Folding Cartons Packaging Market Size

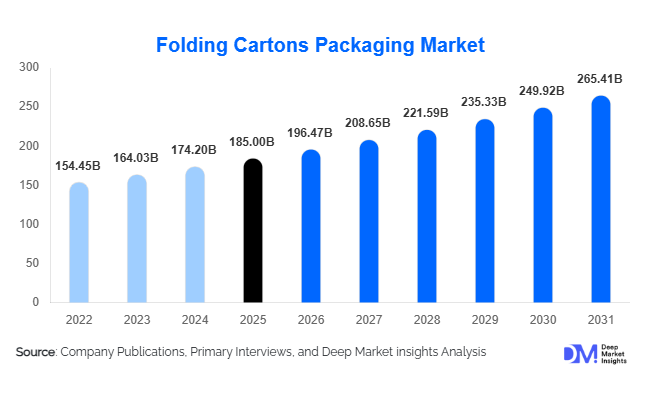

According to Deep Market Insights, the global folding cartons packaging market size was valued at USD 185 billion in 2025 and is projected to grow from USD 196.47 billion in 2026 to reach USD 265.41 billion by 2031, expanding at a CAGR of 6.2% during the forecast period (2026–2031). The folding cartons packaging market growth is primarily driven by rising demand for sustainable packaging solutions, rapid expansion of the food & beverage and pharmaceutical industries, and increasing regulatory pressure to reduce plastic usage globally.

Key Market Insights

- Sustainability-driven demand is reshaping packaging preferences, with folding cartons replacing plastic-based secondary packaging across multiple industries.

- Food & beverages remain the dominant end-use segment, driven by rising consumption of packaged and convenience foods globally.

- Asia-Pacific dominates global demand, supported by large-scale manufacturing, export-oriented industries, and rising consumer goods consumption.

- Pharmaceutical packaging is witnessing rapid growth, fueled by global healthcare expansion and strict regulatory labeling requirements.

- Technological advancements in printing and coating are enabling high-quality branding and improved functional performance of cartons.

- E-commerce expansion is boosting demand for durable, lightweight, and customizable folding carton solutions.

What are the latest trends in the folding cartons packaging market?

Shift Toward Sustainable and Recyclable Packaging

One of the most significant trends in the folding cartons packaging market is the accelerating shift toward sustainable and recyclable materials. Brands across the food, personal care, and pharmaceutical industries are replacing plastic-based packaging with paperboard-based folding cartons due to regulatory pressure and consumer preference for eco-friendly solutions. Manufacturers are increasingly adopting FSC-certified paperboard, recycled fiber content, and biodegradable barrier coatings to reduce environmental impact. Governments in Europe and North America are enforcing stricter packaging waste regulations, further accelerating adoption. This sustainability transition is also influencing corporate ESG strategies, making folding cartons a core component of circular packaging systems worldwide.

Digital Printing and Smart Packaging Integration

The adoption of digital printing technologies and smart packaging features is transforming the folding cartons industry. Digital printing enables shorter production runs, cost efficiency, and high customization, making it ideal for e-commerce and premium branding applications. In addition, smart packaging technologies such as QR codes, NFC tags, and augmented reality features are enhancing consumer engagement and traceability. These innovations allow brands to provide product authentication, interactive marketing, and real-time information access. The integration of intelligent packaging is particularly strong in pharmaceuticals and cosmetics, where traceability and brand protection are critical.

What are the key drivers in the folding cartons packaging market?

Expansion of Food, Beverage, and FMCG Industries

The rapid expansion of the global food and beverage industry is a primary driver of folding cartons demand. Rising urbanization, changing lifestyles, and increasing consumption of packaged and ready-to-eat meals are significantly boosting demand for secondary packaging solutions. Folding cartons provide cost efficiency, branding flexibility, and compliance with food safety regulations, making them ideal for FMCG applications. Growth in frozen foods, bakery products, and dairy packaging is particularly strong, especially in emerging economies where retail modernization is accelerating.

Growth of Pharmaceutical and Healthcare Packaging

The pharmaceutical industry is another major growth driver, with increasing demand for secure, tamper-evident, and regulation-compliant packaging. Folding cartons are widely used for secondary pharmaceutical packaging due to their printability, serialization capability, and compatibility with anti-counterfeiting features. Rising global healthcare expenditure, expansion of generic drug markets, and increasing vaccine distribution networks are further supporting market growth. Regulatory requirements for patient information leaflets and labeling also strengthen reliance on folding cartons.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in pulp and paperboard prices remain a key restraint in the folding cartons packaging market. Since paperboard is the primary input material, changes in global pulp supply, energy costs, and logistics expenses directly impact production costs. This creates pricing instability for manufacturers and reduces profit predictability, especially for small and mid-sized converters. Supply chain disruptions and environmental restrictions on pulp sourcing further add to cost pressures.

Limited Barrier Performance Compared to Plastic Alternatives

Despite advancements in coating technologies, folding cartons still face limitations in moisture, oxygen, and grease resistance compared to plastic-based packaging. This restricts their adoption in certain high-barrier applications such as liquid packaging, long-shelf-life food products, and industrial goods. Although barrier-coated cartons are gaining traction, they remain relatively more expensive, limiting large-scale substitution in sensitive packaging categories.

What are the key opportunities in the folding cartons packaging industry?

Expansion in E-commerce and Direct-to-Consumer Packaging

The rapid growth of e-commerce presents a major opportunity for folding carton manufacturers. Online retail requires durable, lightweight, and visually appealing packaging that enhances brand identity and protects products during shipping. Folding cartons are increasingly used for subscription boxes, electronics packaging, cosmetics delivery, and FMCG shipments. The rise of D2C brands is further boosting demand for customized, short-run packaging solutions enabled by digital printing technologies.

Innovations in Barrier Coatings and Functional Packaging

Technological advancements in barrier coatings are unlocking new applications for folding cartons in food packaging. Innovations such as water-based coatings, grease-resistant layers, and oxygen barrier enhancements are enabling cartons to replace flexible plastic packaging in frozen foods and ready-to-eat meals. This shift significantly expands the addressable market and allows manufacturers to enter higher-value packaging segments with improved product protection and shelf-life extension capabilities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 185 Billion |

| Market Size in 2026 | USD 196.47 Billion |

| Market Size in 2031 | USD 265.41 Billion |

| CAGR | 6.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Recycled paperboard remains the dominant material segment in the folding cartons packaging market, accounting for approximately 42% of the global share in 2025. This leadership is primarily driven by its cost efficiency, wide availability, and strong alignment with global sustainability mandates. Increasing regulatory pressure to reduce carbon footprints and improve recyclability has encouraged brands to transition toward recycled content, particularly in high-volume applications such as food packaging and household goods. Additionally, advancements in recycled fiber processing have improved strength, printability, and hygiene standards, making it suitable even for sensitive applications. Among structural formats, straight tuck end (STE) cartons lead with around 28% share, owing to their structural simplicity, ease of assembly, and compatibility with automated packaging lines. These cartons are widely adopted across the pharmaceuticals, cosmetics, and food industries, where high-speed packaging and cost optimization are critical. Their versatility in accommodating various product shapes and sizes further strengthens their dominance.

Meanwhile, specialty paperboards with enhanced barrier properties are emerging as a high-growth segment. The increasing need to replace plastic packaging in moisture- and grease-sensitive applications, particularly in frozen food and ready-to-eat meals, is driving innovation in coated and functional paperboards. This segment is expected to witness above-average growth due to ongoing R&D investments and evolving food safety standards.

Application Insights

The food and beverage segment dominates the folding cartons packaging market with nearly 48% share in 2025, driven by high consumption volumes and the continuous expansion of packaged food categories. The growth of convenience foods, frozen meals, and on-the-go consumption patterns has significantly increased demand for folding cartons that offer durability, branding potential, and compliance with food safety standards. Additionally, the shift toward sustainable food packaging is accelerating the replacement of plastic containers with paper-based alternatives.

Pharmaceutical applications represent one of the fastest-growing segments, supported by rising global healthcare demand, increasing drug production, and stringent regulatory requirements for secondary packaging. Folding cartons are preferred due to their ability to incorporate labeling, tamper-evidence, and serialization features, which are critical for compliance and patient safety. The personal care and cosmetics segment is also expanding rapidly, driven by premiumization trends and the growing importance of packaging aesthetics. Folding cartons enable high-quality printing, embossing, and finishing, making them ideal for brand differentiation in competitive retail environments. The rise of e-commerce beauty brands has further amplified demand for visually appealing and protective packaging solutions.

Distribution Channel Insights

Direct sales dominate the distribution landscape with approximately 65% market share, as large-scale manufacturers and multinational brands prefer long-term contracts with packaging providers. This approach ensures consistent quality, cost stability, and supply chain reliability, particularly for high-volume production requirements. Distributors and converters play a critical role in catering to small and medium enterprises (SMEs), offering flexibility in order volumes and customized solutions. These intermediaries enable market access for regional brands that lack direct procurement capabilities.

E-commerce platforms are emerging as a fast-growing distribution channel, particularly for customized and short-run packaging orders. The rise of direct-to-consumer (D2C) brands has increased demand for low-volume, high-design packaging solutions, which are efficiently serviced through online platforms. This shift is also driving the adoption of digital printing technologies, enabling faster turnaround times and greater customization.

End-Use Industry Insights

The food and beverage industry remains the largest end-user, with a market size exceeding USD 90,000 million in 2025. Growth is driven by increasing consumption of packaged and processed foods, urbanization, and changing dietary habits. The demand for sustainable and recyclable packaging solutions is further reinforcing the adoption of folding cartons in this sector. The pharmaceutical industry is growing at a robust 7% CAGR, supported by expanding global healthcare infrastructure, rising chronic disease prevalence, and increasing pharmaceutical exports. Folding cartons play a critical role in ensuring product safety, regulatory compliance, and supply chain traceability.

Personal care and cosmetics are among the fastest-growing end-use segments, benefiting from rising disposable incomes, premium product positioning, and the growing influence of social media-driven branding. The demand for innovative and visually appealing packaging is significantly contributing to market growth in this segment.

Explore more data points, trends and opportunities Download Free Sample Report

Folding Cartons Packaging Market Segmentations

By Material Type

- Solid Bleached Sulfate

- Recycled Paperboard

- Kraft Paperboard

- Specialty Paperboard

By Structure Type

- Straight Tuck End

- Reverse Tuck End

- Auto-lock Bottom / Crash Lock Bottom

- Sleeve Cartons

- Gable Top Cartons

- Window Patch Cartons

- Hinged Lid Cartons

By Printing Technology

- Offset Printing

- Flexographic Printing

- Digital Printing

- Gravure Printing

By End-Use Industry

- Food & Beverages

- Pharmaceuticals

- Personal Care & Cosmetics

- Household Products

- Electronics

- Tobacco Packaging

By Distribution Channel

- Direct Sales

- Distributors & Converters

- E-commerce Platforms

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global folding cartons packaging market with approximately 38% share in 2025, making it the largest and fastest-growing region. China accounts for over 20% of global demand, driven by its extensive manufacturing base, strong export activity, and large-scale production of consumer goods. The region’s growth is primarily fueled by rapid urbanization, rising disposable incomes, and expanding middle-class populations.

India is emerging as the fastest-growing market in the region, with growth exceeding 7.5% CAGR. Key drivers include the expansion of the FMCG sector, increasing pharmaceutical manufacturing, and supportive government initiatives such as “Make in India,” which encourage domestic production and packaging demand. Additionally, the growth of e-commerce and organized retail is significantly boosting the need for folding cartons across the region.

North America

North America holds around 25% of the global market share, led by the United States. The region’s growth is driven by high consumption of packaged foods, strong presence of leading FMCG and pharmaceutical companies, and advanced packaging technologies. Sustainability regulations and corporate commitments to reduce plastic usage are accelerating the adoption of recyclable folding cartons. Additionally, the well-established e-commerce ecosystem in the U.S. is driving demand for durable and customizable packaging solutions. Investments in automation and digital printing technologies are further enhancing production efficiency and enabling innovation in packaging design.

Europe

Europe accounts for approximately 22% of the global market, with Germany, France, and the UK as major contributors. The region is characterized by stringent environmental regulations and a strong focus on circular economy practices, which are driving the adoption of paper-based packaging solutions. High recycling rates and well-developed waste management infrastructure support the widespread use of folding cartons. Additionally, increasing consumer preference for sustainable packaging and premium products is encouraging manufacturers to invest in high-quality printing and finishing technologies.

Latin America

Latin America represents about 8% of the global market, with Brazil and Mexico leading demand. Growth in this region is driven by increasing urbanization, rising middle-class populations, and the expansion of the retail sector. The growing penetration of packaged food and beverage products is a key factor supporting market expansion. Furthermore, improvements in manufacturing capabilities and investments in packaging infrastructure are enhancing regional production capacity. Export-oriented industries, particularly in food and agriculture, are also contributing to increased demand for folding cartons.

Middle East & Africa

The Middle East & Africa account for approximately 7% of the global market, with the UAE and South Africa as key markets. Growth in this region is driven by rising demand for packaged consumer goods, increasing retail development, and expanding food and beverage industries. In the Middle East, high disposable incomes and growing demand for premium packaged products are supporting market growth. In Africa, improving industrialization, population growth, and increasing investments in manufacturing and packaging infrastructure are creating new opportunities. Additionally, the expansion of modern retail formats and e-commerce platforms is expected to further boost demand for folding cartons in the region.

Key Players in the Folding Cartons Packaging Market

- International Paper Company

- WestRock Company

- Smurfit Kappa Group

- Graphic Packaging International

- Mondi Group

- DS Smith Plc

- Stora Enso

- Mayr-Melnhof Karton AG

- Huhtamaki Oyj

- Nippon Paper Industries

- Oji Holdings Corporation

- Rengo Co., Ltd.

- UPM-Kymmene Corporation

- Sappi Limited

- Cascades Inc.