Fitness Clothing Market Size

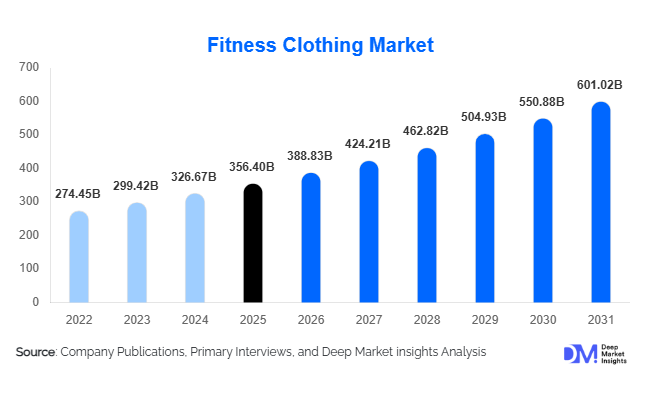

According to Deep Market Insights, the global fitness clothing market size was valued at USD 356.4 billion in 2025 and is projected to grow from USD 388.83 billion in 2026 to reach USD 601.02 billion by 2031, expanding at a CAGR of 9.1% during the forecast period (2026–2031). The fitness clothing market growth is primarily driven by the increasing adoption of athleisure fashion, rising global health awareness, rapid expansion of gym and wellness culture, and growing consumer preference for multifunctional apparel that combines comfort, fashion, and performance. The market has evolved significantly from traditional sportswear into a lifestyle-driven apparel category supported by social media influence, digital fitness ecosystems, and premium activewear innovation.

Key Market Insights

- Athleisure fashion continues to reshape consumer purchasing behavior, with fitness apparel increasingly worn for casual, travel, and workplace environments beyond sports activities.

- Women’s fitness apparel dominates global demand, supported by growing participation in yoga, Pilates, gym memberships, and wellness-focused lifestyles.

- North America leads the global fitness clothing market, driven by premium consumer spending, strong brand penetration, and high fitness participation rates.

- Asia-Pacific remains the fastest-growing regional market, fueled by rising disposable incomes, expanding middle-class populations, and increasing e-commerce penetration.

- Sustainable and recycled activewear is becoming a major industry focus, with consumers increasingly preferring eco-friendly fabrics and ethical manufacturing practices.

- Technology integration is accelerating product innovation, including smart textiles, compression technology, antimicrobial fabrics, and AI-enabled retail personalization.

What are the latest trends in the fitness clothing market?

Sustainable Activewear Becoming Mainstream

The global fitness clothing industry is increasingly shifting toward sustainable manufacturing and environmentally responsible product development. Consumers, particularly millennials and Gen Z demographics, are demanding apparel made from recycled polyester, organic cotton, biodegradable fibers, and low-impact dyes. Major activewear brands are investing heavily in circular production systems, textile recycling initiatives, and carbon-neutral manufacturing facilities to strengthen brand positioning and meet ESG expectations. Sustainability is no longer viewed as a niche feature but as a critical purchasing factor influencing long-term customer loyalty. Companies are also focusing on transparency across supply chains, ethical labor practices, and water-efficient textile processing technologies. The rise of eco-conscious athleisure collections is particularly strong across North America and Europe, where environmentally aware consumers are willing to pay premium prices for sustainable fitness apparel.

Smart and Technology-Integrated Apparel Expansion

Technology-enhanced fitness clothing is emerging as a major innovation trend across the activewear industry. Manufacturers are increasingly integrating moisture-management systems, biometric tracking sensors, antimicrobial coatings, UV protection, and temperature-regulating fabrics into premium apparel categories. Smart activewear connected to fitness ecosystems and wearable technologies is attracting tech-savvy consumers seeking performance optimization and personalized fitness experiences. AI-powered virtual fitting systems, digital customization platforms, and data-driven apparel recommendations are also transforming online retail experiences. Fitness brands are leveraging advanced knitting technologies, seamless construction, and lightweight compression fabrics to improve comfort, durability, and athletic performance. This trend is expected to accelerate further as digital fitness platforms and connected wellness ecosystems continue expanding globally.

What are the key drivers in the fitness clothing market?

Growing Global Health and Wellness Awareness

The increasing global focus on physical fitness, preventive healthcare, and active lifestyles is one of the strongest drivers supporting growth in the fitness clothing market. Rising gym memberships, participation in yoga and home workouts, and expanding interest in sports and outdoor activities are contributing significantly to activewear demand. Consumers are increasingly prioritizing apparel that supports comfort, flexibility, sweat management, and performance enhancement during workouts. Post-pandemic wellness trends have further accelerated demand for fitness-oriented lifestyles, encouraging higher spending on activewear products across both developed and emerging economies.

Rapid Expansion of Athleisure Fashion

Athleisure has transformed fitness apparel from performance-driven sportswear into mainstream fashion. Consumers now regularly wear leggings, hoodies, joggers, sports bras, and performance tops in social, travel, and workplace environments. This crossover between fitness and fashion has substantially expanded the addressable consumer base for activewear manufacturers. Celebrity endorsements, influencer marketing, and social media fitness culture continue driving consumer engagement with premium athleisure brands. Fashion-oriented activewear collaborations and limited-edition collections are also increasing demand among younger demographics seeking both functionality and style.

What are the restraints for the global market?

Volatility in Raw Material Prices

The fitness clothing industry remains highly exposed to fluctuations in textile raw material prices, particularly polyester, nylon, elastane, and performance synthetic fibers. Since many of these materials are linked to petrochemical feedstocks, changes in crude oil prices directly impact production costs and manufacturer profit margins. Sustainable and recycled materials also involve higher sourcing and processing expenses, increasing cost pressures for brands aiming to meet sustainability targets. Smaller and mid-sized manufacturers are particularly vulnerable to pricing volatility due to limited procurement scale and lower supply chain flexibility.

Counterfeit Products and Market Fragmentation

The global activewear industry faces significant challenges from counterfeit products and unorganized regional manufacturers offering low-cost alternatives. Counterfeit fitness apparel negatively impacts premium brands by eroding pricing power and damaging brand reputation. In emerging markets, low-cost imitation products continue to attract price-sensitive consumers, intensifying competitive pressures. Market fragmentation also leads to aggressive discounting strategies, elevated marketing expenditures, and reduced operating margins across the mid-tier activewear segment. Ensuring brand authenticity and supply chain transparency remains a major operational challenge for global fitness apparel companies.

What are the key opportunities in the fitness clothing industry?

Expansion into Emerging Economies

Emerging economies across Asia-Pacific, Latin America, and the Middle East represent major growth opportunities for fitness clothing manufacturers. Countries such as India, Indonesia, Vietnam, Brazil, and Saudi Arabia are witnessing rising middle-class populations, increasing urbanization, and growing health awareness, which are driving activewear demand. International brands are increasingly localizing pricing, product design, and marketing strategies to improve accessibility in these high-growth markets. Expanding gym infrastructure, sports participation programs, and digital retail penetration are further supporting long-term growth potential across emerging economies.

Growth of Digital Fitness Ecosystems

The rapid expansion of digital fitness platforms, connected wellness applications, and virtual workout ecosystems is creating new opportunities for fitness apparel brands. Consumers increasingly seek apparel compatible with wearable technologies and home fitness environments. Brands integrating smart fabrics, biometric monitoring capabilities, and AI-powered personalization into activewear collections can capture higher-value consumers and improve brand differentiation. Collaborations between fitness apparel companies and digital fitness platforms are also becoming increasingly common, enabling companies to create integrated wellness ecosystems and strengthen customer engagement.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 356.4 Billion |

| Market Size in 2026 | USD 388.83 Billion |

| Market Size in 2031 | USD 601.02 Billion |

| CAGR | 9.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Top wear dominates the fitness clothing market, accounting for nearly 36% of global revenue in 2025. Categories such as T-shirts, tank tops, sports bras, hoodies, and compression tops remain highly popular due to their versatility across gym workouts, yoga, running, and casual athleisure use. Bottom wear, including leggings, joggers, shorts, and compression tights, represents another major segment supported by rising participation in fitness activities among women and younger consumers. Specialized apparel categories such as yoga wear, cycling apparel, and CrossFit clothing are witnessing rapid growth due to increasing participation in niche fitness activities. Performance-oriented outerwear, including lightweight jackets and waterproof sportswear, is also gaining traction in outdoor and adventure fitness applications.

Application Insights

Gym and training activities remain the largest application segment within the global fitness clothing market due to rising gym memberships and expanding wellness culture worldwide. Running and athletics apparel continues to witness strong demand supported by marathon participation, recreational sports, and outdoor fitness trends. Yoga and Pilates apparel are among the fastest-growing categories, particularly among women consumers seeking comfort-focused and stretchable activewear products. Athleisure applications are increasingly driving mainstream activewear adoption, with consumers purchasing fitness clothing for daily lifestyle use rather than exclusively athletic purposes. Emerging applications such as home fitness apparel and digitally integrated workout clothing are also gaining popularity due to the expansion of virtual fitness ecosystems.

Distribution Channel Insights

Offline retail channels continue to dominate the fitness clothing market, accounting for nearly 61% of global sales in 2025. Brand-exclusive stores, sporting goods retailers, department stores, and hypermarkets remain important channels due to consumer preference for physical product trials and immediate purchases. However, online retail is witnessing significantly faster growth driven by convenience, wider product availability, and personalized shopping experiences. Direct-to-consumer websites, digital marketplaces, and social commerce platforms are increasingly becoming critical revenue channels for global activewear brands. Companies are investing heavily in AI-powered recommendations, virtual fitting technologies, and influencer-led marketing campaigns to strengthen digital customer engagement and improve conversion rates.

End User Insights

Women represent the leading end-user segment within the global fitness clothing market, accounting for approximately 44% of total market demand in 2025. Rising female participation in yoga, Pilates, gym workouts, and wellness activities has substantially increased demand for leggings, sports bras, seamless activewear, and premium athleisure products. Men’s activewear remains a major category supported by strength training, running, and sports participation trends. The kids and teens segment is also witnessing steady growth as parents increasingly prioritize sports participation and wellness-focused lifestyles for younger demographics. Demand for family-oriented athleisure collections and school sportswear is contributing to broader market expansion.

Material Type Insights

Polyester-based fabrics remain the dominant material category in the fitness clothing market due to their durability, moisture-wicking properties, lightweight structure, and affordability. Nylon-based fabrics are widely used in premium activewear categories because of their flexibility, softness, and abrasion resistance. Spandex and elastane materials continue to experience strong demand due to rising popularity of compression apparel and stretchable activewear. Sustainable materials, including recycled polyester, organic cotton, and biodegradable fibers, are emerging as the fastest-growing material segment as consumers increasingly prioritize environmentally responsible products. Smart and functional textiles featuring odor resistance, UV protection, and thermal regulation capabilities are also becoming important innovation areas within premium fitness apparel categories.

Explore more data points, trends and opportunities Download Free Sample Report

Fitness Clothing Market Segmentations

By Product Type

- Top Wear

- Bottom Wear

- Innerwear & Base Layers

- Outerwear

- Specialized Fitness Apparel

- Accessories Apparel

By End User

- Men

- Women

- Kids & Teens

By Activity Type

- Gym & Training

- Running & Athletics

- Yoga & Pilates

- Cycling

- Outdoor & Adventure Fitness

- Team Sports Training

- Dance & Zumba Fitness

- Athleisure/Casual Fitness Wear

By Material Type

- Polyester-Based Fabrics

- Nylon-Based Fabrics

- Cotton Blends

- Spandex/Elastane-Based Fabrics

- Sustainable/Recycled Materials

- Smart & Functional Textiles

By Distribution Channel

- Offline Retail

- Online Retail

Regional Insights

North America

North America remains the largest regional market for fitness clothing, accounting for approximately 34% of the global market share in 2025. The United States dominates regional demand due to high consumer spending on premium activewear, strong gym participation rates, and widespread adoption of athleisure fashion. Canada also represents a significant growth market supported by outdoor fitness culture and increasing preference for sustainable apparel. The region benefits from strong brand presence, advanced retail infrastructure, and high adoption of digital fitness ecosystems. Premiumization trends and growing demand for performance-enhancing apparel continue supporting long-term market expansion across North America.

Europe

Europe represents one of the most mature fitness clothing markets globally, driven by strong demand across Germany, the United Kingdom, France, Italy, and Spain. European consumers increasingly prioritize sustainability, ethical sourcing, and premium-quality activewear products. The region is witnessing rising adoption of recycled fabrics and eco-friendly manufacturing practices, particularly among younger demographics. Athleisure remains highly popular across urban populations, while wellness-oriented lifestyles continue supporting demand for yoga wear, outdoor fitness apparel, and performance sportswear. Western Europe remains the primary revenue contributor, although Eastern European markets are also witnessing growing fitness apparel adoption.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, accounting for approximately 29% of the global market share in 2025. China remains the largest regional market due to rising middle-class spending, expanding sports participation, and the rapid growth of domestic athleisure brands. India is emerging as one of the fastest-growing countries globally, supported by urbanization, digital commerce expansion, and increasing fitness awareness among younger consumers. Japan and South Korea continue driving premium activewear demand, particularly for technologically advanced and fashion-oriented products. Southeast Asian countries, including Indonesia and Vietnam, are also witnessing rapid market growth driven by rising disposable incomes and expanding e-commerce penetration.

Latin America

Latin America is experiencing steady growth in fitness clothing demand, led primarily by Brazil and Mexico. Brazil benefits from a strong sports culture, increasing gym memberships, and the rising popularity of athleisure fashion among urban consumers. Mexico is witnessing expanding activewear adoption due to improving retail accessibility and rising wellness awareness. Regional demand remains concentrated within mid-priced and affordable activewear categories, although premium segments are gradually expanding among higher-income consumers. Digital retail channels are playing an increasingly important role in improving product accessibility across Latin American markets.

Middle East & Africa

The Middle East and Africa region is witnessing rising adoption of fitness culture and wellness-focused lifestyles, particularly across the UAE, Saudi Arabia, and South Africa. Government investments in sports infrastructure, wellness initiatives, and tourism development are supporting demand for fitness apparel across Gulf countries. Premium activewear brands continue expanding aggressively throughout the Middle East due to strong luxury spending and increasing gym participation among younger populations. South Africa remains one of the most important African markets due to its established retail infrastructure and growing participation in fitness and outdoor sports activities.

Key Players in the Fitness Clothing Market

- Nike Inc.

- Adidas AG

- Puma SE

- Under Armour Inc.

- Lululemon Athletica

- ASICS Corporation

- New Balance Athletics Inc.

- Columbia Sportswear Company

- Skechers USA Inc.

- Anta Sports Products Limited

- Li Ning Company Limited

- VF Corporation

- Gap Inc.

- Gymshark

- Decathlon