Fine Art Advisory Market Size

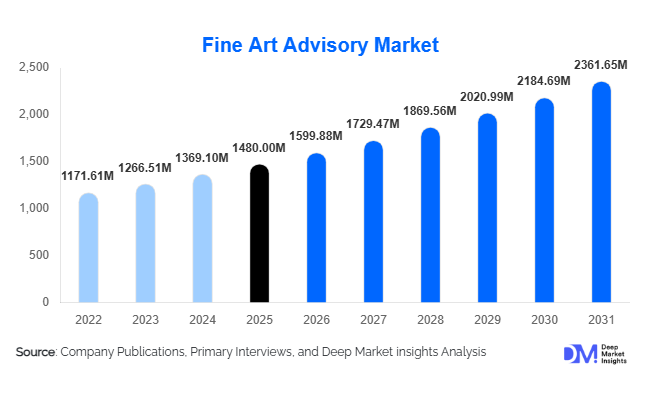

According to Deep Market Insights, the global fine art advisory market size was valued at USD 1,480 million in 2025 and is projected to grow from USD 1,599.88 million in 2026 to reach USD 2,361.65 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The fine art advisory market growth is primarily driven by the increasing financialization of art as an alternative asset class, rising participation of ultra-high-net-worth individuals (UHNWIs), and growing demand for professional expertise in art acquisition, valuation, and portfolio management.

Key Market Insights

- Fine art is increasingly being integrated into wealth management portfolios, with investors allocating 5–10% of assets to art for diversification and inflation hedging.

- Independent boutique advisors dominate advisory services, offering unbiased, conflict-free guidance compared to auction house-led advisory models.

- North America leads the global market, driven by strong auction ecosystems and a high concentration of UHNWIs.

- Asia-Pacific is the fastest-growing region, fueled by rapid wealth creation in China and India and expanding collector bases.

- Digital transformation and blockchain adoption are improving provenance tracking, transparency, and valuation accuracy.

- Contemporary art remains the most actively traded segment, accounting for the largest share of advisory services globally.

What are the latest trends in the fine art advisory market?

Data-Driven Art Investment Strategies

Fine art advisory is increasingly transitioning toward data-driven decision-making. Advisors are leveraging advanced analytics, art price indices, and AI-powered forecasting tools to guide clients on acquisition and portfolio optimization. This shift enhances transparency in a traditionally opaque market and enables more structured investment approaches. Data-backed advisory services are particularly appealing to institutional investors and younger collectors who demand measurable returns and risk assessments. Additionally, proprietary databases and transaction benchmarking tools are being integrated into advisory workflows, improving accuracy in pricing and valuation recommendations.

Expansion of Digital Art and Blockchain Authentication

The emergence of digital art, including NFTs, has significantly expanded the scope of fine art advisory services. Advisors are now assisting clients in navigating digital asset valuation, ownership verification, and portfolio diversification into new media. Blockchain-based provenance systems are gaining traction, reducing fraud risks and enhancing trust in art transactions. These innovations are also enabling fractional ownership models, broadening access to high-value artworks. As digital-native collectors enter the market, advisory firms are adapting their service offerings to include hybrid physical-digital art strategies and cross-platform asset management.

What are the key drivers in the fine art advisory market?

Rising Wealth Concentration and UHNWI Growth

The global increase in ultra-high-net-worth individuals is a major driver of the fine art advisory market. These clients seek specialized services for acquiring, managing, and monetizing art collections. As wealth becomes more concentrated, demand for personalized advisory solutions, including tax planning and estate structuring, continues to grow. Family offices are also expanding their art portfolios, further strengthening demand for professional advisory services.

Art as a Recognized Alternative Investment

Art is increasingly viewed as a viable alternative asset class, offering diversification benefits and resilience against economic volatility. Investors are turning to art for long-term capital appreciation and portfolio stability. This trend is driving demand for advisors who can provide insights into market trends, artist performance, and asset liquidity. The growing presence of art funds and art-backed financial instruments is further institutionalizing the market.

What are the restraints for the global market?

Limited Market Transparency

The fine art market remains relatively opaque, with limited publicly available pricing data and inconsistent valuation standards. This lack of transparency can create challenges for advisors in accurately assessing asset value and risk, particularly for emerging artists or private sales. It also limits scalability for new entrants who lack access to established networks and proprietary data.

High Dependence on Relationships and Trust

Fine art advisory is heavily relationship-driven, requiring long-standing trust between advisors, collectors, and institutions. Building credibility in the market takes time, posing a barrier for new firms. Additionally, conflicts of interest can arise in commission-based models, affecting client trust and decision-making processes.

What are the key opportunities in the fine art advisory industry?

Integration with Wealth Management Services

The convergence of fine art advisory with private banking and wealth management presents a major growth opportunity. Financial institutions are increasingly incorporating art advisory into their service portfolios, offering clients holistic asset management solutions. This integration allows advisors to access a broader client base and provide structured investment strategies, including art-backed lending and portfolio diversification.

Emerging Market Expansion

Asia-Pacific and the Middle East are emerging as high-growth regions for fine art advisory. Rising affluence, government-backed cultural initiatives, and expanding art ecosystems are driving demand for advisory services. Countries such as China, India, and the UAE are witnessing increased participation in global art markets, creating opportunities for advisors to establish regional expertise and capture untapped demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1480 Million |

| Market Size in 2026 | USD 1599.88 Million |

| Market Size in 2031 | USD 2361.65 Million |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Service Type Insights

Acquisition advisory continues to dominate the fine art advisory market, accounting for approximately 28% of total revenue in 2025. This leadership is primarily driven by the increasing volume of high-value transactions across both primary (gallery-led) and secondary (auction and private sale) markets. The globalization of art trade, rising cross-border purchases, and growing participation of institutional buyers have significantly increased the need for expert guidance in sourcing, pricing, and negotiation. Additionally, the complexity of provenance verification and authenticity checks further strengthens reliance on acquisition advisors, making this segment indispensable.

Valuation and appraisal services remain a critical component of the market, particularly due to rising demand for insurance coverage, estate planning, and collateralization of art assets. Collection management services are witnessing accelerated growth with the adoption of digital cataloguing, blockchain-backed inventory systems, and condition monitoring technologies, enabling efficient asset tracking for large collections. Art investment advisory is also expanding rapidly, driven by the increasing perception of art as a financial asset class, while estate and legacy planning services are gaining traction due to intergenerational wealth transfer and tax optimization requirements.

Client Type Insights

Ultra-high-net-worth individuals (UHNWIs) represent the largest client segment, contributing approximately 42% of total market demand. Their dominance is driven by substantial purchasing power, growing interest in alternative investments, and the desire to build culturally significant collections. UHNWIs increasingly rely on advisory services for portfolio diversification, risk management, and legacy planning, making them the primary revenue drivers for advisory firms.

Family offices are the fastest-growing segment, expanding at a notable pace as they adopt structured investment strategies and long-term wealth preservation approaches. The integration of art into multi-asset portfolios and the rise of art-backed lending are further accelerating demand from this segment. Corporate collections are also expanding steadily, particularly in sectors such as finance, hospitality, and technology, where art is used for brand positioning, employee engagement, and experiential environments. Museums and institutions continue to represent a stable demand base, supported by government funding, philanthropy, and cultural initiatives.

Art Category Insights

Contemporary art leads the market with an estimated 35% share, driven by its strong global appeal, higher liquidity, and consistent performance in auction markets. The segment benefits from increasing demand among younger collectors and investors who prefer emerging and mid-career artists with high growth potential. Additionally, the dynamic nature of contemporary art aligns well with evolving cultural trends, making it a preferred choice for both private collectors and institutions.

Modern art and Impressionist works continue to command high-value transactions, particularly among established collectors seeking stability and prestige. Digital art, including NFTs, is emerging as a rapidly growing category, supported by blockchain technology and increasing adoption among tech-savvy investors. Decorative arts and photography are gaining traction as accessible entry points for new collectors, contributing to market diversification and broader participation.

Advisory Model Insights

Independent boutique advisory firms dominate the market, accounting for approximately 38% share, primarily due to their perceived objectivity and client-centric approach. Clients increasingly prefer independent advisors to avoid conflicts of interest associated with auction houses or galleries, especially in high-value transactions. The personalized nature of services offered by boutique firms further strengthens their market position.

Auction house advisory divisions leverage extensive transaction data, global networks, and direct market access, enabling them to provide competitive insights and execution capabilities. Meanwhile, wealth management-integrated advisory services are expanding rapidly as private banks incorporate art advisory into their offerings, creating a more holistic asset management ecosystem. Digital advisory platforms are emerging as a disruptive force, offering scalable, data-driven solutions and expanding access to a broader client base, particularly among younger and mid-tier investors.

Revenue Model Insights

Commission-based models dominate the market, accounting for approximately 46% of total revenue, as they align directly with transaction values and incentivize successful deal execution. This model remains prevalent in acquisition and sales advisory services, particularly in high-value transactions.

Fee-based advisory services are gaining popularity due to increasing demand for transparency, independence, and conflict-free advice. Clients, particularly institutional investors and family offices, are shifting toward retainer-based or fixed-fee structures to ensure unbiased recommendations. Hybrid models are also emerging, combining fixed advisory fees with performance-linked incentives, enabling firms to balance revenue predictability with client alignment and long-term engagement.

End-Use Insights

Private collectors and family offices dominate end-use demand, collectively accounting for over 55% of the global market. This dominance is driven by increasing allocation of wealth into art as an alternative investment and the growing importance of structured collection management. The family office segment is expanding at a CAGR of approximately 9%, supported by intergenerational wealth transfer and the integration of art into diversified portfolios.

Corporate demand is rising steadily, particularly in industries such as finance, technology, and hospitality, where art is used to enhance brand identity, corporate image, and workplace environments. Emerging applications such as art-backed lending and fractional ownership are expanding the scope of advisory services, creating new revenue streams. Export-driven demand remains strong in global art hubs such as the United States, the United Kingdom, and Switzerland, which act as key centers for cross-border art transactions, storage, and advisory services.

Explore more data points, trends and opportunities Download Free Sample Report

Fine Art Advisory Market Segmentations

By Service Type

- Acquisition Advisory

- Collection Management

- Art Investment Advisory

- Valuation & Appraisal

- Sales & Deaccession Advisory

- Estate & Legacy Planning

- Art Financing & Lending Advisory

By Client Type

- Ultra-High-Net-Worth Individuals (UHNWIs)

- High-Net-Worth Individuals (HNWIs)

- Family Offices

- Corporations

- Museums & Institutions

- Art Investment Funds

By Art Category

- Modern Art

- Contemporary Art

- Old Masters

- Impressionist & Post-Impressionist

- Decorative Arts

- Digital Art (NFTs)

- Photography

By the Advisory Model

- Independent Boutique Advisors

- Auction House Advisory Divisions

- Wealth Management Integrated Advisory

- Digital Advisory Platforms

By Revenue Model

- Fee-Based

- Commission-Based

- Hybrid Model

Regional Insights

North America

North America accounts for approximately 40% of the global fine art advisory market, with the United States serving as the dominant contributor. The region’s leadership is driven by a highly mature art ecosystem, a strong concentration of UHNWIs, and the presence of major auction houses and galleries. New York remains a global hub for art transactions, facilitating high-value deals and international participation. Key growth drivers include the increasing integration of art into wealth management services, rising demand for art-backed financial products, and strong institutional participation. Canada is witnessing steady growth, supported by expanding private wealth, growing museum investments, and increased adoption of advisory services among collectors.

Europe

Europe holds around 30% of the global market share, led by the United Kingdom, France, and Switzerland. London continues to be a major global art trading center, supported by its strong auction infrastructure and international collector base. Switzerland’s prominence is driven by its advanced art logistics, freeport storage facilities, and favorable tax environment. France is experiencing renewed growth due to increased cultural investments and government initiatives promoting the arts. Regional growth is further supported by strong export activity, cross-border transactions within the EU, and increasing demand for advisory services related to estate planning and art financing.

Asia-Pacific

Asia-Pacific accounts for approximately 20% of the market and is the fastest-growing region, with a CAGR of around 10%. China dominates regional demand, followed by Hong Kong and India, which are emerging as key growth markets. The primary drivers of growth include rapid wealth creation, expanding middle- and high-income populations, and increasing interest in art as an investment asset. Government-backed cultural initiatives, museum expansions, and rising participation in global auctions are further accelerating demand. Additionally, digital adoption and the popularity of online art platforms are enhancing accessibility and driving market expansion across the region.

Latin America

Latin America represents approximately 4% of the global market, with Brazil and Mexico leading demand. Growth in the region is driven by increasing awareness of art as an investment, rising participation of local collectors, and expanding international exposure through global art fairs and auctions. Economic stabilization in key markets and growing private wealth are encouraging the adoption of advisory services. However, the market remains in a nascent stage, with significant potential for expansion as infrastructure and awareness improve.

Middle East & Africa

The Middle East & Africa region accounts for approximately 6% of the market, with the UAE and Saudi Arabia emerging as key growth centers. The region’s growth is driven by substantial government investments in cultural infrastructure, including museums, art districts, and international exhibitions. High-income populations and strong demand for luxury assets are further supporting market expansion. Additionally, initiatives aimed at diversifying economies beyond oil, particularly in the Gulf countries, are promoting the development of art ecosystems. Africa contributes through its role as a source of cultural assets and increasing participation in global art markets, further strengthening regional demand for advisory services.

Key Players in the Fine Art Advisory Market

- Gurr Johns

- The Fine Art Group

- Deloitte Art & Finance

- Citi Private Bank Art Advisory

- Sotheby’s Art Advisory

- Christie’s Art Advisory

- ArtTactic

- Philip Hoffman Advisors

- Beaumont Nathan

- Winston Art Group

- Athena Art Finance

- Artory

- MyArtBroker Advisory

- Larasati Advisory

- Art Advisory Services (AAS)