Frying Pan Market Size

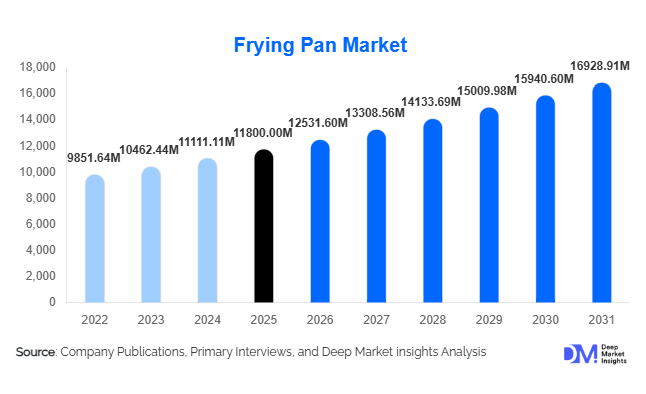

According to Deep Market Insights, the global frying pan market size was valued at USD 11,800 million in 2025 and is projected to grow from USD 12,531.60 million in 2026 to reach USD 16,928.91 million by 2031, expanding at a CAGR of 6.2% during the forecast period (2026–2031). The frying pan market growth is primarily driven by increasing home cooking trends, rising urbanization, and continuous product innovation in cookware materials and coatings. Growing consumer preference for durable, non-toxic, and easy-to-clean cookware has further strengthened market demand globally.

Key Market Insights

- Non-stick frying pans dominate the market, accounting for over 50% share due to convenience and ease of maintenance.

- Asia-Pacific leads global demand, driven by a large population base, manufacturing dominance, and rising middle-class consumption.

- Residential usage accounts for the majority of demand, supported by increased home cooking and kitchen upgrades.

- Mid-range products are the most widely sold segment, balancing affordability and durability across emerging markets.

- E-commerce is rapidly transforming distribution, enabling global brands to reach wider consumer bases.

- Sustainability and chemical-free coatings are becoming critical factors influencing consumer purchasing decisions.

What are the latest trends in the frying pan market?

Shift Toward Eco-Friendly and Non-Toxic Cookware

Consumers are increasingly prioritizing health and environmental safety, driving demand for frying pans made with PFOA-free, PTFE-free, and ceramic-based coatings. Manufacturers are responding by introducing eco-friendly product lines, incorporating recycled metals, and sustainable packaging. Regulatory pressure in developed regions is accelerating the transition toward safer materials, positioning sustainability as a core competitive differentiator in the frying pan market.

Growth of Induction-Compatible and Smart Cookware

The rising adoption of induction cooktops, particularly in urban households, is driving demand for induction-compatible frying pans. Additionally, smart cookware innovations such as heat indicators, temperature sensors, and multi-layered bases are enhancing cooking efficiency. These advancements appeal to tech-savvy consumers and support premiumization within the market, enabling brands to command higher price points.

What are the key drivers in the frying pan market?

Rising Home Cooking and Health Awareness

Global shifts toward home cooking, driven by health consciousness and cost savings, are significantly boosting frying pan demand. Consumers are investing in better-quality cookware to prepare healthier meals, increasing replacement cycles and supporting market growth.

Urbanization and Rising Disposable Income

Rapid urbanization, particularly in Asia-Pacific and Latin America, is expanding the consumer base for modern kitchenware. Increasing disposable incomes allow households to upgrade to premium and durable frying pans, contributing to sustained market expansion.

Product Innovation and Premiumization

Continuous innovation in materials, coatings, and design is driving consumer interest. Features such as scratch resistance, ergonomic handles, and aesthetic finishes are enhancing product appeal. Premium brands are capitalizing on these trends by offering high-performance cookware with extended durability.

What are the restraints for the global market?

Volatility in Raw Material Prices

Fluctuations in the prices of aluminum, stainless steel, and copper significantly impact production costs. This volatility affects profit margins and creates pricing challenges for manufacturers, particularly in competitive markets.

Regulatory Restrictions on Chemical Coatings

Strict regulations on non-stick coatings, especially in Europe and North America, pose challenges for manufacturers. Compliance requirements increase R&D costs and may limit the use of certain materials, potentially slowing market growth.

What are the key opportunities in the frying pan industry?

Expansion in Emerging Markets

Countries such as India, Indonesia, and Brazil present significant growth opportunities due to rising middle-class populations and increasing urbanization. Expansion of retail infrastructure and e-commerce platforms is further enabling market penetration in these regions.

Adoption of Sustainable and Premium Products

The growing demand for eco-friendly cookware provides an opportunity for manufacturers to introduce premium, sustainable product lines. Brands investing in non-toxic coatings and recyclable materials can capture higher-value segments and build long-term consumer trust.

Technological Integration in Cookware

Innovations such as induction compatibility, heat sensors, and multi-functional cookware are opening new avenues for differentiation. These technologies cater to evolving consumer preferences and support the premiumization trend across developed markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11800 Million |

| Market Size in 2026 | USD 12531.60 Million |

| Market Size in 2031 | USD 16928.91 Million |

| CAGR | 6.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Material Type Insights

Aluminum frying pans continue to dominate the global market, accounting for approximately 38% of the total market share in 2025. The leadership of this segment is primarily driven by its superior heat conductivity, lightweight structure, and cost-effectiveness, making it highly accessible to mass-market consumers across both developed and emerging economies. In regions such as Asia-Pacific and Latin America, where price sensitivity remains high, aluminum cookware serves as the preferred choice for households due to its affordability and ease of use. Additionally, advancements such as hard-anodized aluminum have significantly improved durability, corrosion resistance, and scratch resistance, further strengthening its market position.

Meanwhile, stainless steel and cast iron frying pans are gaining increasing traction in premium segments. Stainless steel, particularly multi-ply variants, is favored for its durability, non-reactive properties, and compatibility with induction cooking. Cast iron pans, on the other hand, are witnessing renewed demand due to their long lifespan and superior heat retention, especially among health-conscious consumers and professional chefs. This shift toward premium materials reflects a broader trend of product longevity and performance-driven purchasing behavior.

Coating Type Insights

Non-stick coatings remain the leading segment, capturing approximately 52% of the global market share. The dominance of this segment is largely attributed to its convenience, minimal oil requirement, and ease of cleaning, making it highly suitable for modern, fast-paced lifestyles. Urban households, particularly in North America and the Asia-Pacific, are increasingly adopting non-stick cookware to reduce cooking time and simplify maintenance. Continuous innovations in coating technologies, including multi-layered and reinforced non-stick surfaces, have also enhanced durability and safety, addressing earlier concerns about wear and tear.

At the same time, ceramic coatings are emerging as the fastest-growing segment due to rising awareness around chemical safety and environmental sustainability. Consumers in Europe and North America are actively shifting toward PFOA-free and PTFE-free alternatives, driving demand for ceramic-coated frying pans. This segment is further supported by regulatory frameworks that encourage the adoption of safer, eco-friendly materials, positioning ceramic coatings as a key growth area in the coming years.

Price Range Insights

The mid-range segment dominates the frying pan market, accounting for approximately 45% of the total market share. This segment’s leadership is driven by its ability to offer a balanced combination of affordability, durability, and performance, making it highly appealing to a broad consumer base. In emerging markets such as India, Indonesia, and Brazil, mid-range products are particularly popular among middle-income households upgrading from basic cookware to more durable and feature-rich options.

Premium frying pans, although smaller in share, are experiencing the fastest growth. This trend is fueled by increasing consumer willingness to invest in high-quality, long-lasting cookware with advanced features such as induction compatibility, ergonomic design, and enhanced aesthetics. In developed markets, premiumization is further supported by brand loyalty and the growing influence of lifestyle-driven purchasing decisions.

Distribution Channel Insights

Offline retail channels continue to dominate the frying pan market, holding nearly 62% of the global share. The primary driver for this dominance is consumer preference for physically evaluating cookware products before purchase, particularly in terms of weight, finish, and build quality. Supermarkets, hypermarkets, and specialty kitchen stores remain key sales channels, especially in regions where traditional retail infrastructure is well established.

However, online retail is rapidly gaining momentum and is expected to be the fastest-growing distribution channel over the forecast period. The growth is driven by increasing internet penetration, convenience of home delivery, competitive pricing, and access to a wider variety of products. E-commerce platforms are also leveraging customer reviews, product comparisons, and digital marketing strategies to influence purchasing decisions, particularly among younger consumers and urban populations.

End-Use Insights

The residential segment dominates the frying pan market, accounting for approximately 70% of total demand. This dominance is driven by the global rise in home cooking, influenced by health awareness, cost-saving considerations, and lifestyle changes. Increasing urbanization and the proliferation of nuclear families are further contributing to the demand for household cookware, particularly in emerging economies.

The commercial segment, which includes restaurants, hotels, catering services, and cloud kitchens, is the fastest-growing end-use category. Expansion of the global foodservice industry, coupled with the rapid growth of online food delivery platforms, is significantly boosting demand for high-performance, durable frying pans. Commercial users prioritize longevity and efficiency, driving demand for premium and heavy-duty cookware solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Frying Pan Market Segmentations

By Material Type

- Aluminum Frying Pans

- Stainless Steel Frying Pans

- Cast Iron Frying Pans

- Copper Frying Pans

- Carbon Steel Frying Pans

- Ceramic Frying Pans

By Coating Type

- Non-Stick Coating

- Ceramic Coating

- Uncoated/Traditional Surface

By Price Range

- Economy Segment

- Mid-Range Segment

- Premium Segment

By Distribution Channel

- Online Retail

- Supermarkets & Hypermarkets

- Specialty Kitchen Stores

- Department Stores

- Brand-Owned Stores/Websites

By End-Use

- Residential/Household

- Restaurants

- Hotels

- Catering Services

- Institutional Kitchens

Regional Insights

Asia-Pacific

Asia-Pacific leads the global frying pan market with approximately 42% share in 2025, making it the largest and fastest-growing regional market with a CAGR exceeding 7%. China dominates as both a major manufacturing hub and exporter, benefiting from large-scale production capabilities, cost advantages, and established global supply chains. India is emerging as a high-growth market due to rising disposable incomes, rapid urbanization, and increasing penetration of modern retail and e-commerce platforms. Additionally, government initiatives promoting domestic manufacturing and expanding middle-class consumption are further accelerating demand. The region’s growth is also supported by a large population base and increasing adoption of modular kitchens.

North America

North America accounts for approximately 22% of the global market share, with the United States being the primary contributor. The region’s growth is driven by strong consumer preference for premium cookware, high awareness regarding product quality and safety, and a well-established retail infrastructure. Increasing demand for non-toxic and eco-friendly cookware, along with the widespread adoption of induction cooktops, is further boosting market growth. Additionally, the presence of leading global brands and continuous product innovation are key drivers in this region.

Europe

Europe holds nearly 20% of the global market share, with major markets including Germany, France, and the UK. The region’s growth is strongly influenced by sustainability trends and stringent regulatory standards related to chemical coatings and food safety. Consumers in Europe show a high preference for eco-friendly, durable, and premium cookware products, driving demand for ceramic-coated and stainless steel frying pans. Furthermore, the region benefits from a strong culture of home cooking and culinary traditions, which sustains consistent demand for high-quality cookware.

Latin America

Latin America contributes around 8% of the global market, with Brazil and Mexico leading regional demand. The growth in this region is primarily driven by urbanization, rising disposable incomes, and the expansion of organized retail channels. Increasing adoption of modern kitchen appliances and cookware among middle-income households is also supporting market growth. Additionally, local manufacturing and import expansion are improving product availability and affordability across the region.

Middle East & Africa

The Middle East & Africa region accounts for approximately 8% of the market share. Growth in this region is largely driven by increasing investments in the hospitality and tourism sectors, particularly in countries such as the UAE and Saudi Arabia. Rising urbanization, improving living standards, and growing demand for modern kitchenware among households are also contributing to market expansion. In Africa, countries like South Africa are witnessing steady growth due to improving retail infrastructure and increasing consumer awareness. The expansion of international hotel chains and foodservice outlets is further boosting demand for commercial-grade frying pans.

Key Players in the Frying Pan Market

- Groupe SEB

- TTK Prestige

- Meyer Corporation

- Newell Brands

- Tramontina

- Fissler

- Scanpan

- All-Clad

- Le Creuset

- Lodge Manufacturing

- Hawkins Cookers

- Vinod Cookware

- BergHOFF

- GreenPan

- Cuisinart