Fire Doors Market Size

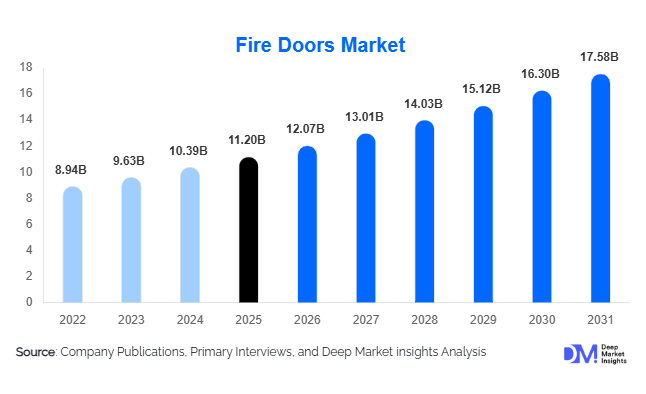

According to Deep Market Insights, the global fire doors market size was valued at USD 11.2 billion in 2025 and is projected to grow from USD 12.07 billion in 2026 to reach USD 17.58 billion by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The fire doors market growth is primarily driven by stringent fire safety regulations, rising construction activities across residential and commercial sectors, and increasing awareness regarding passive fire protection systems globally.

Key Market Insights

- Fire safety regulations are becoming increasingly stringent globally, mandating the installation of certified fire doors in both new and existing buildings.

- Commercial infrastructure dominates demand, particularly in offices, malls, hospitals, and hotels requiring high compliance standards.

- Europe leads the global market, supported by strict regulatory frameworks and high retrofit demand.

- Asia-Pacific is the fastest-growing region, driven by rapid urbanization and infrastructure expansion in China and India.

- Steel fire doors are the most widely used material, due to durability, strength, and high fire resistance.

- Technological advancements, including smart fire doors integrated with automation and IoT systems, are transforming product offerings.

What are the latest trends in the fire doors market?

Smart and Automated Fire Doors Adoption

The adoption of smart fire doors is increasing as buildings become more integrated with digital infrastructure. These doors are equipped with sensors, automatic closing mechanisms, and connectivity to centralized fire alarm systems. In case of fire detection, doors automatically close to prevent the spread of flames and smoke. This trend is particularly strong in commercial buildings, hospitals, and smart city projects. Integration with IoT platforms allows real-time monitoring and predictive maintenance, improving operational efficiency and safety compliance.

Growing Demand for Aesthetic and Customized Fire Doors

Modern construction trends emphasize both safety and design, leading to increased demand for aesthetically appealing fire doors. Manufacturers are offering customizable designs, finishes, and materials such as glass and composite structures that blend with interior architecture. This trend is especially prominent in premium residential and commercial spaces where safety cannot compromise design. Fire-rated glass doors and wooden finishes are gaining traction in offices and hospitality sectors.

What are the key drivers in the fire doors market?

Stringent Fire Safety Regulations

Governments and regulatory bodies across regions have implemented strict fire safety codes, making fire doors mandatory in various building types. Standards such as EN, NFPA, and local building codes ensure compliance, driving consistent demand. Regular inspections and penalties for non-compliance further reinforce adoption.

Rapid Growth in Construction and Infrastructure

Urbanization and industrialization are fueling construction activities globally. High-rise buildings, commercial complexes, and industrial facilities require compartmentalized fire safety systems, including fire doors. Emerging economies are witnessing massive infrastructure investments, significantly contributing to market growth.

Increasing Awareness of Fire Safety

Rising awareness due to fire incidents has encouraged building owners and developers to invest in advanced safety systems. Insurance companies also promote compliance with fire safety measures, indirectly supporting demand for fire doors.

What are the restraints for the global market?

High Installation and Maintenance Costs

Fire doors, particularly certified and high-performance variants, involve higher costs compared to conventional doors. This cost factor limits adoption in price-sensitive markets and small-scale residential applications.

Lack of Awareness and Improper Installation

In developing regions, lack of awareness and improper installation practices reduce the effectiveness of fire doors. Weak enforcement of regulations and use of non-compliant products also act as barriers to market growth.

What are the key opportunities in the fire doors industry?

Retrofit and Renovation Projects

A significant number of older buildings require upgrades to meet modern fire safety standards. Retrofitting fire doors presents a strong opportunity, especially in developed regions where regulatory compliance is strictly enforced.

Expansion in Emerging Markets

Rapid urbanization in Asia-Pacific, the Middle East, and Latin America is creating substantial demand for fire safety solutions. Government initiatives and infrastructure projects are driving adoption in these regions.

Eco-Friendly and Sustainable Fire Doors

The rising focus on sustainability is driving demand for fire doors made from recyclable materials and eco-friendly components. Green building certifications are encouraging manufacturers to develop energy-efficient and sustainable products.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.2 Billion |

| Market Size in 2026 | USD 12.07 Billion |

| Market Size in 2031 | USD 17.58 Billion |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Material Insights

Steel fire doors dominate the global market, accounting for approximately 38% of total demand in 2025, primarily driven by their superior strength, durability, and high fire resistance capabilities. These doors are extensively used in commercial and industrial environments where stringent fire safety compliance is required. The ability of steel doors to withstand extreme temperatures and provide longer fire ratings makes them the preferred choice in high-risk applications. Timber fire doors continue to witness strong demand in residential and hospitality sectors due to their aesthetic appeal and ability to blend with interior designs. The growing trend of combining safety with visual appeal is driving their adoption in premium residential projects. Glass fire doors are gaining traction in commercial spaces such as offices, malls, and airports, where transparency and modern architectural design are critical, supported by advancements in fire-resistant glazing technologies.

Composite fire doors are emerging as a high-growth segment, offering a balance between performance, insulation, and flexibility in design. These doors are increasingly adopted in modern infrastructure projects. Aluminum fire doors, although niche, are preferred in applications requiring lightweight structures and corrosion resistance, particularly in coastal and industrial environments.

Fire Rating Insights

Fire doors rated between 60–120 minutes account for approximately 34% of the global market, making them the leading segment. This dominance is driven by their optimal balance between cost, safety, and regulatory compliance, making them suitable for commercial buildings, high-rise apartments, and institutional facilities. Lower-rated fire doors (up to 30 minutes) are primarily used in residential buildings, where basic compartmentalization is sufficient. On the other hand, fire doors rated above 120 minutes are increasingly deployed in high-risk environments such as industrial plants, data centers, and chemical facilities. The demand for higher-rated doors is growing due to increasing awareness of risk mitigation and stricter industrial safety standards.

Mechanism Insights

Hinged fire doors dominate the mechanism segment with a share of approximately 45%, driven by their cost-effectiveness, ease of installation, and compatibility with a wide range of building structures. Their simplicity and reliability make them the most widely adopted solution across residential, commercial, and institutional applications.

Sliding and rolling shutter fire doors are primarily used in industrial and warehouse settings, where large openings require efficient fire containment solutions. The growth of logistics and e-commerce sectors is further driving demand for these variants. Automatic fire doors are gaining momentum in smart buildings and high-end commercial spaces, supported by the integration of sensors, alarm systems, and building automation technologies, which enhance safety and operational efficiency.

Application Insights

Internal fire doors account for nearly 62% of the market share, driven by their critical role in compartmentalizing buildings and preventing the spread of fire and smoke between sections. Increasing regulatory emphasis on internal safety measures in high-rise buildings and commercial complexes is a key driver for this segment.

External fire doors are primarily used in exit routes, industrial facilities, and perimeter safety applications. Their demand is supported by regulations mandating safe evacuation routes and fire containment at building exteriors, particularly in industrial and hazardous environments.

End-Use Insights

Commercial buildings lead the fire doors market with approximately 36% share, driven by strict fire safety regulations, high occupancy risks, and mandatory compliance standards. Offices, shopping malls, hotels, and healthcare facilities are the primary contributors to this segment.

The residential sector is the fastest-growing segment, supported by rapid urbanization, increasing construction of high-rise apartments, and rising consumer awareness regarding fire safety. Industrial facilities, including manufacturing plants and warehouses, contribute significantly due to the need for asset protection and risk mitigation. Institutional buildings such as hospitals, schools, and government facilities also drive steady demand due to strict compliance requirements and safety protocols.

Distribution Channel Insights

Direct sales dominate the market, accounting for approximately 55% of total share, as fire doors are typically procured through contractors, builders, and large-scale infrastructure projects. This channel ensures customization, compliance, and bulk procurement for construction activities.

Distributors and dealers play a crucial role in regional market penetration, particularly in small and mid-scale projects. Meanwhile, online channels are gradually emerging, especially for standardized fire door products, driven by digitalization and the growing adoption of e-commerce platforms in the construction materials industry.

Explore more data points, trends and opportunities Download Free Sample Report

Fire Doors Market Segmentations

By Material

- Steel Fire Doors

- Timber/Wood Fire Doors

- Glass Fire Doors

- Composite Fire Doors

- Aluminum Fire Doors

By Mechanism

- Hinged Fire Doors

- Sliding Fire Doors

- Rolling Shutter Fire Doors

- Automatic Fire Doors

- Manual Fire Doors

By Application

- Internal Fire Doors

- External Fire Doors

By End-Use Industry

- Residential Buildings

- Commercial Buildings

- Industrial Facilities

- Institutional Buildings

By Distribution Channel

- Direct Sales

- Distributors & Dealers

- Online Channels

Regional Insights

Europe

Europe holds the largest share of the global fire doors market at approximately 32% in 2025. This dominance is primarily driven by stringent fire safety regulations, such as EN standards, and strong enforcement mechanisms across countries like the UK, Germany, and France. A major growth driver in this region is the high demand for retrofitting older buildings to comply with modern fire safety codes. Additionally, increased awareness following past fire incidents and strong government mandates for public safety infrastructure continue to drive market expansion.

Asia-Pacific

Asia-Pacific accounts for around 30% of the market and is the fastest-growing region, with a projected CAGR exceeding 9%. China and India are the key contributors, driven by rapid urbanization, large-scale infrastructure development, and government initiatives such as smart city projects. Increasing construction of residential high-rises and commercial complexes, coupled with improving regulatory frameworks, is a major growth driver. Rising awareness of fire safety and increasing foreign investments in infrastructure further accelerate demand in this region.

North America

North America holds approximately 25% market share, with the United States being the largest contributor. Growth in this region is driven by strict building codes such as NFPA standards, high awareness of fire safety, and consistent investment in commercial infrastructure. Additionally, the presence of advanced construction technologies and early adoption of smart fire door systems are key drivers supporting market growth.

Middle East & Africa

The Middle East & Africa region is experiencing strong growth, driven by large-scale infrastructure projects and urban development in countries such as the UAE and Saudi Arabia. Mega projects, including smart cities and commercial hubs, are key demand drivers. Increasing adoption of international safety standards and government investments in public infrastructure are further supporting market expansion. In Africa, gradual improvements in regulatory frameworks and urbanization are contributing to steady growth.

Latin America

Latin America is an emerging market for fire doors, with Brazil and Mexico leading demand. The region’s growth is driven by increasing urbanization, expansion of commercial infrastructure, and gradual implementation of fire safety regulations. Rising investments in construction and improving awareness regarding fire safety standards are key factors contributing to market growth. Although the market share is relatively smaller, the region presents strong long-term growth potential.

Key Players in the Fire Doors Market

- ASSA ABLOY

- Allegion plc

- dormakaba Group

- Hörmann Group

- JELD-WEN Holding Inc.

- Masonite International Corporation

- Sanwa Holdings Corporation

- Novoferm Group

- Ninz S.p.A.

- Teckentrup GmbH

- Vista Panels

- Latham’s Steel Doors

- Pyropanel Developments

- Schüco International KG

- Tata Metaliks