Forceps and Spatulas Market Size

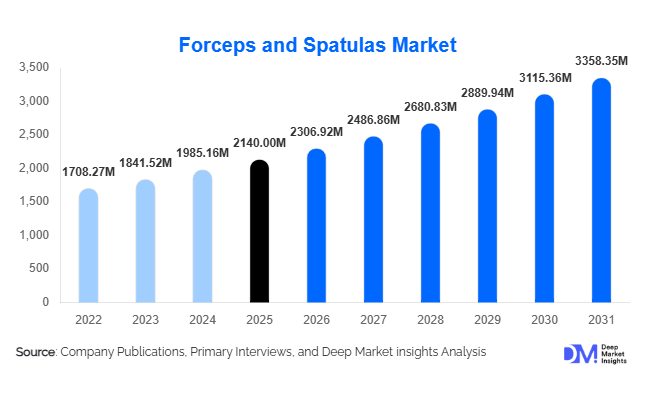

According to Deep Market Insights, the global forceps and spatulas market size was valued at USD 2,140 million in 2025 and is projected to grow from USD 2,306.92 million in 2026 to reach USD 3,358.35 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The market growth is primarily driven by the rising volume of surgical procedures worldwide, expanding healthcare infrastructure in emerging economies, and increasing adoption of precision surgical instruments across hospitals, ambulatory surgical centers, and research laboratories.

Forceps and spatulas are critical handheld surgical instruments used for tissue handling, surgical manipulation, and laboratory material transfer. They are widely applied across medical specialties including general surgery, neurosurgery, obstetrics and gynecology, dentistry, and pharmaceutical research. Growing prevalence of chronic diseases such as cardiovascular disorders, orthopedic conditions, and cancer is significantly increasing the demand for surgical procedures, which in turn drives consistent consumption of these instruments.

The market is also benefiting from technological advancements in surgical instrument manufacturing. Innovations such as titanium-based instruments, anti-corrosion coatings, ergonomic handles, and micro-surgical forceps are improving surgical precision and clinical outcomes. Additionally, the increasing shift toward minimally invasive surgeries and outpatient surgical procedures is expanding the adoption of specialized surgical tools.

Key Market Insights

- Forceps account for the majority of market demand, representing nearly 68% of total revenue due to their extensive use across surgical procedures.

- Stainless steel instruments dominate the material segment, supported by durability, sterilization compatibility, and cost efficiency.

- North America holds the largest market share, driven by advanced healthcare infrastructure and high surgical procedure volumes.

- Asia-Pacific is the fastest-growing region, fueled by healthcare expansion in China, India, and Southeast Asia.

- Reusable surgical instruments remain dominant, though disposable variants are gaining traction due to infection control protocols.

- Hospitals represent the largest end-use segment, accounting for more than half of global demand for surgical instruments.

What are the latest trends in the forceps and spatulas market?

Rising Adoption of Disposable Surgical Instruments

Healthcare facilities are increasingly adopting disposable surgical instruments to minimize infection risks and simplify sterilization procedures. Single-use forceps and spatulas are particularly gaining traction in ambulatory surgical centers and high-volume hospital environments where rapid patient turnover requires efficient instrument management. Disposable variants also help reduce cross-contamination risks and comply with stringent infection control protocols. Manufacturers are investing in cost-effective polymer and medical-grade plastic instruments that provide similar precision and functionality as reusable metal tools. As healthcare systems prioritize patient safety and operational efficiency, the disposable surgical instruments segment is expected to expand rapidly.

Advancements in Microsurgical Instruments

The growing adoption of minimally invasive and microsurgical procedures is driving demand for highly precise surgical tools. Microsurgical forceps used in neurosurgery, ophthalmology, and reconstructive surgery require extremely fine tips, anti-slip grip designs, and lightweight materials such as titanium. Innovations in surgical instrument engineering are enabling improved dexterity and control for surgeons performing complex procedures. Additionally, the integration of robotic-assisted surgery systems is encouraging the development of specialized instruments compatible with robotic platforms. These advancements are improving surgical accuracy while reducing tissue damage and recovery time for patients.

What are the key drivers in the forceps and spatulas market?

Increasing Global Surgical Procedure Volumes

The rising number of surgical procedures worldwide remains the most significant growth driver for the forceps and spatulas market. Aging populations, increasing chronic disease prevalence, and improved access to healthcare services are contributing to higher surgical intervention rates. Orthopedic surgeries, cardiovascular procedures, and cancer-related operations have increased steadily over the past decade. Each surgical procedure requires multiple handheld instruments, including forceps and spatulas, creating consistent demand across hospitals and surgical centers globally.

Expansion of Ambulatory Surgical Centers

Ambulatory surgical centers (ASCs) are rapidly expanding across healthcare systems due to their cost efficiency and ability to perform outpatient procedures. These facilities require compact surgical instrument sets for high-volume procedures such as orthopedic surgeries, cosmetic surgeries, and minor gynecological operations. ASCs often prefer disposable instruments to simplify sterilization and logistics. The continued shift of surgical procedures from traditional hospitals to outpatient facilities is therefore significantly increasing demand for forceps and spatulas.

What are the restraints for the global market?

Skill Requirements for Specialized Surgical Instruments

Some types of forceps, particularly obstetric forceps used in assisted vaginal deliveries, require specialized training and experience for safe usage. In certain regions, reduced training exposure for these procedures has limited the adoption of such instruments. As a result, alternative methods such as cesarean delivery or vacuum extraction may be preferred in some healthcare systems.

Availability of Alternative Surgical Technologies

Technological innovations in surgical procedures, including robotic-assisted systems and automated surgical devices, may reduce reliance on traditional manual instruments in some specialized procedures. While forceps and spatulas remain essential for most surgeries, the adoption of advanced surgical systems may slightly impact demand for certain conventional tools.

What are the key opportunities in the forceps and spatulas industry?

Growth in Emerging Healthcare Markets

Emerging economies in Asia-Pacific, Latin America, and the Middle East present substantial growth opportunities for surgical instrument manufacturers. Countries such as China, India, Indonesia, Brazil, and Saudi Arabia are investing heavily in healthcare infrastructure and expanding hospital networks. Government initiatives aimed at improving surgical care access and reducing maternal mortality are increasing procurement of essential surgical instruments including forceps and spatulas. The construction of new hospitals and specialty clinics in these regions will continue to drive market demand.

Development of Advanced Materials and Coatings

Advancements in materials technology offer significant opportunities for manufacturers to differentiate their products. Titanium instruments, ceramic surgical tools, and PTFE-coated surfaces provide improved durability, corrosion resistance, and enhanced handling precision. Surgeons increasingly prefer instruments that offer ergonomic design, lightweight construction, and superior grip control. Companies that invest in advanced materials and precision manufacturing technologies can capture premium market segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2140 Million |

| Market Size in 2026 | USD 2306.92 Million |

| Market Size in 2031 | USD 3358.35 Million |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Forceps dominate the product category, contributing approximately 68% of global market revenue. These instruments are essential in surgical procedures for grasping, holding, and manipulating tissues or medical materials. Tissue forceps and dissecting forceps are the most widely used types, owing to their versatility across various surgical disciplines. Spatulas account for the remaining market share and are primarily utilized in laboratory settings, pharmaceutical compounding, and specialized surgical procedures. Double-ended and spoon spatulas are commonly used in laboratories for mixing compounds and transferring materials. The global expansion of research laboratories and pharmaceutical manufacturing, along with the increasing focus on precision in experimental and clinical work, is expected to drive steady growth in the demand for high-precision laboratory spatulas over the coming years.

Application Insights

General surgery remains the largest application segment due to the extensive use of forceps in routine surgical procedures. Obstetrics and gynecology continue to represent an important segment, driven by the persistent use of obstetric forceps in assisted deliveries and gynecological surgeries. The cardiovascular and neurosurgery segments are experiencing rising demand for high-precision micro-forceps, reflecting the need for delicate tissue manipulation in complex procedures. Dental surgery and plastic surgery are also witnessing growth, as specialized forceps and micro-spatulas are increasingly used for fine procedural work. Across all applications, the primary driver is the rising volume of surgical procedures and the growing emphasis on minimally invasive techniques, which require specialized instruments.

Distribution Channel Insights

Direct institutional sales remain the largest distribution channel in the forceps and spatulas market, as hospitals and healthcare systems typically purchase surgical instruments directly from manufacturers or authorized distributors to ensure quality and compliance. Medical device distributors are key players in supplying instruments to smaller clinics and ambulatory surgical centers, where procurement volumes are lower but demand for specialized tools remains high. Emerging online medical equipment platforms allow healthcare facilities to access a wider variety of surgical instruments and compare pricing across multiple manufacturers, providing convenience and cost efficiency. Group purchasing organizations (GPOs) increasingly influence procurement by negotiating bulk purchasing agreements, allowing healthcare institutions to optimize costs while maintaining consistent instrument quality.

End-Use Insights

Hospitals represent the largest end-use segment, accounting for roughly 55% of global demand for forceps and spatulas, due to their wide range of surgical procedures and requirement for comprehensive surgical instrument sets. Ambulatory surgical centers are the fastest-growing segment, driven by the global shift toward outpatient surgical care, which emphasizes cost efficiency and rapid procedural turnover, often relying on disposable or semi-disposable instruments. Academic and research laboratories also hold a significant share, with laboratory spatulas in particular being vital for chemical handling, pharmaceutical research, and experimental procedures. The growth in end-use is primarily driven by increasing surgical volumes, expanding outpatient care facilities, and rising investment in research and development infrastructure across both public and private sectors.

Explore more data points, trends and opportunities Download Free Sample Report

Forceps and Spatulas Market Segmentations

By Product Category

- Forceps

- Spatulas

By Forceps Type

- Tissue Forceps

- Dissecting Forceps

- Dressing Forceps

- Hemostatic Forceps

- Micro Forceps

- Obstetric Forceps

- Iris Forceps

- Splinter / Foreign Body Forceps

By Spatula Type

- Laboratory Spatulas

- Surgical Spatulas

- Micro Spatulas

- Double-Ended Spatulas

- Spoon Spatulas

- Pharmaceutical Compounding Spatulas

By Application

- General Surgery

- Obstetrics & Gynecology

- Cardiovascular Surgery

- Neurosurgery

- Plastic & Reconstructive Surgery

- Orthopedic Surgery

- Dental Surgery

- Laboratory and Pharmaceutical Handling

By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Academic & Research Laboratories

- Pharmaceutical & Biotechnology Companies

By Distribution Channel

- Direct Institutional Sales

- Medical Device Distributors

- Online Medical Equipment Platforms

- Group Purchasing Organizations (GPOs)

Regional Insights

North America

North America holds the largest share of the global forceps and spatulas market, accounting for approximately 34% of total revenue. The United States dominates regional demand due to its advanced healthcare infrastructure, high surgical procedure volumes, and a large network of hospitals and ambulatory surgical centers. Continuous investment in healthcare technology, coupled with a strong emphasis on minimally invasive and high-precision surgical procedures, drives the adoption of advanced forceps and spatulas. In Canada, government initiatives supporting healthcare modernization and surgical capacity expansion contribute significantly to market growth. The region’s leadership is further strengthened by stringent quality standards and strong presence of medical device manufacturers.

Europe

Europe represents around 28% of global market demand, with Germany, the United Kingdom, France, and Italy leading the regional market. Germany is a dominant player, supported by its strong medical device manufacturing industry, extensive hospital network, and focus on innovative surgical instruments. The United Kingdom and France maintain robust demand due to publicly funded healthcare systems that support high surgical procedure volumes. Across Europe, the growth in surgical instrument adoption is driven by the increasing prevalence of chronic diseases requiring surgical intervention, advancements in minimally invasive surgeries, and strong government funding for hospital infrastructure and medical research.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, fueled by the rapid expansion of healthcare infrastructure, rising surgical procedure volumes, and increasing adoption of advanced surgical instruments in China, India, Japan, and South Korea. China is investing heavily in hospital construction, modern surgical facilities, and large-scale medical device procurement programs. India is witnessing significant growth due to the expansion of private healthcare networks, rising medical tourism, and increasing affordability of surgical care. Japan and South Korea are contributing through high adoption rates of precision surgical instruments driven by aging populations and advanced healthcare technologies. Overall, the primary growth drivers in this region are rising healthcare expenditure, increasing surgical volumes, and government initiatives supporting healthcare modernization.

Latin America

Latin America is experiencing steady growth in demand for surgical instruments, particularly in Brazil and Mexico. Brazil’s large public healthcare system performs millions of surgeries annually, creating strong demand for surgical instruments, while government initiatives are enhancing hospital capacity. Mexico benefits from growing medical tourism and the expansion of private healthcare facilities, which increases the need for specialized surgical tools. Regional growth is driven by rising healthcare investments, increasing access to surgical care, and adoption of modern instruments in both public and private hospitals.

Middle East & Africa

The Middle East and Africa region is gradually expanding its surgical instrument market due to increased healthcare investments and infrastructure development. Saudi Arabia and the United Arab Emirates lead regional demand through large-scale hospital construction projects and government healthcare development programs focused on modern surgical care. South Africa remains the largest market in Africa, supported by relatively advanced healthcare infrastructure and a growing number of private hospitals. Key growth drivers include rising government healthcare expenditure, modernization of hospital facilities, and increasing focus on advanced surgical procedures across the region.

Key Players in the Forceps and Spatulas Market

- B. Braun Melsungen AG

- Johnson & Johnson (Ethicon)

- Medtronic plc

- Integra LifeSciences

- CONMED Corporation

- Stryker Corporation

- Teleflex Incorporated

- CooperSurgical Inc.

- KLS Martin Group

- Sklar Surgical Instruments

- Medline Industries

- BD (Becton Dickinson)

- Richard Wolf GmbH

- Symmetry Surgical

- Aspen Surgical