Food Processing Lighting Market Size

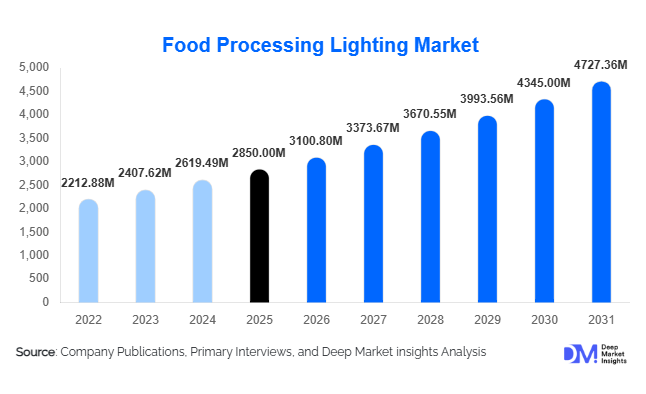

According to Deep Market Insights, the global food processing lighting market size was valued at USD 2,850 million in 2025 and is projected to grow from USD 3,100.80 million in 2026 to reach USD 4,727.36 million by 2031, expanding at a CAGR of 8.8% during the forecast period (2026–2031). The food processing lighting market growth is primarily driven by increasing global demand for processed food, stringent food safety regulations, and rapid adoption of energy-efficient LED lighting systems across industrial food facilities.

Key Market Insights

- LED lighting dominates the market, accounting for nearly 68% share, driven by energy efficiency, durability, and compliance with hygiene standards.

- Hygienic and washdown lighting solutions are witnessing strong demand, especially in meat and dairy processing facilities requiring IP69K-rated fixtures.

- Asia-Pacific dominates the global market, supported by rapid food processing industrialization in China and India.

- Retrofit installations are gaining traction globally, as existing facilities upgrade to energy-efficient and compliant lighting systems.

- Smart lighting integration is emerging rapidly, with IoT-enabled systems enhancing operational monitoring and predictive maintenance.

- Export-driven food processing industries are accelerating demand for high-compliance lighting systems globally.

What are the latest trends in the food processing lighting market?

Adoption of Hygienic and IP-Rated Lighting Systems

Food processing facilities are increasingly adopting lighting systems designed specifically for hygienic environments. IP65, IP66, and IP69K-rated fixtures are becoming standard, particularly in wet and high-pressure washdown zones. These lighting systems are built to resist corrosion, prevent contamination from glass breakage, and withstand harsh cleaning chemicals. Manufacturers are also incorporating antimicrobial coatings and seamless designs to eliminate dirt accumulation points. This trend is particularly prominent in meat, poultry, and dairy processing industries, where contamination risks are high. As global food safety standards tighten, hygienic lighting solutions are transitioning from optional upgrades to mandatory infrastructure components in modern processing facilities.

Integration of Smart and Connected Lighting

The adoption of smart lighting systems integrated with IoT platforms is transforming food processing environments. These systems enable real-time monitoring of energy consumption, temperature, and operational performance, helping facilities optimize efficiency and reduce downtime. Predictive maintenance capabilities are minimizing unexpected failures, while automated lighting adjustments based on occupancy and production schedules are improving energy savings. Integration with broader Industry 4.0 frameworks is enabling centralized control of lighting systems alongside other plant operations. This trend is particularly appealing to large-scale food manufacturers seeking to enhance productivity, reduce operational costs, and meet sustainability targets.

What are the key drivers in the food processing lighting market?

Stringent Food Safety Regulations

Regulatory frameworks such as HACCP, FDA guidelines, and international food safety standards are mandating the use of specialized lighting systems in food processing environments. These regulations require shatterproof, sealed, and contamination-resistant lighting fixtures to ensure product safety. As compliance becomes more stringent globally, food manufacturers are increasingly investing in advanced lighting systems that meet certification requirements, thereby driving market growth.

Expansion of the Global Processed Food Industry

The rapid growth of the processed food sector, valued at over USD 3 trillion globally, is significantly boosting demand for food processing infrastructure, including lighting systems. Rising urbanization, changing lifestyles, and increasing consumption of ready-to-eat foods are driving the expansion of food processing facilities worldwide. This directly translates into higher demand for specialized lighting solutions designed for industrial environments.

Shift Toward Energy Efficiency and Sustainability

Energy-efficient lighting solutions, particularly LEDs, are being widely adopted due to their ability to reduce energy consumption by up to 60% compared to traditional lighting systems. Governments and corporations are focusing on sustainability goals, encouraging the transition toward low-energy, long-lasting lighting solutions. This shift is further supported by declining LED prices and favorable government incentives.

What are the restraints for the global market?

High Initial Investment Costs

Advanced lighting systems, especially LED and smart lighting solutions designed for food processing environments, require significant upfront investment. Small and medium-sized enterprises often face budget constraints, limiting adoption despite long-term cost benefits. The need for specialized installation and compliance certification further adds to initial expenses.

Complex Regulatory Compliance

Meeting diverse regulatory standards across different regions can be challenging for manufacturers and end-users. Variations in certification requirements, safety standards, and inspection protocols increase complexity, particularly for companies operating in multiple international markets. This can slow down implementation and increase operational costs.

What are the key opportunities in the food processing lighting industry?

Expansion in Emerging Markets

Emerging economies such as India, Brazil, and Southeast Asian countries are experiencing rapid growth in food processing industries. Government initiatives, infrastructure development, and rising consumer demand for packaged foods are creating significant opportunities for lighting manufacturers. Establishing local production and distribution networks in these regions can provide a competitive advantage and unlock new revenue streams.

Growth of Smart Lighting Solutions

The increasing adoption of Industry 4.0 technologies in food processing plants is opening opportunities for smart lighting systems. IoT-enabled lighting solutions offer benefits such as predictive maintenance, energy optimization, and improved operational efficiency. Companies investing in advanced lighting technologies with integrated sensors and automation capabilities are well-positioned to capitalize on this trend.

Rising Demand for Hygienic Lighting Solutions

As food safety standards become more stringent globally, demand for hygienic lighting solutions is expected to grow significantly. Lighting systems with high ingress protection ratings, corrosion resistance, and antimicrobial properties are becoming essential in food processing environments. This creates opportunities for manufacturers specializing in high-performance, compliance-focused lighting products.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2850 Million |

| Market Size in 2026 | USD 3100.80 Million |

| Market Size in 2031 | USD 4727.36 Million |

| CAGR | 8.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Technology Insights

LED lighting systems continue to dominate the food processing lighting market, accounting for approximately 68% of the global share in 2025. The leadership of this segment is primarily driven by its superior energy efficiency, reducing power consumption by up to 50–60% compared to conventional systems, along with extended operational lifespan exceeding 50,000 hours. Additionally, LED fixtures are inherently more compatible with hygienic design requirements, including sealed housings, shatterproof construction, and resistance to moisture and chemical exposure, making them ideal for food-grade environments. Regulatory compliance with standards such as HACCP and IP69K has further accelerated adoption. Fluorescent and HID lighting systems are steadily losing market share due to higher maintenance costs, shorter lifespan, and environmental concerns related to mercury content. Meanwhile, induction lighting remains a niche segment, utilized in specialized industrial settings requiring extremely long service intervals. The continued decline in LED pricing, coupled with government-backed energy efficiency initiatives, is expected to further strengthen the dominance of LED technology globally.

Application Insights

Processing areas represent the largest application segment, accounting for approximately 35% of the global market share in 2025. This segment leads due to the critical need for high-intensity, uniform, and contamination-resistant lighting to ensure product quality, operational accuracy, and worker safety during core manufacturing processes. The increasing automation of processing lines and integration of machine vision systems are further driving demand for high-performance lighting solutions in these areas. Packaging and inspection zones also hold significant shares, supported by the growing importance of quality control and traceability in food production. Storage and warehousing facilities, including cold storage units, are increasingly adopting energy-efficient LED lighting to reduce operational costs and maintain optimal visibility under low-temperature conditions. Cleanrooms and hygienic zones are emerging as the fastest-growing application areas, driven by rising demand for contamination-free environments in high-value food segments such as dairy, ready-to-eat meals, and nutraceuticals.

End-Use Industry Insights

The meat, poultry, and seafood processing segment leads the market with an estimated 28% share in 2025, primarily driven by stringent hygiene standards, high regulatory scrutiny, and the need for robust washdown lighting systems. These facilities require specialized lighting capable of withstanding frequent cleaning cycles, exposure to moisture, and corrosive agents. The dairy processing segment is another key contributor, experiencing steady growth due to rising global consumption of milk and dairy products, particularly in the Asia-Pacific. The bakery and confectionery segment is expanding consistently, supported by increasing demand for packaged and convenience foods. Beverage processing, including both alcoholic and non-alcoholic segments, is also contributing significantly, driven by large-scale automated bottling and packaging lines. Emerging sectors such as plant-based foods, nutraceuticals, and ready-to-eat meals are creating new demand for advanced, hygienic lighting systems, particularly in cleanroom and controlled environments.

Distribution Channel Insights

Direct sales dominate the food processing lighting market, accounting for approximately 60% of total revenue in 2025. This dominance is attributed to the project-based nature of lighting installations in large-scale food processing facilities, where customized solutions, technical consultations, and compliance certifications are required. Manufacturers often work directly with food processing companies, engineering firms, and contractors to deliver tailored lighting systems. Distributors and wholesalers play a crucial role in regional markets, particularly for small and medium-sized enterprises that require standardized lighting products and faster delivery timelines. Meanwhile, online sales channels are gradually gaining traction, especially for replacement lighting, spare parts, and smaller-scale installations. The growth of e-commerce platforms and digital procurement systems is expected to enhance accessibility and streamline purchasing processes in the coming years.

Explore more data points, trends and opportunities Download Free Sample Report

Food Processing Lighting Market Segmentations

By Technology

- LED Lighting Systems

- Fluorescent Lighting Systems

- High-Intensity Discharge (HID) Lighting

- Induction Lighting

By Product Type

- Waterproof & Washdown Lights (IP Rated)

- High Bay Lights

- Low Bay Lights

- Linear Strip Lights

- Panel Lights

- Explosion-Proof Lighting

- Emergency & Backup Lighting

By Application

- Processing Areas

- Packaging Areas

- Storage & Warehousing

- Inspection & Quality Control

- Cleanrooms & Hygienic Zones

By End-Use Industry

- Meat, Poultry & Seafood Processing

- Dairy Processing

- Bakery & Confectionery

- Beverages

- Fruits & Vegetable Processing

- Ready-to-Eat / Packaged Food

By Distribution Channel

- Direct Sales

- Distributors & Wholesalers

- Online / E-commerce

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global food processing lighting market, accounting for approximately 38% of the total share in 2025. The region’s leadership is driven by rapid industrialization, expanding food processing capacity, and strong export-oriented manufacturing. China leads the region due to its large-scale food production and government-backed industrial modernization programs such as “Made in China 2026,” which emphasize automation and energy efficiency. India is the fastest-growing market, with a CAGR exceeding 10%, supported by initiatives like “Make in India,” increasing foreign direct investment, and the rapid expansion of cold chain infrastructure. Rising domestic consumption of processed foods and growing export demand are further boosting lighting installations. Japan and South Korea contribute through advanced, automated processing facilities that require high-quality, precision lighting systems. Overall, the region benefits from a combination of cost advantages, government incentives, and increasing adoption of modern food processing technologies.

North America

North America holds approximately 26% of the global market share, driven by stringent regulatory frameworks and high levels of technological adoption. The United States dominates the region, supported by strict food safety standards enforced by regulatory bodies, which mandate the use of hygienic and shatterproof lighting systems. The widespread adoption of LED technology, coupled with a strong focus on sustainability and energy efficiency, is a key growth driver. Additionally, the presence of large, well-established food processing companies and continuous investment in facility upgrades and automation are fueling demand. Canada also contributes significantly, particularly in the dairy and meat processing industries, where modernization and compliance requirements are driving lighting upgrades. The region’s mature market structure and emphasis on innovation continue to support steady growth.

Europe

Europe accounts for approximately 22% of the global market share, with Germany, France, and the United Kingdom leading demand. The region is characterized by advanced food processing infrastructure and a strong focus on sustainability and energy efficiency. Stringent environmental regulations and energy directives are encouraging the replacement of traditional lighting systems with LED solutions. Retrofitting existing facilities is a major growth driver, as companies aim to reduce energy consumption and comply with evolving standards. Additionally, Europe’s strong emphasis on food quality, traceability, and hygiene is driving demand for high-performance lighting systems in processing and packaging areas. The presence of leading lighting manufacturers and continuous technological innovation further supports market expansion.

Latin America

Latin America is experiencing steady growth in the food processing lighting market, with Brazil and Mexico emerging as key markets. The region is expected to grow at a CAGR of 7–8% during the forecast period. Growth is primarily driven by strong agricultural output, increasing food exports, and rising investment in food processing infrastructure. Brazil, as a major exporter of meat and agricultural products, is witnessing increased demand for hygienic and durable lighting systems in processing facilities. Mexico is benefiting from its proximity to North American markets, with growing investments in food manufacturing and export-oriented production. Government initiatives to improve industrial infrastructure and attract foreign investment are further supporting market growth in the region.

Middle East & Africa

The Middle East and Africa region is witnessing moderate but steadily increasing growth, driven by food security initiatives and rising investment in domestic food processing capabilities. Countries such as the UAE and Saudi Arabia are investing heavily in food infrastructure to reduce reliance on imports, creating demand for modern lighting systems in newly established processing facilities. In Africa, the growth of agro-processing industries and increasing focus on value-added food production are contributing to market expansion. Additionally, international investments and development programs aimed at improving food supply chains are supporting infrastructure development, including lighting systems. The region’s growth is further supported by rising urbanization and increasing demand for packaged and processed food products.

Key Players in the Food Processing Lighting Market

- Signify N.V.

- Acuity Brands Inc.

- Zumtobel Group

- Hubbell Incorporated

- Dialight plc

- Cree Lighting (IDEAL Industries)

- OSRAM GmbH

- GE Current

- Eaton Corporation

- Fagerhult Group

- Thorn Lighting

- Panasonic Corporation

- Emerson Electric Co.

- Larson Electronics

- Nemalux Inc.