Fixed Length Seal Market Size

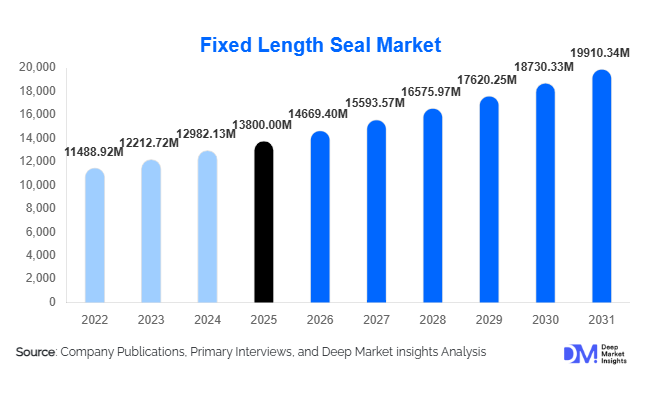

According to Deep Market Insights, the global fixed-length seal market size was valued at USD 13,800 million in 2025 and is projected to grow from USD 14,669.40 million in 2026 to reach USD 19,910.34 million by 2031, expanding at a CAGR of 6.3% during the forecast period (2026–2031). The market growth is primarily driven by increasing industrial automation, rising demand for high-performance sealing solutions, and stringent regulatory standards across industries such as automotive, oil & gas, and aerospace.

Key Market Insights

- Elastomer-based seals dominate the market, accounting for over 40% share due to their versatility and cost-effectiveness across multiple industries.

- O-rings remain the most widely used product type, contributing nearly 35% of total demand owing to ease of installation and broad application scope.

- Asia-Pacific leads the global market, supported by strong manufacturing activity in China, India, and Japan.

- OEM distribution channels dominate, representing around 60% of the market due to long-term supply contracts and quality requirements.

- Automotive is the largest end-use industry, driven by global vehicle production and increasing adoption of electric vehicles.

- Advanced materials and smart sealing technologies are reshaping product innovation and driving premiumization.

What are the latest trends in the fixed-length seal market?

Adoption of Advanced Materials and High-Performance Seals

The market is witnessing a shift toward advanced materials such as PTFE composites, PEEK, and metal-elastomer hybrids. These materials offer superior resistance to extreme temperatures, pressure, and corrosive environments, making them suitable for demanding applications in aerospace, oil & gas, and chemical processing. Manufacturers are increasingly focusing on R&D to develop seals with longer service life, reduced maintenance, and improved operational efficiency. This trend is particularly prominent in high-value applications where performance reliability is critical, driving higher margins and product differentiation.

Integration of Smart Sealing Solutions

Technological integration is transforming traditional sealing systems into smart components. Sensors embedded within seals enable real-time monitoring of wear, leakage, and performance, supporting predictive maintenance strategies. This trend aligns with Industry 4.0 adoption across manufacturing and industrial sectors. Smart seals help reduce downtime, improve safety, and optimize maintenance schedules, creating new revenue streams for manufacturers through digital services and long-term contracts. Increasing demand for connected industrial systems is expected to accelerate the adoption of such technologies.

What are the key drivers in the fixed-length seal market?

Growth in Industrial Automation and Machinery Modernization

The rapid adoption of automation across industries is significantly increasing demand for reliable sealing solutions. Fixed-length seals play a critical role in maintaining system integrity in high-speed, high-pressure environments. As manufacturing facilities upgrade machinery and adopt advanced production systems, the need for precision-engineered seals continues to grow, supporting consistent market expansion.

Stringent Environmental and Safety Regulations

Global regulatory frameworks are becoming increasingly strict regarding emissions, leakage prevention, and workplace safety. Industries such as oil & gas and chemical processing require high-quality sealing solutions to comply with these standards. This regulatory push is driving the adoption of advanced seals that minimize leakage and enhance operational safety, thereby boosting market demand.

What are the restraints for the global market?

Volatility in Raw Material Prices

The fixed-length seal market is highly sensitive to fluctuations in raw material prices, particularly elastomers and specialty polymers derived from petrochemicals. Price volatility impacts production costs and profit margins, posing challenges for manufacturers in maintaining competitive pricing while ensuring product quality.

Intense Competition in Commoditized Segments

Standard sealing products face significant pricing pressure due to competition from low-cost manufacturers, particularly in Asia. This limits profitability and forces companies to differentiate through innovation, customization, and value-added services. Smaller players often struggle to compete with established global manufacturers with strong distribution networks and economies of scale.

What are the key opportunities in the fixed-length seal industry?

Expansion in Emerging Markets

Rapid industrialization in the Asia-Pacific and the Middle East presents significant growth opportunities. Countries such as India and China are investing heavily in infrastructure, manufacturing, and energy projects, driving demand for sealing solutions. Establishing local manufacturing and distribution networks can help companies capitalize on these high-growth regions while reducing operational costs.

Integration with Industry 4.0 and Predictive Maintenance

The integration of sealing solutions with smart technologies and predictive maintenance systems offers substantial growth potential. Manufacturers can develop smart seals equipped with sensors to monitor performance in real time. This not only enhances operational efficiency but also creates recurring revenue streams through maintenance services and digital solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 13800 Million |

| Market Size in 2026 | USD 14669.40 Million |

| Market Size in 2031 | USD 19910.34 Million |

| CAGR | 6.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

O-rings continue to dominate the product segment, accounting for approximately 35% of the global fixed-length seal market in 2025. The leadership of this segment is primarily driven by their design simplicity, low manufacturing cost, and high adaptability across a wide range of sealing environments. O-rings are extensively used in automotive engines, hydraulic systems, and industrial fluid handling applications due to their ability to provide effective sealing under both static and dynamic conditions. Their ease of installation and replacement further enhances their preference among OEMs and aftermarket users.

Gaskets and hydraulic seals also represent substantial market shares, particularly in high-pressure and high-temperature applications such as oil & gas and power generation. These segments are driven by the need for robust sealing solutions capable of withstanding extreme operating environments. Meanwhile, custom-molded fixed-length seals are emerging as a high-growth niche, supported by increasing demand for application-specific and precision-engineered components in aerospace, healthcare, and semiconductor industries. This segment benefits from the ongoing trend toward customization and performance optimization, where standard sealing solutions are insufficient.

Application Insights

Dynamic sealing applications lead the market, contributing approximately 55% of total demand in 2025. The dominance of this segment is driven by the rapid expansion of rotating and reciprocating machinery across industries such as automotive, industrial manufacturing, and oil & gas. Dynamic seals are critical in ensuring operational efficiency by preventing leakage in systems that experience continuous motion, high pressure, and varying temperatures. The increasing complexity of machinery and the need for higher performance standards are further strengthening demand for advanced dynamic sealing solutions.

Static sealing applications remain essential, particularly in industries such as chemical processing, power generation, and water treatment, where leak prevention and long-term system integrity are critical. Growth in this segment is supported by stringent environmental and safety regulations that require zero-leakage systems. Additionally, the integration of advanced materials and improved manufacturing techniques is enhancing the performance of both static and dynamic seals, driving overall market growth.

Distribution Channel Insights

OEM channels dominate the distribution landscape, accounting for nearly 60% of total market sales in 2025. This dominance is primarily driven by the increasing preference for direct procurement agreements between seal manufacturers and equipment producers. OEMs prioritize high-quality, reliable sealing solutions to ensure product performance and reduce warranty risks, leading to long-term supply contracts and stable revenue streams for manufacturers.

The aftermarket segment represents a significant and steadily growing share, driven by maintenance, repair, and replacement demand across aging industrial equipment and automotive fleets. This segment benefits from recurring demand cycles and offers higher margins compared to OEM sales. Industrial distributors continue to play a crucial role in serving small and medium enterprises by providing accessibility to a wide range of sealing products. Furthermore, the rise of digital procurement platforms and e-commerce channels is transforming the distribution landscape, enabling faster sourcing, improved inventory management, and enhanced customer reach.

End-Use Industry Insights

The automotive industry remains the largest end-use segment, contributing approximately 28% of the global market in 2025. This dominance is driven by high global vehicle production, increasing component complexity, and the rapid transition toward electric vehicles (EVs). EVs, in particular, require specialized sealing solutions for battery systems, thermal management, and electronic components, creating new growth avenues for manufacturers.

The oil & gas sector continues to be a major consumer, with demand driven by exploration, refining, and pipeline infrastructure investments. High-performance seals are essential in this industry to ensure safety and efficiency under extreme conditions. Meanwhile, the healthcare and medical devices segment is the fastest-growing, with a CAGR exceeding 7.5%, supported by stringent hygiene standards, increasing adoption of precision equipment, and rising healthcare investments globally. Emerging industries such as renewable energy and semiconductor manufacturing are also contributing to incremental demand, driven by the need for high-purity and high-reliability sealing solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Fixed Length Seal Market Segmentations

By Material Type

- Elastomer-Based Seals

- Thermoplastic Seals

- Metal Seals

- Composite Seals

By Product Type

- O-Rings

- Gaskets

- Shaft Seals

- Hydraulic & Pneumatic Seals

- Lip Seals

- Custom-Molded Fixed Length Seals

By Application

- Static Sealing Applications

- Dynamic Sealing Applications

By Distribution Channel

- OEM

- Aftermarket Sales

- Industrial Distributors

By End-Use Industry

- Automotive

- Aerospace & Defense

- Oil & Gas

- Industrial Machinery

- Chemical Processing

- Power Generation

- Healthcare & Medical Devices

- Food & Beverage Processing

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global fixed-length seal market with approximately 38% share in 2025, making it the largest regional market. China leads regional demand, contributing nearly 18% of the global market, driven by its extensive manufacturing base, strong export-oriented industries, and large-scale industrial production. India is the fastest-growing country in the region, supported by rapid industrialization, infrastructure development, and government initiatives such as “Make in India,” which promote domestic manufacturing and foreign investments. Japan remains a key contributor, particularly in high-precision and advanced manufacturing sectors. The primary drivers of regional growth include expansion of automotive production, rising industrial automation, increasing foreign direct investments, and strong growth in export-oriented manufacturing.

North America

North America accounts for approximately 26% of the global market, with the United States dominating regional demand. The region’s growth is driven by advanced manufacturing capabilities, a strong presence of aerospace and defense industries, and significant investments in oil & gas exploration. Additionally, North America is at the forefront of technological innovation, particularly in the development of smart sealing solutions and high-performance materials. The increasing adoption of Industry 4.0 practices, coupled with a focus on operational efficiency and predictive maintenance, is further boosting demand for advanced sealing systems in the region.

Europe

Europe holds around 22% of the global market share, led by Germany, France, and the United Kingdom. Germany’s strong automotive and industrial manufacturing base makes it a key contributor to regional demand. The region is characterized by stringent environmental regulations and high-quality standards, which drive the adoption of advanced and sustainable sealing solutions. Additionally, Europe’s focus on energy efficiency, renewable energy expansion, and circular economy initiatives is creating demand for high-performance seals in wind energy, chemical processing, and industrial applications. Technological innovation and strong R&D capabilities further support regional growth.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth, driven primarily by large-scale investments in oil & gas infrastructure and energy projects. Countries such as Saudi Arabia and the UAE are key contributors, with increasing demand for high-performance seals in upstream and downstream activities. The region’s growth is also supported by industrial diversification initiatives, petrochemical expansion, and infrastructure development projects. Additionally, rising investments in water treatment and power generation are creating new opportunities for sealing solutions in the region.

Latin America

Latin America represents a smaller but steadily growing market, with Brazil and Mexico as the primary contributors. Growth in the region is driven by expanding automotive production, increasing industrial activity, and rising foreign investments. Infrastructure development and government initiatives aimed at boosting manufacturing capabilities are further supporting demand. Additionally, the presence of oil & gas reserves in countries such as Brazil is contributing to increased demand for high-performance sealing solutions. Despite economic fluctuations, the region offers long-term growth potential due to industrial modernization and increasing integration into global supply chains.

Key Players in the Fixed Length Seal Market

- Trelleborg AB

- Freudenberg Group

- Parker Hannifin Corporation

- SKF Group

- Saint-Gobain

- Flowserve Corporation

- EagleBurgmann

- Garlock Sealing Technologies

- James Walker Group

- NOK Corporation

- Greene Tweed

- Bal Seal Engineering

- Chesterton Company

- Hutchinson SA

- Techno Ad Ltd