Gaming Monitor Market Size

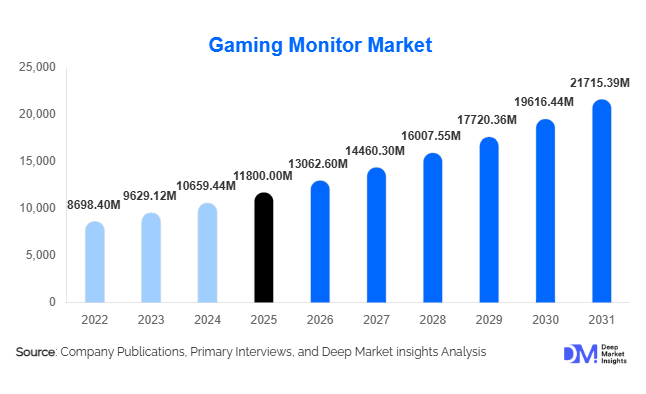

According to Deep Market Insights, the global gaming monitor market size was valued at USD 11,800 million in 2025 and is projected to grow from USD 13,062.60 million in 2026 to reach USD 21,715.39 million by 2031, expanding at a CAGR of 10.7% during the forecast period (2026–2031). The gaming monitor market growth is primarily driven by the rapid expansion of the global gaming ecosystem, increasing adoption of high-performance displays among professional and casual gamers, and rising demand for immersive visual experiences supported by advanced panel technologies such as OLED and Mini-LED.

Key Market Insights

- High refresh rate monitors (144 Hz and above) are becoming standard, driven by competitive gaming and esports demand.

- IPS panels dominate the market, offering superior color accuracy and wide viewing angles for both gaming and content creation.

- Asia-Pacific leads global demand, supported by strong manufacturing capabilities and a large gaming population.

- The mid-range pricing segment (USD 300–700) holds the largest share, reflecting consumer preference for value-performance balance.

- Online retail channels dominate distribution, fueled by e-commerce growth and digital purchasing behavior.

- OLED and Mini-LED technologies are emerging as key innovation drivers, enhancing contrast ratios and response times.

What are the latest trends in the gaming monitor market?

Shift Toward OLED and Mini-LED Displays

The gaming monitor market is witnessing a significant transition toward OLED and Mini-LED technologies. These advanced display technologies offer superior contrast ratios, deeper blacks, and faster response times compared to traditional LCD panels. As production costs gradually decline, these technologies are moving beyond premium segments into mid-range categories, expanding their accessibility. Manufacturers are investing heavily in improving brightness levels, reducing burn-in risks, and enhancing durability, making OLED monitors more viable for long gaming sessions. This trend is particularly appealing to professional gamers and content creators who prioritize visual quality and performance.

Rise of Ultra-High Refresh Rates and Esports Optimization

Ultra-high refresh rate monitors, exceeding 240 Hz and even reaching 360 Hz, are becoming increasingly popular, especially in esports and competitive gaming environments. These monitors provide smoother gameplay and reduced motion blur, offering a competitive edge. Gaming monitor manufacturers are collaborating with esports organizations to design products specifically optimized for professional gaming. Features such as low latency, adaptive sync technologies, and customizable settings are being integrated to enhance performance. This trend is expected to continue as esports gains mainstream recognition and investment globally.

What are the key drivers in the gaming monitor market?

Expansion of the Global Gaming Industry

The rapid growth of the global gaming industry, which has surpassed USD 200 billion in revenue, is a primary driver for gaming monitors. Increasing participation in online multiplayer games and the rise of streaming platforms have created a strong demand for high-performance displays. Gamers are increasingly upgrading their setups to enhance their gaming experience, driving consistent market growth.

Technological Advancements in Display Hardware

Continuous innovation in display technologies, including HDR, adaptive sync, and ultra-fast refresh rates, has significantly improved gaming experiences. These advancements have transformed gaming monitors into essential components for serious gamers. The integration of AI-based enhancements and improved color accuracy further boosts adoption across both gaming and professional applications.

What are the restraints for the global market?

High Cost of Advanced Gaming Monitors

Premium gaming monitors, particularly those featuring OLED panels, 4K resolution, and high refresh rates, remain expensive. This limits their adoption in price-sensitive markets, especially in developing regions. Despite declining costs, affordability remains a key challenge for broader market penetration.

Supply Chain and Component Constraints

The gaming monitor market is highly dependent on semiconductor and display panel supply chains. Fluctuations in raw material prices and geopolitical disruptions can impact production and pricing. These challenges can delay product launches and affect overall market growth.

What are the key opportunities in the gaming monitor industry?

Growth of Esports Infrastructure

The expansion of esports infrastructure presents a major opportunity for gaming monitor manufacturers. Investments in esports arenas, tournaments, and training facilities are increasing globally, particularly in the Asia-Pacific and North America. These developments require high-performance monitors with ultra-fast refresh rates and low latency, creating a strong demand for specialized products.

Emerging Markets and Rising Disposable Income

Emerging economies such as India, Brazil, and Southeast Asian countries are witnessing rapid growth in gaming adoption. Increasing disposable income, improved internet connectivity, and a shift toward PC gaming are driving demand for gaming monitors. Manufacturers can tap into these markets through localized pricing strategies and expanded distribution networks.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11800 Million |

| Market Size in 2026 | USD 13062.60 Million |

| Market Size in 2031 | USD 21715.39 Million |

| CAGR | 10.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Mid-sized gaming monitors (24–27 inches) dominate the market, accounting for approximately 38% of the 2025 market share. This segment’s leadership is primarily driven by its optimal balance between performance, affordability, and desk-space efficiency, making it the preferred choice for both competitive esports players and mainstream consumers. These monitors are widely compatible with mid-range GPUs, enabling high refresh rate performance (144–240 Hz) without requiring expensive hardware upgrades. Additionally, this size range aligns well with ergonomic viewing distances, which is critical for long gaming sessions. Larger monitors above 32 inches are gaining traction, particularly in immersive and simulation-based gaming, supported by the rise of curved and ultra-wide formats. However, their higher price points and space requirements limit widespread adoption. Smaller monitors below 24 inches are gradually declining in demand due to limited immersion and lower feature integration, especially as gamers increasingly prioritize visual experience and multitasking capabilities.

Application Insights

Individual consumers represent the largest application segment, contributing nearly 70% of the total market share in 2025. The dominance of this segment is driven by the rapid expansion of home gaming ecosystems, increasing penetration of gaming PCs and consoles, and the rise of streaming platforms such as Twitch and YouTube Gaming. Gamers are increasingly investing in high-performance monitors to enhance gameplay quality, reduce latency, and improve visual clarity. Additionally, the growing trend of hybrid usage, where monitors are used for both gaming and productivity, further strengthens demand among individual users. Meanwhile, commercial applications, including gaming cafés, esports arenas, and professional training facilities, represent the fastest-growing segment. This growth is fueled by rising investments in esports infrastructure, particularly in Asia-Pacific and North America, where organized gaming tournaments and leagues are expanding rapidly. Bulk procurement of high-refresh-rate monitors in these facilities is significantly contributing to overall market growth.

Distribution Channel Insights

Online retail channels dominate the gaming monitor market, accounting for approximately 55% of total sales in 2025. The growth of this segment is driven by the increasing penetration of e-commerce platforms, the availability of a wide product range, and competitive pricing enabled by direct-to-consumer (D2C) models. Online platforms allow consumers to compare specifications, read reviews, and access discounts, making them the preferred purchasing channel, especially among younger demographics. Flash sales, bundled offers, and easy financing options further accelerate online sales. Offline channels, including specialty electronics stores and brand outlets, continue to play a crucial role in premium and high-end product segments. Consumers purchasing OLED or ultra-wide monitors often prefer in-store experiences to evaluate display quality, build design, and ergonomics before making high-value purchases. Additionally, offline channels are important in emerging markets where digital trust and logistics infrastructure are still developing.

Traveler Type Insights

Competitive gamers form the largest user group within the gaming monitor market, driven by their demand for ultra-fast refresh rates, low response times, and advanced synchronization technologies such as NVIDIA G-Sync and AMD FreeSync. This segment prioritizes performance over price, leading to higher adoption of premium monitors. Casual gamers represent a significant portion of the market, focusing on affordability and balanced performance, often opting for mid-range monitors with Full HD or QHD resolution. Content creators and streamers are emerging as a rapidly growing segment, requiring high-resolution displays with accurate color reproduction and HDR capabilities. This group is influencing product innovation, as manufacturers increasingly design monitors that cater to both gaming and professional content creation needs, thereby expanding the overall addressable market.

Age Group Insights

Consumers aged 18–35 years dominate the gaming monitor market, driven by high engagement in gaming, esports, and digital content consumption. This demographic is highly tech-savvy and prioritizes performance features such as refresh rate, resolution, and response time when making purchasing decisions. The influence of social media, streaming platforms, and competitive gaming culture further strengthens demand within this age group. The 35–50 age group is also contributing significantly, particularly in the premium segment, as higher disposable income allows for investment in advanced gaming setups, including OLED and ultra-wide monitors. This segment often uses gaming monitors for both entertainment and professional purposes, such as content creation and remote work. Older demographics are gradually entering the market as gaming becomes more mainstream, though their contribution remains comparatively smaller.

Explore more data points, trends and opportunities Download Free Sample Report

Gaming Monitor Market Segmentations

By Screen Size

- Below 24 Inches

- 24–27 Inches

- 28–32 Inches

- Above 32 Inches

By Refresh Rate

- Below 144 Hz

- 144–240 Hz

- 241–360 Hz

- Above 360 Hz

By Price Range

- Budget (Below USD 300)

- Mid-Range (USD 300–700)

- Premium (Above USD 700)

By Distribution Channel

- Online Retail

- Offline Retail

By End User

- Individual Consumers

- Commercial

Regional Insights

North America

North America holds approximately 27% of the global market share, with the United States accounting for the majority of regional demand. The region’s growth is driven by high disposable income, a mature gaming ecosystem, and strong adoption of advanced technologies such as OLED and 4K displays. The presence of leading gaming companies and esports organizations further accelerates demand for high-performance monitors. Additionally, the growing popularity of streaming and content creation, along with widespread availability of high-speed internet, supports continuous market expansion. The U.S. remains the largest contributor, while Canada shows steady growth driven by increasing gaming participation.

Europe

Europe accounts for around 20% of the global market, with Germany, the United Kingdom, and France serving as key demand centers. The region’s growth is driven by a strong base of PC gamers, increasing adoption of high-resolution monitors, and a growing content creation industry. European consumers show a preference for high-quality and energy-efficient products, encouraging manufacturers to focus on sustainability and advanced display technologies. Additionally, the expansion of esports events and gaming communities across the region is boosting demand for high-refresh-rate monitors. Government regulations promoting energy efficiency and electronic waste management are also shaping product innovation.

Asia-Pacific

Asia-Pacific dominates the gaming monitor market with approximately 41% share in 2025, making it the largest and fastest-growing region. China leads the market due to its massive gaming population, strong domestic manufacturing capabilities, and government support for electronics production. India is the fastest-growing country in the region, with double-digit growth driven by rising disposable income, increasing internet penetration, and rapid adoption of PC and console gaming. South Korea and Japan contribute significantly due to their advanced gaming culture and early adoption of cutting-edge technologies. The region also benefits from the presence of major manufacturing hubs, enabling cost-effective production and export-driven growth.

Latin America

Latin America holds about 6% of the global market, led by Brazil and Mexico. The region is experiencing steady growth due to increasing gaming adoption, improving broadband infrastructure, and rising interest in esports. Government initiatives supporting digitalization and the expansion of online gaming platforms are further driving demand. However, price sensitivity remains a key challenge, leading to higher demand for budget and mid-range gaming monitors. Localization strategies and affordable product offerings are critical for market expansion in this region.

Middle East & Africa

The Middle East & Africa region contributes nearly 6% of the global market, with the UAE and South Africa emerging as key markets. Growth in this region is driven by increasing investments in gaming infrastructure, the rising popularity of esports, and government initiatives aimed at diversifying economies through digital entertainment sectors. The UAE, in particular, is investing heavily in gaming events and esports tournaments, creating demand for high-end gaming equipment. In Africa, improving internet connectivity and the growing youth population are supporting gradual market expansion. While the region is still developing, it presents significant long-term growth potential for gaming monitor manufacturers.

Key Players in the Gaming Monitor Market

- Samsung Electronics

- LG Electronics

- Dell Technologies

- ASUS

- Acer

- MSI

- BenQ

- Gigabyte

- HP

- Lenovo

- ViewSonic

- AOC (TPV Technology)

- Philips (TPV)

- Sony

- Panasonic