Food Thermometer Market Size

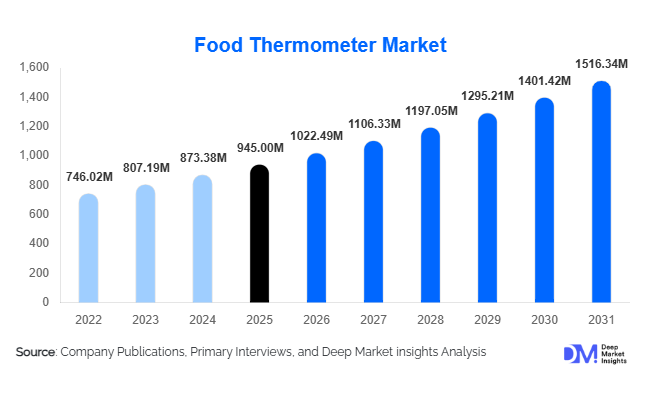

According to Deep Market Insights, the global food thermometer market size was valued at USD 945 million in 2025 and is projected to grow from USD 1,022.49 million in 2026 to reach USD 1,516.34 million by 2031, expanding at a CAGR of 8.2% during the forecast period (2026–2031). The food thermometer market growth is primarily driven by increasing food safety awareness, rising demand for precision cooking, and stringent regulatory compliance requirements across the global foodservice and food processing industries.

Key Market Insights

- Digital food thermometers dominate the market, accounting for over 65% share due to accuracy, speed, and advanced features such as instant-read and connectivity.

- Commercial end-use leads demand, with restaurants, QSRs, and food processing units driving over 50% of global consumption.

- North America dominates the global market, supported by strict food safety regulations and high consumer awareness.

- Asia-Pacific is the fastest-growing region, driven by rapid expansion of QSR chains and increasing food safety compliance.

- Smart and wireless thermometers are gaining traction, supported by IoT integration and mobile app connectivity.

- Mid-range products (USD 15–50) dominate, balancing affordability and functionality across residential and commercial users.

What are the latest trends in the food thermometer market?

Adoption of Smart and Connected Thermometers

The food thermometer market is witnessing rapid adoption of smart and connected devices equipped with Bluetooth and Wi-Fi capabilities. These thermometers allow users to monitor food temperature remotely through mobile applications, enabling convenience and precision in both residential and commercial kitchens. Integration with smart home ecosystems and cooking appliances is further enhancing the appeal of these devices. Advanced features such as real-time alerts, predictive cooking guidance, and cloud-based data tracking are transforming traditional thermometers into intelligent cooking tools. This trend is particularly strong among tech-savvy consumers and professional chefs who prioritize accuracy and automation.

Growing Emphasis on Food Safety and Compliance

Rising global awareness regarding foodborne illnesses is driving demand for reliable temperature monitoring solutions. Governments and regulatory bodies are enforcing stricter food safety standards, compelling restaurants, food processors, and catering services to adopt accurate thermometers. Compliance with standards such as HACCP is becoming mandatory across many regions, especially in North America and Europe. This trend is pushing demand for high-precision, calibrated thermometers with data logging capabilities. Additionally, increased inspections and audits in commercial kitchens are reinforcing the need for consistent temperature monitoring practices.

What are the key drivers in the food thermometer market?

Expansion of Global Foodservice Industry

The rapid growth of the global foodservice industry, particularly quick-service restaurants (QSRs), cloud kitchens, and catering services, is a major driver for the food thermometer market. These establishments require consistent temperature monitoring to ensure food quality, safety, and regulatory compliance. As foodservice revenues continue to expand globally, demand for thermometers is increasing proportionately. The rise of online food delivery platforms and dark kitchens is further amplifying the need for standardized cooking processes, thereby boosting thermometer adoption.

Rising Consumer Interest in Precision Cooking

Consumers are increasingly embracing precision cooking techniques such as grilling, baking, and sous vide, which require accurate temperature control. This has significantly increased the adoption of digital and smart thermometers in households. Social media influence, cooking shows, and culinary experimentation are encouraging consumers to invest in reliable cooking tools. The growing popularity of home-based gourmet cooking and baking trends is further supporting market growth, particularly in developed economies.

What are the restraints for the global market?

Price Sensitivity in Emerging Markets

In price-sensitive markets such as India, Southeast Asia, and parts of Latin America, the adoption of advanced food thermometers is limited by affordability constraints. While premium smart thermometers offer enhanced features, their higher price points restrict widespread usage among small-scale users and households. This creates a gap between product availability and actual adoption in developing regions.

Proliferation of Low-Quality and Counterfeit Products

The presence of low-cost, unbranded, and counterfeit thermometers in the market poses a significant challenge. These products often lack accuracy and durability, leading to inconsistent performance and reduced consumer trust. The widespread availability of such products in local markets and online platforms can negatively impact brand reputation and hinder the growth of established manufacturers.

What are the key opportunities in the food thermometer industry?

Integration with Smart Kitchen Ecosystems

The increasing adoption of smart kitchens presents a significant opportunity for manufacturers to develop connected thermometers that integrate with appliances such as smart ovens, grills, and cooking platforms. IoT-enabled thermometers that offer app-based monitoring, voice assistant compatibility, and automated cooking recommendations can unlock premium market segments. This integration enhances user convenience and positions thermometers as essential components of modern kitchens.

Growth in Emerging Markets

Emerging economies such as China, India, and Brazil offer substantial growth opportunities due to expanding foodservice industries and rising food safety awareness. The proliferation of QSR chains, organized retail, and cloud kitchens is driving demand for reliable temperature monitoring solutions. Companies can capitalize on this opportunity by offering cost-effective products tailored to local market conditions while ensuring compliance with international standards.

Expansion in Food Processing and Cold Chain Logistics

The growing global trade in perishable food items is driving demand for temperature monitoring solutions in food processing and cold chain logistics. Food thermometers are increasingly being integrated into storage and transportation systems to maintain product quality and comply with export regulations. Industrial-grade thermometers with data logging and traceability features are gaining traction in this segment, offering long-term growth potential for market participants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 945 Million |

| Market Size in 2026 | USD 1022.49 Million |

| Market Size in 2031 | USD 1516.34 Million |

| CAGR | 8.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Digital food thermometers continue to dominate the global market, accounting for approximately 68% of the total market share in 2025, primarily driven by their superior accuracy, rapid response time, and ability to deliver instant-read measurements that are critical in both commercial and residential cooking environments. The increasing integration of advanced technologies such as Bluetooth and Wi-Fi connectivity, along with compatibility with mobile applications, has further enhanced their usability by enabling real-time monitoring and remote temperature tracking. This technological advancement is particularly appealing to professional chefs and tech-savvy consumers seeking precision and convenience. In addition, the growing emphasis on food safety standards and the need to minimize risks associated with undercooked or overcooked food are accelerating the adoption of digital thermometers across foodservice establishments. While analog thermometers maintain a presence in cost-sensitive and traditional markets due to their affordability and simplicity, their slower response time and comparatively lower precision limit their competitiveness. The continuous innovation in smart kitchen devices and the rising popularity of connected cooking ecosystems are expected to further strengthen the leadership of digital food thermometers over the forecast period.

Application Insights

The meat and poultry segment leads the application category, accounting for nearly 38% of the global market share in 2025, with its dominance primarily driven by the critical requirement for precise temperature monitoring to ensure food safety and compliance with health regulations. The high risk of foodborne illnesses associated with improperly cooked meat products has made temperature measurement an essential practice in both commercial kitchens and households, thereby reinforcing the segment’s leading position. Additionally, increasing consumer awareness regarding safe cooking practices and the expansion of quick-service restaurants and meat processing facilities are further fueling demand in this segment. Other applications such as bakery, confectionery, beverages, and frying are also witnessing steady growth, supported by the rising popularity of specialty cooking, artisanal baking, and gourmet food preparation. The growing trend of home-based culinary experimentation and professional-grade cooking standards among consumers is further contributing to the broader adoption of food thermometers across diverse applications.

Distribution Channel Insights

Offline retail channels continue to dominate the global food thermometer market, capturing approximately 60% share, largely due to their strong presence across supermarkets, hypermarkets, specialty kitchen stores, and hospitality supply outlets. These channels provide consumers with the advantage of physical product evaluation, immediate purchase, and access to expert guidance, which is particularly important for commercial buyers and first-time users. However, the rapid expansion of e-commerce platforms is significantly transforming the distribution landscape, with online retail emerging as the fastest-growing channel. Factors such as increasing internet penetration, convenience of doorstep delivery, availability of a wide range of products, and competitive pricing are driving the shift toward online purchasing. Moreover, direct-to-consumer sales through brand-owned websites are gaining traction, especially for premium and technologically advanced thermometers, as manufacturers seek to enhance customer engagement, offer personalized experiences, and improve profit margins by reducing reliance on intermediaries.

End-Use Insights

The commercial segment holds a dominant position in the market, accounting for around 55% of the global market share in 2025, driven by extensive demand from restaurants, hotels, catering services, and food processing industries where maintaining precise temperature control is essential for operational efficiency and regulatory compliance. Stringent food safety regulations imposed by health authorities, along with the need to ensure consistent food quality across large-scale operations, are key factors supporting the adoption of food thermometers in this segment. Additionally, the rapid growth of the global foodservice industry and the expansion of organized retail and hospitality sectors are further reinforcing demand. The residential segment, while smaller in comparison, is witnessing steady growth due to increasing consumer interest in home cooking, baking, and grilling. Rising disposable incomes, evolving lifestyles, and the growing influence of cooking shows and digital content are encouraging consumers to adopt professional-grade kitchen tools, including food thermometers, thereby supporting segment expansion.

Price Range Insights

Mid-range food thermometers priced between USD 15–50 dominate the market, holding approximately 46% share, as they offer an optimal balance between affordability and functionality, making them highly attractive to both residential users and small-to-medium commercial establishments. These products typically provide reliable accuracy, user-friendly interfaces, and essential features such as quick response times, which are sufficient for most cooking applications. The strong demand for mid-range products is driven by their cost-effectiveness and widespread availability across both offline and online channels. At the same time, premium products are gaining traction, particularly among professional chefs and tech-oriented consumers, due to their advanced features such as wireless connectivity, app integration, and enhanced durability. Conversely, low-cost products continue to maintain relevance in developing markets where price sensitivity remains high, although their growth is comparatively limited by lower performance and reduced feature sets.

Explore more data points, trends and opportunities Download Free Sample Report

Food Thermometer Market Segmentations

By Product Type

- Digital Food Thermometers

- Analog Food Thermometers

- Infrared (Non-contact) Thermometers

- Smart/Bluetooth/Wi-Fi Thermometers

By Application

- Meat & Poultry

- Bakery & Confectionery

- Beverages

- Oil & Frying

- Dairy & Frozen Food Monitoring

By Distribution Channel

- Online Retail

- Supermarkets & Hypermarkets

- Specialty Kitchen Stores

- Institutional/B2B Sales

By End-Use

- Household/Residential

- Restaurants & QSRs

- Hotels & Catering

- Food Processing Industry

- Food Safety Inspection Agencies

Regional Insights

North America

North America holds the largest share of the global food thermometer market, accounting for approximately 34% in 2025, with the United States serving as the primary growth engine. The region’s dominance is supported by stringent food safety regulations enforced by government authorities, which mandate accurate temperature monitoring across foodservice and processing industries. High consumer awareness regarding food hygiene and safety, coupled with widespread adoption of advanced kitchen technologies, further contributes to market expansion. The strong presence of established restaurant chains, quick-service restaurants, and large-scale food processing companies significantly drives demand for reliable and high-precision thermometers. Additionally, the growing trend of smart kitchens and connected home devices is encouraging the adoption of digital and app-enabled thermometers. Increasing participation in outdoor cooking activities such as grilling and barbecuing also acts as a key driver for residential demand in the region.

Europe

Europe accounts for around 27% of the global market share, driven by robust demand from countries including Germany, the United Kingdom, and France. The region benefits from strict regulatory frameworks related to food safety and hygiene, which require precise temperature control in both commercial and industrial food operations. A well-established food processing industry, along with strong export activities, further supports the adoption of food thermometers. Additionally, European consumers exhibit a high preference for premium and technologically advanced products, leading to increased demand for smart and digital thermometers. The growing popularity of gourmet cooking, artisanal food production, and sustainable food practices also contributes to market growth. Furthermore, continuous innovation by regional manufacturers and the integration of advanced features into kitchen tools are enhancing product adoption across the region.

Asia-Pacific

Asia-Pacific represents the fastest-growing region in the global food thermometer market and is expected to register a CAGR of over 9.5% during the forecast period. Rapid urbanization, rising disposable incomes, and the expansion of the middle-class population are key factors driving market growth in countries such as China and India. The increasing presence of quick-service restaurant chains, coupled with the growing popularity of international cuisines, is significantly boosting demand for food thermometers. In addition, rising awareness of food safety standards and government initiatives aimed at improving food quality are encouraging adoption across both commercial and residential sectors. Mature markets such as Japan and South Korea demonstrate strong demand for technologically advanced and high-precision devices, driven by consumer preference for quality and innovation. The rapid growth of e-commerce platforms and improved distribution networks further facilitate market penetration across the region.

Latin America

Latin America is experiencing moderate growth in the food thermometer market, with Brazil and Mexico emerging as key contributors. The region’s expansion is driven by increasing food exports, which necessitate adherence to international food safety standards and temperature monitoring practices. Improvements in regulatory frameworks and growing awareness of food hygiene are further supporting market development. Additionally, the gradual expansion of the foodservice industry, including restaurants and catering services, is contributing to increased demand for food thermometers. Economic development and rising urbanization are also encouraging the adoption of modern kitchen appliances among consumers, thereby supporting residential segment growth.

Middle East & Africa

The Middle East & Africa region is gradually expanding, supported by the rapid growth of the hospitality and tourism sectors, particularly in countries such as the United Arab Emirates and Saudi Arabia. The increasing number of hotels, restaurants, and large-scale catering services is driving demand for food thermometers to ensure compliance with food safety standards. Rising investments in foodservice infrastructure and the growing influence of international dining trends are further contributing to market growth. Additionally, increasing awareness of food hygiene practices and government initiatives aimed at improving food quality and safety are encouraging adoption across the region. The expansion of organized retail and the gradual penetration of e-commerce platforms are also playing a role in improving product accessibility and market reach.

Key Players in the Food Thermometer Market

- ThermoWorks

- Weber Inc.

- Taylor Precision Products

- OXO

- Maverick Industries

- CDN (Component Design Northwest)

- Fluke Corporation

- Testo SE & Co. KGaA

- Hanna Instruments

- Polder Products

- Lavatools

- Inkbird Tech

- ETI Ltd

- Cooper-Atkins Corporation

- AcuRite