Fishing Waders Market Size

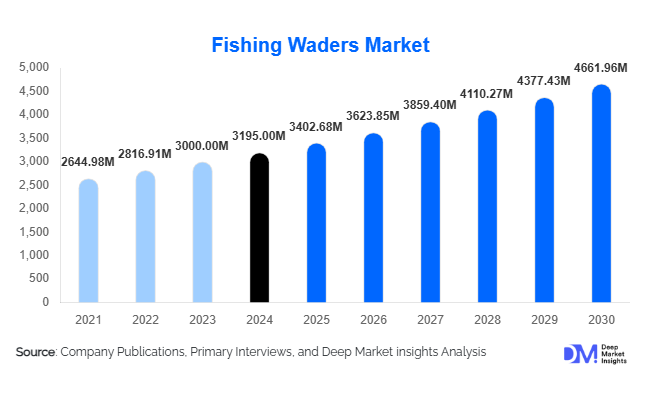

According to Deep Market Insights, the global fishing waders market size was valued at USD 3,195 million in 2025 and is projected to grow from USD 3,402.68 million in 2026 to reach USD 4,661.96 million by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The growth of the fishing waders market is primarily driven by the rising popularity of recreational and sport fishing, the expansion of aquaculture and commercial fisheries, and the integration of technologically advanced and eco-friendly materials in wader designs.

Key Market Insights

- Recreational fishing is the largest driver, with hobbyists and fly-fishing enthusiasts accounting for the majority of demand in North America and Europe.

- Commercial and institutional use in aquaculture, fisheries, and environmental surveying is rising, providing steady, year-round demand for durable and specialized waders.

- Neoprene and breathable synthetic waders dominate, combining waterproofing, insulation, and comfort to meet diverse environmental and climatic requirements.

- Offline retail remains the largest distribution channel, though online sales are rapidly increasing, particularly in emerging regions like the Asia-Pacific.

- Emerging markets in APAC and Latin America offer high growth potential due to rising disposable incomes and expanding outdoor recreation culture.

- Technological innovations and sustainable material adoption are enhancing product performance and attracting environmentally conscious consumers.

Latest Market Trends

Growth of Sustainable and Eco-Friendly Waders

Manufacturers are increasingly focusing on eco-friendly materials, including recycled neoprene, biodegradable composites, and low-impact synthetics. These products appeal to environmentally conscious consumers, particularly in Europe and North America, and align with broader sustainability initiatives in outdoor gear. Wader designs now prioritise lightweight construction, breathability, and ergonomic fit without compromising waterproofing, meeting the demands of both casual and professional anglers.

Technological Integration in Product Design

Advancements in material technology and smart features are transforming fishing waders. Innovations such as moisture-wicking fabrics, thermal insulation, modular designs for multi-season use, and integrated water-safety features are gaining traction. Premium brands are experimenting with sensor integration for temperature and water-level monitoring, improving both comfort and utility for recreational and commercial users alike. Digital platforms are also facilitating online fitting tools, product customisation, and direct-to-consumer sales.

Fishing Waders Market Drivers

Rising Recreational Fishing Participation

The increasing popularity of recreational fishing and outdoor adventure activities is a key growth driver. Higher disposable incomes, growing eco-tourism, and expanding interest in fly fishing are boosting demand for waders. Modern retail channels and e-commerce have further enhanced accessibility, enabling new demographics to purchase premium and mid-range products easily.

Growth of Commercial Fisheries and Aquaculture

Commercial use of fishing waders is rising in aquaculture, commercial fishing, and environmental survey applications. Expanding aquaculture operations globally and increased government support for sustainable fisheries are creating consistent demand for industrial-grade waders. This trend reduces reliance on seasonal recreational purchases and strengthens market stability.

Advancements in Material Technology

Innovations in neoprene, breathable synthetics, and lightweight waterproof fabrics are improving comfort, durability, and performance. Enhanced seam-sealing and ergonomic designs support wider adoption in both warm and cold climates, expanding the total addressable market. Premium features such as integrated boots, insulation, and smart sensors are increasingly influencing buying decisions among serious anglers.

Market Restraints

Seasonal and Regional Demand Fluctuations

Fishing is often seasonal and highly region-specific, leading to fluctuations in demand. In warmer climates or off-seasons, wader sales may decline, affecting revenue consistency and inventory management.

High Costs in Emerging Markets

Premium waders can be expensive, limiting penetration in low- and middle-income regions. Additionally, limited local availability and distribution networks hinder widespread adoption, constraining growth in emerging markets despite rising interest in recreational fishing.

Fishing Waders Market Opportunities

Expansion in Emerging Recreational Markets

Rising leisure spending and interest in adventure tourism in regions like Asia-Pacific, Latin America, and Africa present opportunities for market growth. Affordable, region-specific products and stronger distribution networks can attract new consumer bases.

Commercial and Institutional Demand

Growth in aquaculture, fisheries, and water-based environmental surveying is generating demand for industrial-grade waders. Manufacturers can target commercial buyers with durable, specialised products tailored for professional use, providing steady, off-season revenue streams.

Innovative and Sustainable Product Development

Integrating eco-friendly materials and “smart” wader features offers differentiation in competitive markets. Premium buyers increasingly seek sustainable, performance-enhancing products, presenting an opportunity for higher-margin, innovation-focused offerings.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3195 Million |

| Market Size in 2026 | USD 3402.68 Million |

| Market Size in 2031 | USD 4661.96 Million |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Chest waders continue to dominate the global fishing waders market, accounting for approximately 45–50% of the 2025 market. Their full-coverage design, superior waterproofing, and adaptability across diverse fishing conditions make them the preferred choice for both recreational anglers and commercial users in aquaculture and environmental monitoring. The segment’s growth is driven by rising cold-water fishing activities in North America and Europe, as well as increasing demand for high-performance, durable waders among professional fishery workers. Hip and waist waders are gaining traction in warmer climates and tropical regions, especially in the Asia-Pacific and Latin America, due to their lightweight and breathable design that enhances comfort during extended fishing sessions. Boot-foot waders remain popular among casual anglers and hobbyists, offering ease of use and affordability, particularly in regions where occasional fishing is prevalent.

Application Insights

Recreational fishing remains the largest application segment, representing 60–65% of the global market in 2025. The segment is fueled by increasing outdoor leisure activities, growth of fly-fishing and angling communities, and rising disposable incomes in North America and Europe. Commercial fishing, aquaculture, and environmental survey applications are experiencing robust growth, driven by expanding fishery operations, sustainable aquaculture initiatives, and government-supported environmental monitoring programs. Emerging applications, including eco-tourism and water-based occupational activities, are further broadening market reach, providing steady year-round demand and presenting opportunities for innovation in wader design and material technology.

Distribution Channel Insights

Offline retail continues to dominate, accounting for approximately 55–60% of global sales, with specialty outdoor stores, sporting goods chains, and fishing equipment outlets serving as the primary channels. The segment benefits from hands-on product trials and professional guidance for selecting high-performance waders. Online sales are rapidly expanding, particularly in APAC and LATAM, offering greater geographic reach, direct-to-consumer engagement, and customized product recommendations. E-commerce platforms are increasingly influential in driving awareness and adoption, especially among younger anglers and tech-savvy consumers seeking convenience, product variety, and competitive pricing.

End-User Insights

Male anglers constitute the largest demographic in the fishing waders market; however, female and youth participation is rising steadily, supported by the introduction of more inclusive and ergonomically designed waders. Hobbyists and recreational anglers drive peak-season demand, while institutional and commercial buyers in aquaculture, fisheries, and environmental survey applications ensure stable, long-term growth. Export-driven demand is particularly strong, with APAC manufacturing hubs supplying technologically advanced and mid-range waders to North American and European markets. Increasing participation in organized fishing events, competitions, and eco-tourism also contributes to higher overall consumption across demographics.

Explore more data points, trends and opportunities Download Free Sample Report

Fishing Waders Market Segmentations

By Product Type

- Chest Waders

- Hip Waders

- Waist Waders

- Boot-Foot Waders

By Application

- Recreational Fishing

- Commercial Fishing

- Aquaculture

- Environmental Survey

- Eco-Tourism & Occupational Tasks

By Distribution Channel

- Offline Retail (Specialty Outdoor Stores, Sporting Goods)

- Online Retail / E-Commerce

- Direct-to-Consumer / Brand Stores

By End-User

- Male Anglers

- Female Anglers

- Youth / Young Anglers

- Institutional / Commercial Buyers

Regional Insights

North America

North America holds 35–40% of the 2025 global market, led by the U.S. and Canada. The region’s growth is driven by a strong recreational fishing culture, widespread fly-fishing communities, high disposable incomes, and well-established outdoor sports infrastructure. Chest waders dominate due to cold-water fishing in northern states and Canada, while premium and technologically advanced waders, including breathable and insulated designs, are increasingly popular. Conservation-oriented products and eco-certified waders are driving demand among environmentally conscious anglers. Government-led initiatives supporting sustainable fisheries, combined with widespread participation in sport and competitive fishing events, further bolster market expansion.

Europe

Europe accounts for 20–25% of the global market, with major contributors including the U.K., Germany, France, and Nordic countries. Chest waders remain the leading product due to extensive cold-water recreational fishing and fly-fishing traditions. Growth is supported by rising eco-tourism, stringent environmental regulations promoting sustainable fishing practices, and a growing preference for high-quality, durable fishing equipment. Eastern Europe is emerging as a high-growth sub-region, driven by increased disposable incomes, expanding outdoor leisure activities, and improved distribution channels. Premium and mid-range waders are witnessing rising adoption, reflecting a growing willingness among European consumers to invest in performance-enhancing and environmentally friendly fishing gear.

Asia-Pacific

APAC is the fastest-growing region in the global fishing waders market, driven by rising aquaculture operations, growing recreational fishing interest, and expanding middle-class incomes in China, Japan, South Korea, and Southeast Asia. Hip and waist waders are gaining popularity due to the region’s warmer climates and preference for lightweight, breathable designs. Demand is also fueled by export-oriented production from APAC countries, serving North American and European consumers. Government support for aquaculture, infrastructure development in inland fisheries, and increasing participation in recreational angling clubs are key growth drivers. Additionally, digital retail penetration is enhancing accessibility and adoption of mid-range and premium waders across emerging markets.

Latin America

LATAM accounts for 5–10% of the market in 2025, with Brazil, Argentina, and Mexico as key contributors. The region’s growth is supported by traditional fishing cultures, increasing leisure fishing among affluent consumers, and rising tourism-linked fishing activities. Hip and waist waders are commonly used due to warmer climates, while mid-range and casual boot-foot designs dominate recreational segments. Government-led initiatives promoting sustainable fishing practices and growth in sport-fishing tourism are further supporting market expansion. Urbanization and increasing disposable income levels among younger consumers are also driving higher adoption of recreational fishing gear.

Middle East & Africa

MEA represents 3–7% of the market, with Africa serving as both a production hub and a growing recreational market. Countries such as South Africa, Nigeria, the UAE, Saudi Arabia, and Qatar are emerging as high-potential markets for premium and mid-range waders. Growth is supported by tourism-linked fishing activities, professional aquaculture operations, and government initiatives promoting sustainable fisheries. Chest and hip waders are preferred depending on climate conditions, while technological innovations and durability in harsh environments are key decision factors. Rising outdoor sports participation and investments in fishery infrastructure are further contributing to regional market growth.

Key Players in the Fishing Waders Market

- Simms Fishing Products

- The Orvis Company

- Patagonia

- Columbia Sportswear Company

- Cabela’s

- Redington

- Gator Waders

- Caddis Waders

- Pure Fishing

- Hodgman

- Fishpond

- Pacific Eagle Enterprise

- Complete Angler

- Drake Waterfowl

- Waders (Independent Specialist Brands)