Food Processor Market Size

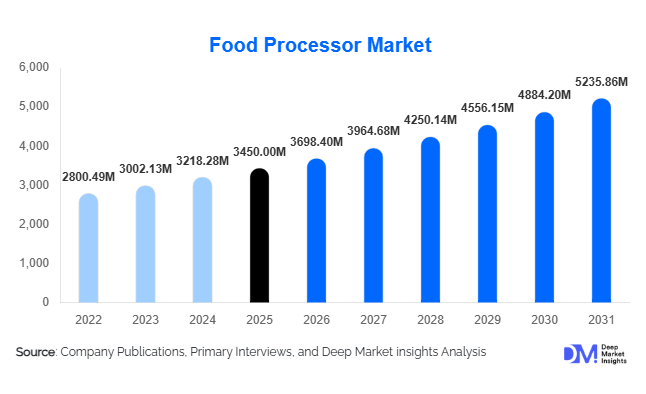

According to Deep Market Insights, the global food processor market size was valued at USD 3,450 million in 2025 and is projected to grow from USD 3,698.40 million in 2026 to reach USD 5,235.86 million by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The food processor market growth is primarily driven by increasing demand for kitchen automation, rising disposable incomes, and the growing preference for time-saving cooking appliances among urban households. Additionally, the expansion of commercial foodservice establishments and the rising popularity of home cooking are further accelerating market demand globally.

Key Market Insights

- Multifunctional food processors are gaining popularity, enabling users to perform multiple kitchen tasks such as chopping, slicing, grinding, and kneading using a single appliance.

- Asia-Pacific dominates the global market, supported by rising middle-class populations and increasing appliance penetration in countries like China and India.

- Residential applications account for the largest share, driven by the growing adoption of convenient kitchen solutions in urban households.

- Online retail channels are expanding rapidly, supported by e-commerce growth and increasing consumer preference for digital purchasing.

- Mid-range products lead the market, offering a balance between affordability and advanced features.

- Technological advancements, including smart controls and energy-efficient motors, are transforming product innovation and user experience.

What are the latest trends in the food processor market?

Shift Toward Smart and Connected Appliances

The food processor market is witnessing a strong shift toward smart and connected appliances. Manufacturers are integrating IoT-enabled features, app-based controls, and AI-powered recipe suggestions into food processors. These innovations enhance convenience and user experience, allowing consumers to automate cooking processes and customize settings remotely. Smart appliances are particularly gaining traction in developed markets, where consumers are willing to invest in technologically advanced kitchen solutions. Additionally, integration with smart home ecosystems is enabling seamless connectivity with other kitchen devices, further driving adoption.

Rising Demand for Compact and Multifunctional Designs

Consumers are increasingly favoring compact and multifunctional food processors that save space and reduce the need for multiple appliances. This trend is especially prominent in urban areas with limited kitchen space. Multifunctional processors that combine blending, grinding, juicing, and kneading capabilities are gaining widespread popularity. Manufacturers are focusing on ergonomic designs, easy-to-clean components, and energy-efficient motors to meet evolving consumer preferences. This trend is expected to continue, particularly in emerging markets where affordability and versatility are key purchasing factors.

What are the key drivers in the food processor market?

Growing Demand for Convenience and Time Efficiency

The increasing number of dual-income households and busy lifestyles is driving demand for time-saving kitchen appliances. Food processors significantly reduce food preparation time, making them an essential tool for modern kitchens. Consumers are prioritizing convenience and efficiency, leading to higher adoption rates across both residential and commercial sectors.

Expansion of the Foodservice Industry

The rapid growth of restaurants, hotels, and cloud kitchens is boosting demand for commercial-grade food processors. These establishments require efficient and high-capacity appliances to maintain consistency and productivity. The rise of online food delivery platforms and quick-service restaurants is further fueling this demand, particularly in urban centers.

What are the restraints for the global market?

High Cost of Advanced Models

Premium and multifunctional food processors often come with high price tags, limiting their adoption in price-sensitive markets. While basic models are affordable, advanced units with smart features and high power ratings remain expensive, restricting their penetration in developing regions.

Availability of Substitute Appliances

The presence of alternative appliances such as mixer grinders, blenders, and manual tools poses a challenge to market growth. In many regions, especially in Asia, consumers prefer multifunctional appliances that can perform similar tasks at a lower cost, reducing the demand for dedicated food processors.

What are the key opportunities in the food processor industry?

Expansion in Emerging Markets

Emerging economies present significant growth opportunities due to rising disposable incomes, urbanization, and increasing awareness about kitchen appliances. Countries in Asia-Pacific and Africa are witnessing a surge in demand, driven by first-time buyers and growing middle-class populations. Manufacturers can capitalize on this trend by offering affordable and durable products tailored to local needs.

Growth of Commercial Foodservice and Cloud Kitchens

The rapid expansion of cloud kitchens and quick-service restaurants is creating demand for high-capacity and efficient food processors. These establishments require automation to reduce labor costs and improve operational efficiency. This trend is expected to drive significant growth in the commercial segment over the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3450 Million |

| Market Size in 2026 | USD 3698.40 Million |

| Market Size in 2031 | USD 5235.86 Million |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Full-size food processors continue to dominate the global market, accounting for approximately 38% of the total share in 2025. This leadership is primarily driven by their high versatility and multifunctionality, enabling users to perform a wide range of kitchen tasks such as chopping, slicing, kneading, blending, and grinding within a single appliance. These processors cater to both residential and commercial users, making them the most practical and cost-efficient solution for bulk food preparation. Additionally, their larger capacity and higher power ratings make them ideal for households with higher consumption needs and for foodservice establishments requiring operational efficiency.

Mini and compact food processors are witnessing increasing adoption, particularly in urban markets where space optimization and portability are key purchasing factors. These models are gaining traction among nuclear families and single-person households. Meanwhile, multifunctional food processors are emerging as a strong growth segment, driven by the rising demand for all-in-one kitchen appliances that reduce the need for multiple devices, thereby saving both cost and space. Commercial-grade food processors are also expanding rapidly, supported by the growth of quick-service restaurants (QSRs), cloud kitchens, and catering services, where automation and consistency are critical operational requirements.

Application Insights

Chopping and slicing applications hold the largest share of approximately 30% in the global market, primarily because these functions represent the most frequent and time-consuming tasks in both residential and commercial kitchens. The dominance of this segment is driven by the need for speed, precision, and uniformity in food preparation, especially in high-volume cooking environments such as restaurants and food processing units.

Mixing and kneading applications are experiencing steady growth, fueled by the rising popularity of home baking and the expansion of commercial bakeries. The growing influence of Western cuisines and increased consumption of bakery products globally have further supported this segment. Pureeing and grinding functions are also gaining traction, particularly in emerging markets, where demand for ready-to-cook and processed food products is increasing. The ability of food processors to seamlessly switch between multiple applications enhances their overall value proposition, making them indispensable in modern kitchens.

Distribution Channel Insights

Offline retail channels dominate the food processor market, accounting for around 58% of total sales in 2025. This dominance is largely attributed to consumer preference for physical product evaluation, live demonstrations, and immediate purchase assurance. Specialty appliance stores and large-format retail outlets play a crucial role in influencing buying decisions, particularly for mid-range and premium products.

However, online retail is the fastest-growing segment, driven by the rapid expansion of e-commerce platforms and increasing digital penetration. Consumers are increasingly attracted to competitive pricing, wider product selection, customer reviews, and doorstep delivery. Additionally, the rise of direct-to-consumer (D2C) strategies by manufacturers is enabling brands to improve margins, enhance customer engagement, and offer personalized promotions. The integration of augmented reality (AR) and virtual product demos is further enhancing the online shopping experience, accelerating this shift.

End-Use Insights

The residential segment leads the market with approximately 62% share in 2025, driven by increasing adoption of kitchen appliances among urban households. The primary growth driver for this segment is the rising demand for convenience, time-saving solutions, and home cooking trends, particularly among working professionals and nuclear families. Increased awareness and affordability of kitchen appliances in emerging economies are also contributing to segment growth.

The commercial foodservice segment is the fastest-growing, supported by the rapid expansion of restaurants, hotels, and cloud kitchens. The need for high efficiency, consistency, and reduced labor dependency is driving adoption in this segment. Additionally, the food processing industry is witnessing growing demand for automated equipment to meet increasing global consumption of packaged and processed foods. Export-driven demand for processed food products, especially from countries like China and India, is further boosting the use of industrial-grade food processors.

Explore more data points, trends and opportunities Download Free Sample Report

Food Processor Market Segmentations

By Product Type

- Full-Size Food Processors

- Mini / Compact Food Processors

- Handheld / Immersion Food Processors

- Multifunctional Food Processors

- Commercial-Grade Food Processors

By Application

- Chopping

- Slicing & Shredding

- Mixing & Kneading

- Pureeing

- Grinding & Milling

By Distribution Channel

- Online Retail

- Supermarkets/Hypermarkets

- Specialty Appliance Stores

- Multi-brand Retail Stores

By End-Use

- Residential / Household

- Commercial Foodservice

- Food Processing Industry

Regional Insights

Asia-Pacific

Asia-Pacific is the largest market, accounting for approximately 34% of the global share in 2025, with China and India being the primary contributors. The region’s dominance is driven by rapid urbanization, rising disposable incomes, and expanding middle-class populations. Increasing penetration of modern retail and e-commerce platforms has significantly improved product accessibility. Additionally, the growth of the foodservice sector, particularly cloud kitchens and quick-service restaurants, is driving commercial demand. Government initiatives supporting domestic manufacturing, such as “Make in India” and “Made in China 2026,” are also boosting local production and market expansion.

North America

North America holds around 28% of the global market, with the United States leading demand. The region’s growth is driven by high consumer awareness, strong purchasing power, and a well-established kitchen appliance market. There is a strong preference for premium and technologically advanced products, including smart and connected food processors. Additionally, the widespread adoption of automation in commercial kitchens and the presence of major market players contribute to sustained growth. Increasing demand for healthy and home-cooked meals is further supporting residential adoption.

Europe

Europe accounts for approximately 25% of the market, with Germany, the UK, and France as key contributors. The region’s growth is primarily driven by strict energy efficiency regulations and strong consumer preference for sustainable and eco-friendly appliances. High adoption of premium products and increasing demand for multifunctional appliances are also supporting market expansion. Additionally, the presence of established brands and strong distribution networks enhances market penetration across the region.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth, supported by rapid urbanization, rising disposable incomes, and expanding hospitality and tourism sectors. Countries such as the UAE and Saudi Arabia are key growth markets due to increasing investments in hotels, restaurants, and catering services. The growing expatriate population and changing dietary habits are also contributing to increased adoption of kitchen appliances. Additionally, government initiatives to diversify economies beyond oil are driving investments in foodservice and retail sectors.

Latin America

Latin America shows moderate growth, with Brazil and Mexico leading demand. The region’s expansion is driven by rising middle-class populations, improving economic conditions, and increasing urbanization. Growing awareness about modern kitchen appliances and the expansion of retail infrastructure are supporting market growth. Additionally, the increasing popularity of processed and convenience foods is driving demand for food processors in both residential and commercial segments.

Key Players in the Food Processor Market

- Philips

- Whirlpool Corporation

- Panasonic Corporation

- Breville Group

- Cuisinart

- KitchenAid

- Bosch (BSH Home Appliances)

- Kenwood

- Hamilton Beach Brands

- Black+Decker

- Morphy Richards

- Bajaj Electricals

- Preethi Kitchen Appliances

- TTK Prestige

- Havells India