French Doors Market Size

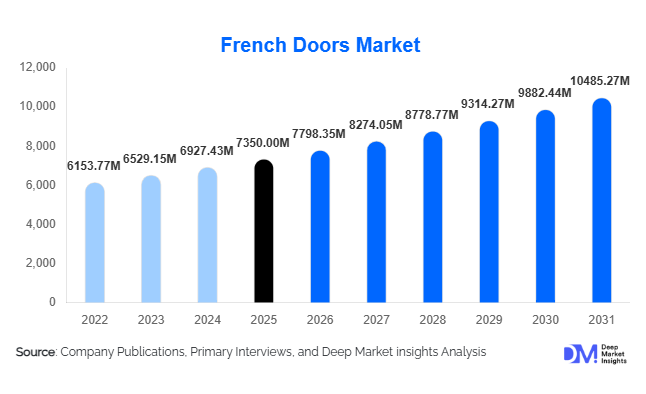

According to Deep Market Insights, the global French doors market size was valued at USD 7,350 million in 2025 and is projected to grow from USD 7,798.35 million in 2026 to reach USD 10,485.27 million by 2031, expanding at a CAGR of 6.1% during the forecast period (2026–2031). The market growth is primarily driven by increasing urbanization, rising residential and commercial construction, and growing preference for aesthetically appealing, energy-efficient, and functional door solutions across the globe.

Key Market Insights

- Rising adoption of energy-efficient and low-maintenance materials such as uPVC and aluminum is driving the French doors market, particularly in residential and commercial buildings.

- Double French doors dominate high-end residential and commercial projects due to their wide openings, premium aesthetics, and functionality.

- Europe leads the market with Germany, France, and the U.K. being the largest consumers, while APAC is emerging as the fastest-growing region, driven by China and India.

- Smart home integration is creating premium opportunities, with automated locks, multi-point systems, and app-controlled access becoming increasingly popular.

- Residential end-use remains the largest segment, accounting for around 60% of global demand in 2025, fueled by urban housing growth and renovations.

- Technological advancements in composite materials, thermal insulation, and sustainable designs are reshaping consumer preferences and increasing adoption globally.

What are the latest trends in the French doors market?

Shift Toward Energy-Efficient and Sustainable Materials

Manufacturers are increasingly producing French doors using energy-efficient uPVC, aluminum, and composite materials to meet growing environmental standards and consumer demand for sustainable housing solutions. These materials offer thermal insulation, low maintenance, and resistance to corrosion or moisture, making them ideal for modern urban and luxury residential projects. Regulatory incentives in Europe and APAC for energy-efficient building materials are further accelerating adoption. Premium wooden French doors are also being treated with eco-friendly coatings and finishes to enhance durability while appealing to sustainability-conscious consumers.

Smart and Automated French Doors

Integration with smart home systems is transforming French doors from purely aesthetic and functional elements into high-tech home components. Features such as app-controlled locks, multi-point locking systems, and automated sliding mechanisms are increasingly demanded in high-end residential and commercial projects. This trend is particularly pronounced in North America and Europe, where smart home adoption is higher. Automation not only increases convenience but also enhances security and energy efficiency, positioning French doors as a premium upgrade in modern constructions.

What are the key drivers in the French doors market?

Increasing Residential and Commercial Construction

The growth of urbanization, rising disposable incomes, and expanding real estate sectors are driving French door adoption. Luxury apartments, villas, office spaces, and hotels are increasingly choosing French doors for their aesthetic appeal, natural light facilitation, and ventilation benefits. Construction activity in emerging economies like India, China, and Brazil is particularly boosting demand for cost-effective yet stylish uPVC and aluminum options.

Rising Preference for Premium Design and Functionality

Consumers and developers are increasingly favoring French doors due to their ability to combine style with functionality. Thermal insulation, soundproofing, and security features make them desirable for mid- to high-end projects. European and North American markets show strong adoption of premium wooden and aluminum doors in residential and hospitality applications, reflecting the market’s focus on aesthetics and long-term durability.

Technological Innovations in Materials and Security

Advanced manufacturing techniques, including reinforced frames, energy-efficient glass, and smart locking systems, are enhancing the performance and longevity of French doors. These innovations are boosting market growth by appealing to tech-savvy and design-conscious consumers, particularly in the premium segment.

What are the restraints for the global market?

High Initial Costs

French doors, especially premium wooden or smart-automated models, involve a higher upfront investment compared to conventional doors. This limits adoption in price-sensitive markets, particularly in developing countries where cost remains a significant barrier.

Maintenance Challenges for Certain Materials

Wooden French doors require regular upkeep to prevent damage from moisture, pests, or environmental wear, while aluminum doors can require periodic maintenance to avoid corrosion in coastal regions. High-maintenance concerns can deter adoption in areas where long-term upkeep is challenging.

What are the key opportunities in the French doors market?

Smart Home Integration

With the global rise of smart homes, integrating automated and app-controlled French doors presents a high-value growth opportunity. Features such as remote access, multi-point locking, and sensors can create a premium segment that appeals to high-income residential and commercial customers.

Emerging Markets Expansion

Rapid urbanization and growth in emerging economies like India, China, and Brazil are driving demand for stylish and functional French doors. Government housing initiatives and rising disposable incomes make these regions critical opportunities for both new entrants and established players. Localized production and distribution strategies can capture early mover advantages in these fast-growing markets.

Sustainable and Energy-Efficient Solutions

As environmental awareness grows, energy-efficient French doors using uPVC, composite, or treated wood are gaining traction. These solutions appeal to eco-conscious consumers and help developers meet stricter building codes and energy regulations, presenting opportunities for product differentiation and premium pricing.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7350 Million |

| Market Size in 2026 | USD 7798.35 Million |

| Market Size in 2031 | USD 10485.27 Million |

| CAGR | 6.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Double French doors dominate the global market, accounting for approximately 50% of the total market share in 2025. Their leadership is primarily driven by strong adoption in premium residential properties, luxury villas, hospitality establishments, and commercial buildings that require wider entryways and enhanced architectural aesthetics. Double doors enable greater natural light penetration, improved ventilation, and seamless connectivity between indoor and outdoor living spaces, making them particularly attractive in modern residential construction and hospitality infrastructure projects. Additionally, developers increasingly prefer double French doors in luxury apartments, resorts, and boutique hotels where aesthetic design and open-space layouts are prioritized.

From a material perspective, uPVC French doors lead the market with around 35% share, supported by their affordability, durability, and superior thermal insulation properties. uPVC doors are particularly popular in energy-efficient housing projects and urban residential developments. Wooden French doors account for roughly 30% of the market, largely driven by their premium aesthetic appeal and widespread use in luxury homes and heritage-style buildings. Meanwhile, aluminum and composite French doors collectively represent about 35%, gaining traction due to their structural strength, corrosion resistance, and suitability for commercial and coastal environments. Aluminum doors are increasingly favored in large commercial spaces because of their slim profiles and modern design compatibility.

Application Insights

The residential segment dominates the French doors market with nearly 60% of total demand in 2025. This dominance is primarily attributed to rising urban housing development, home renovation activities, and growing consumer preference for aesthetically pleasing architectural features. French doors are commonly used in living rooms, patios, balconies, and garden entrances in residential properties, enabling improved natural lighting and ventilation. The surge in luxury housing developments and high-end apartment complexes across North America, Europe, and parts of Asia-Pacific has further strengthened residential demand. Additionally, the growing popularity of open-concept living spaces in modern home designs continues to drive the adoption of French doors in residential architecture.

The commercial segment accounts for approximately 25% of the market, supported by demand from hotels, office buildings, restaurants, retail outlets, and hospitality infrastructure. In the hospitality sector, French doors are widely installed in luxury hotels, resorts, and boutique accommodations to enhance aesthetic appeal while offering seamless outdoor access to patios, gardens, or balconies. Office buildings and premium retail outlets are also increasingly adopting French doors to create open and visually appealing environments that improve natural lighting and customer experience.

Explore more data points, trends and opportunities Download Free Sample Report

French Doors Market Segmentations

By Product Type

- Single French Doors

- Double French Doors

- Sliding French Doors

- Bi-Fold French Doors

By Material Type

- uPVC French Doors

- Wooden French Doors

- Aluminum French Doors

- Composite French Doors

By Application

- Residential Buildings

- Commercial Buildings

- Institutional and Public Infrastructure

By Distribution Channel

- Direct Sales (Manufacturers and Contractors)

- Specialty Door & Window Retailers

- Online Retail and E-commerce Platforms

- Construction Material Distributors

Regional Insights

North America

North America accounts for approximately 30% of the global French doors market, with the United States representing the largest share within the region. Strong demand is primarily driven by a well-established residential renovation market and high spending on home improvement projects. In the U.S., homeowners frequently upgrade doors and windows to improve energy efficiency, aesthetics, and property value, which significantly supports the demand for French doors. Canada also contributes to regional growth through increasing residential construction activity and government initiatives promoting energy-efficient building materials.

Another key driver in North America is the widespread adoption of smart home technologies, where automated doors with integrated locking systems and security features are becoming increasingly popular. The region also benefits from the strong presence of leading manufacturers, advanced distribution networks, and higher consumer willingness to invest in premium home design elements.

Europe

Europe holds the largest share of the global market at approximately 40%, with major demand coming from Germany, France, the United Kingdom, Italy, and Spain. The region has a long architectural tradition of incorporating French doors in residential and commercial buildings, which sustains strong replacement and renovation demand. Strict energy efficiency regulations and building performance standards across the European Union are also encouraging the adoption of insulated door systems, particularly uPVC and aluminum French doors.

Additionally, Europe’s mature construction market and high consumer preference for aesthetic architectural features contribute to consistent demand. Renovation of historic buildings and heritage properties across Western Europe further drives installations of wooden French doors that preserve traditional design aesthetics. Government incentives for energy-efficient housing upgrades are another major factor supporting market expansion in this region.

Asia-Pacific

The Asia-Pacific region is the fastest-growing market, expanding at an estimated CAGR of around 7%. Rapid urbanization, increasing disposable incomes, and large-scale residential construction activities in countries such as China and India are major drivers of market growth. China leads regional demand due to extensive real estate development and the expansion of urban housing infrastructure, while India is experiencing rising adoption of premium architectural products in high-end residential projects.

Japan and Australia represent relatively mature markets within the region and contribute primarily through premium housing and renovation demand. Increasing adoption of modern Western-style home designs across urban Asian markets is further supporting the demand for French doors. Moreover, the Asia-Pacific has become a significant manufacturing hub for doors and window systems, enabling export-driven growth in the regional industry.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth driven by luxury real estate development and expanding tourism infrastructure. Countries such as the United Arab Emirates and Saudi Arabia are investing heavily in high-end residential communities, hotels, and mixed-use commercial developments, where French doors are widely used to enhance architectural aesthetics and provide access to outdoor spaces such as terraces and courtyards.

Large-scale urban development projects and government-led initiatives such as Saudi Arabia’s Vision 2031 are further supporting construction activity in the region. In Africa, countries like South Africa are witnessing gradual growth due to rising urban housing development and growing demand for modern architectural designs in urban centers.

Latin America

Latin America represents a smaller share of the global market but is gradually expanding, with Brazil, Mexico, and Argentina emerging as key demand centers. Urban housing expansion and growing middle-class consumer spending are supporting the adoption of French doors in residential construction projects. Brazil leads regional demand due to its large construction industry and increasing preference for aesthetically designed residential properties.

In Mexico, proximity to the United States construction supply chain has facilitated increased adoption of premium building materials, including French doors. Meanwhile, Argentina and Chile are witnessing moderate growth driven by urban infrastructure development and a gradual recovery in the housing sector. Although economic fluctuations continue to impact construction activity in the region, long-term demand for modern architectural products is expected to sustain market growth.

Key Players in the French Doors Market

- Andersen Corporation

- Pella Corporation

- Masonite International

- JELD-WEN Holding, Inc.

- Marvin Windows and Doors

- Atrium Windows and Doors

- Simpson Door Company

- ODL, Inc.

- Reliability (Lowe’s)

- Milgard Manufacturing, Inc.

- ThermoTech Windows

- Harvia Doors

- Eurocell plc

- Saint-Gobain Glass

- KMC Doors