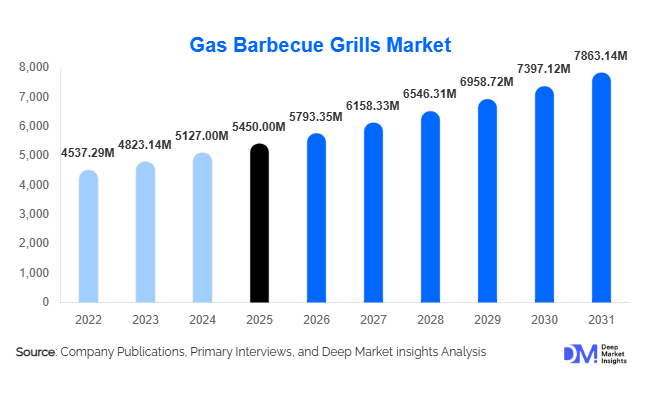

According to Deep Market Insights, the global gas barbecue grills market size was valued at USD 5,450 million in 2025 and is projected to grow from USD 5,793.35 million in 2026 to reach USD 7,863.14 million by 2031, expanding at a CAGR of 6.3% during the forecast period (2026–2031). The market growth is primarily driven by rising outdoor cooking culture, increasing residential patio and backyard renovations, and growing commercial demand from restaurants, hotels, and catering businesses. Gas grills continue to gain preference over charcoal alternatives due to faster ignition, precise temperature control, lower smoke emissions, and easier maintenance.

Key Market Insights

- Freestanding gas grills dominate global sales, accounting for nearly 58% of total revenue in 2025 due to their versatility and residential adoption.

- Propane (LPG)-based grills lead with approximately 68% share, supported by widespread cylinder distribution and portability advantages.

- Mid-range grills (USD 300–800) hold nearly 49% of the market, reflecting strong demand for feature-rich yet affordable products.

- North America remains the largest regional market, contributing around 38% of global revenue in 2025.

- Asia-Pacific is the fastest-growing region, expanding at nearly 8% CAGR, driven by urbanization and rising middle-class spending.

- Smart grill technologies, including Bluetooth thermometers and app-based monitoring systems, are increasingly influencing premium segment growth.

What are the latest trends in the gas barbecue grills market?

Smart and Connected Grilling Solutions

Manufacturers are increasingly integrating IoT-enabled temperature probes, Wi-Fi connectivity, and mobile app controls into premium gas grills. These smart features allow real-time heat monitoring, remote control of burners, and automated cooking presets, appealing particularly to tech-savvy consumers. Connected grilling ecosystems are creating opportunities for higher-margin products and customer loyalty through proprietary applications and digital engagement platforms.

Premium Outdoor Kitchen Integration

There is a rising shift toward built-in gas grills integrated within outdoor kitchens. Homeowners in North America and Europe are investing in stainless steel, multi-burner configurations with side burners and infrared searing zones. This trend is driving growth in the premium segment and supporting higher average selling prices globally.

What are the key drivers in the gas barbecue grills market?

Growth in Residential Outdoor Living Spaces

Increasing investments in backyard renovations and outdoor entertainment spaces are fueling demand. Homeowners are allocating higher budgets to patio enhancements, directly benefiting gas grill manufacturers. The residential segment accounts for nearly 72% of the overall market value in 2025.

Convenience and Time Efficiency

Gas grills provide rapid ignition, uniform heating, and precise temperature control compared to charcoal grills. These advantages resonate with younger consumers and working households, supporting replacement demand in mature markets.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuating prices of stainless steel and aluminum significantly impact manufacturing costs. Producers face margin pressure when raw material inflation cannot be fully transferred to end consumers, particularly in the economy segment.

Seasonality of Demand

Sales are highly concentrated in the spring and summer months in temperate regions. Weather variability can influence annual revenue performance, especially in North America and Europe.

What are the key opportunities in the gas barbecue grills industry?

Expansion in Emerging Markets

Rising disposable income in Asia-Pacific and Latin America is creating strong first-time buyer demand. Compact and portable gas grills are particularly attractive for urban households with limited outdoor space.

Sustainability and Energy Efficiency Innovations

Governments promoting cleaner LPG infrastructure and low-emission appliances provide opportunities for gas grill manufacturers to develop energy-efficient burners and eco-friendly designs. ESG-focused branding can further differentiate premium players.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5450 Million |

| Market Size in 2026 | USD 5793.35 Million |

| Market Size in 2031 | USD 7863.14 Million |

| CAGR | 6.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Freestanding gas grills dominate the global market with approximately 58% share in 2025, primarily driven by strong residential demand and ease of installation. These models require no permanent structural modification, making them highly suitable for suburban homes, rental properties, and seasonal usage. Their mobility, wide price availability (economy to premium), and compatibility with propane fuel systems make them the preferred choice across North America and Europe. Replacement demand also remains high in this category, as average product life cycles range between 5 and 8 years, supporting recurring sales.

Built-in gas grills represent a fast-growing premium segment, particularly in developed markets where outdoor kitchen installations are expanding. Growth in this category is fueled by rising investments in backyard remodeling, luxury villa construction, and integrated outdoor living spaces. Portable and tabletop grills are witnessing accelerating adoption in dense urban markets across Asia-Pacific and Latin America, where limited balcony and patio space necessitate compact, lightweight designs. Innovation in foldable frames, lightweight stainless-steel construction, and travel-friendly propane canisters is further supporting this sub-segment.

Burner Configuration Insights

Three to four-burner gas grills lead the market with around 46% share in 2025, as they provide an optimal balance between cooking capacity, price, and fuel efficiency. This configuration meets the needs of average households (4–6 members) and small gatherings, making it the most commercially viable and globally scalable product category. Manufacturers strategically position this segment within the mid-range pricing tier (USD 300–800), which itself accounts for nearly 49% of global revenue. One to two-burner grills primarily serve entry-level consumers, apartment dwellers, and portable usage scenarios. Meanwhile, five-burner and above configurations are gaining momentum in premium residential installations and commercial foodservice establishments, particularly restaurants and hotels offering live-grill dining experiences.

Fuel Type Insights

Propane (LPG) grills dominate with nearly 68% of global market share, driven by portability, ease of cylinder exchange, and widespread retail distribution networks. Propane’s flexibility makes it ideal for freestanding grills, tailgating, and camping applications. The rapid ignition capability and independence from fixed gas lines enhance consumer convenience, particularly in North America.

Natural gas grills are predominantly installed in permanent residential settings with dedicated pipeline infrastructure. Adoption is strongest in urban regions of the U.S., Canada, and Western Europe, where stable gas connectivity and lower long-term fuel costs justify fixed installations. Growth in this segment is closely tied to housing construction trends and urban gas infrastructure expansion.

Distribution Channel Insights

Offline retail accounts for approximately 61% of global sales, as consumers prefer physical inspection of build quality, burner strength, and material finish before purchase. Specialty home improvement stores and large-format retailers remain dominant sales channels, especially in North America and Europe. In-store demonstrations and bundled accessory sales further enhance average transaction values. Online retail is the fastest-growing channel, supported by expanding e-commerce penetration, competitive pricing, seasonal promotional campaigns, and direct-to-consumer strategies adopted by leading brands. Growth in online sales is particularly strong in the Asia-Pacific region, where digital marketplaces significantly influence appliance purchases.

End-Use Insights

The residential segment accounts for approximately USD 3.9 billion in 2025, representing nearly 72% of total market revenue. Growth is driven by backyard cooking culture, rising home improvement expenditure, and increasing consumer preference for outdoor social gatherings. Developed markets exhibit strong replacement demand, while emerging markets show first-time purchase growth. The commercial segment, valued at around USD 1.5 billion in 2025, is expanding at a faster CAGR of 7–8%. Growth drivers include global expansion of quick-service restaurants, experiential dining formats, hotel and resort development, and catering services. High-capacity built-in grills are increasingly deployed in hospitality environments, particularly in tourism-driven economies.

Explore more data points, trends and opportunities Download Free Sample Report

Gas Barbecue Grills Market Segmentations

By Product Type

- Freestanding Gas Grills

- Built-in Gas Grills

- Portable/Tabletop Gas Grills

By Burner Configuration

- 1–2 Burners

- 3–4 Burners

- 5 Burners & Above

By Price Range

- Economy (Below USD 300)

- Mid-Range (USD 300–800)

- Premium (Above USD 800)

By End-Use

- Residential

- Commercial

By Distribution Channel

- Offline Retail

- Online Retail

Regional Insights

North America

North America holds approximately 38% of the global market in 2025, making it the largest regional contributor. The United States accounts for nearly 85% of regional demand, supported by deeply embedded barbecue culture, suburban housing patterns with backyard spaces, and high replacement cycles. Strong consumer purchasing power, seasonal promotional sales, and mature propane distribution networks further sustain demand. Canada contributes stable seasonal sales, driven by outdoor leisure culture and increasing deck renovations.

Europe

Europe represents around 27% of global revenue, led by Germany, the UK, and France. Germany accounts for nearly 22% of European demand due to strong garden culture and high consumer spending on outdoor appliances. Stringent emission regulations and environmental awareness are encouraging consumers to shift from charcoal to cleaner gas alternatives. Additionally, rising urban terrace living and increased adoption of compact grills in Southern Europe are supporting steady growth.

Asia-Pacific

Asia-Pacific holds approximately 22% market share and is the fastest-growing region at close to 8% CAGR. China and Australia are leading contributors. In China, rising disposable incomes, expanding middle-class households, and Western lifestyle influences are driving premium grill adoption. Australia benefits from one of the world’s strongest outdoor cooking cultures. Urbanization, e-commerce penetration, and expanding residential construction across Southeast Asia are further accelerating regional growth.

Middle East & Africa

The Middle East & Africa account for roughly 7% of global demand. Growth is primarily driven by hospitality sector expansion in the UAE and Saudi Arabia, where luxury villa developments, resort construction, and tourism diversification initiatives are increasing demand for premium built-in gas grills. Rising disposable income and outdoor entertainment culture are also contributing to residential adoption in urban areas.

Latin America

Latin America contributes around 6% of global revenue, with Brazil and Mexico leading consumption. Growth drivers include rising middle-class income, urban housing development, and the increasing popularity of social outdoor gatherings. Expansion of modern retail infrastructure and improving e-commerce accessibility are further supporting market penetration across the region.

Key Players in the Gas Barbecue Grills Market

- Weber Inc.

- Napoleon Products

- Char-Broil

- Broil King

- Traeger Inc.

- Landmann

- Char-Griller

- Bull Outdoor Products

- Dyna-Glo

- Rinnai Corporation

- Middleby Corporation

- Saber Grills

- Coleman Company

- Fire Magic

- Kenmore