File Folders Market Size

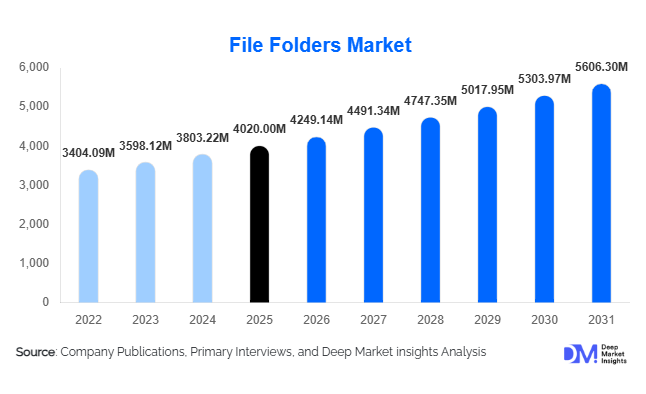

According to Deep Market Insights, the global file folders market size was valued at USD 4,020 million in 2025 and is projected to grow from USD 4,249.14 million in 2026 to reach USD 5,606.30 million by 2031, expanding at a CAGR of 5.7% during the forecast period (2026–2031). The file folders market growth is primarily driven by sustained demand from corporate offices, educational institutions, healthcare administration, and government documentation requirements worldwide. Despite ongoing digitalization, hybrid documentation systems combining physical and digital recordkeeping continue to support stable consumption across developed and emerging economies.

Key Market Insights

- Institutional procurement remains the backbone of market demand, with governments, corporations, and educational institutions accounting for the majority of global purchases.

- Sustainable and recycled paper-based folders are gaining strong adoption, particularly across Europe and North America due to ESG procurement mandates.

- Asia-Pacific dominates global consumption, driven by administrative expansion, SME growth, and rising education infrastructure investments.

- B2B contract sales represent the leading distribution channel, supported by long-term institutional supply agreements.

- Hybrid work models are increasing demand for portable organization solutions, including expanding and multi-divider folders.

- E-commerce penetration is reshaping pricing transparency and accessibility, allowing manufacturers to reach SMEs and home-office users directly.

What are the latest trends in the file folders market?

Sustainability and Recycled Material Adoption

Environmental sustainability has emerged as a defining trend in the file folders market. Organizations are increasingly prioritizing recyclable and FSC-certified paper products to align with corporate ESG commitments and government procurement policies. Manufacturers are transitioning toward recycled fiber materials, biodegradable coatings, and plastic-free packaging solutions. This shift is particularly strong in Europe, where environmental compliance regulations influence purchasing decisions. Eco-friendly folders are commanding premium pricing while strengthening brand differentiation among institutional buyers seeking environmentally responsible office supplies.

Hybrid Work and Modular Organization Solutions

The rise of hybrid workplaces has transformed product innovation within the file folders industry. Employees managing documents across office and home environments require portable, categorized storage solutions. Expanding folders, color-coded systems, and customizable labeling products are gaining popularity. Manufacturers are integrating ergonomic designs and durable materials to improve usability. Digital ordering platforms and subscription-based office supply procurement models are further supporting recurring purchases, enabling companies to maintain organized workflows despite decentralized work environments.

What are the key drivers in the file folders market?

Regulatory Documentation and Compliance Requirements

Industries such as healthcare, legal services, and finance continue to rely heavily on physical documentation for compliance, auditing, and record retention. Regulatory mandates requiring secure physical storage sustain recurring procurement cycles. Hospitals and legal institutions, in particular, maintain long-term archival systems that ensure steady demand even amid digital transformation initiatives.

Expansion of Education and Public Administration Infrastructure

Global investments in education systems and government administration are driving consistent consumption of filing products. Developing economies are expanding public offices, schools, and administrative institutions, all of which depend on organized document storage solutions. Increasing student enrollments and administrative paperwork continue to support high-volume purchases globally.

What are the restraints for the global market?

Shift Toward Digital Documentation

The adoption of cloud storage, electronic signatures, and enterprise document management systems is gradually reducing per-office paper consumption in developed markets. Organizations transitioning toward paperless workflows may reduce purchase frequency over time, creating long-term demand pressure.

Raw Material Price Volatility

Fluctuations in pulp and polymer prices directly impact manufacturing costs. Since file folders remain a price-sensitive commodity product, manufacturers often face margin compression when raw material costs rise, limiting pricing flexibility and profitability expansion.

What are the key opportunities in the file folders industry?

Eco-Friendly Product Innovation

Growing environmental awareness presents a major opportunity for manufacturers investing in recycled and biodegradable materials. Eco-certified folders are increasingly preferred by multinational corporations and government agencies, enabling suppliers to secure long-term contracts and premium pricing advantages. Sustainable manufacturing also improves brand positioning and export competitiveness.

Emerging Economy Institutional Expansion

Rapid administrative growth across Asia-Pacific and Africa is generating strong demand for basic office supplies. Government modernization programs and SME formation are increasing procurement volumes. Localized manufacturing and regional distribution networks offer new entrants opportunities to compete effectively by reducing logistics costs.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4020 Million |

| Market Size in 2026 | USD 4249.14 Million |

| Market Size in 2031 | USD 5606.30 Million |

| CAGR | 5.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global file folders market demonstrates strong diversification across product types, with standard file folders maintaining a dominant position and accounting for nearly 38% of total demand. Their leadership is primarily supported by cost efficiency, ease of mass production, and universal compatibility with traditional filing systems used across corporate offices, educational institutions, and government departments. Organizations continue to rely on standard folders for everyday document storage due to their simplicity and scalability in high-volume administrative environments. The leading segment growth is further driven by continuous demand from emerging economies where physical documentation remains essential for regulatory compliance and operational workflows.

Expanding file folders are experiencing accelerated adoption as businesses manage increasingly complex documentation structures. The rise of hybrid work environments and mobile administrative operations has created demand for portable yet organized storage solutions capable of accommodating higher document volumes without compromising accessibility. Hanging folders continue to maintain strong relevance within structured corporate filing infrastructures, particularly in mature markets where legacy cabinet-based systems remain operational. Classification and fastener folders are gaining increased traction within legal, healthcare, and financial sectors, where secure document segmentation and audit-ready organization are critical requirements. Meanwhile, specialty folders, including waterproof, fire-resistant, and archival-grade variants, are emerging as a niche but high-value category supported by compliance-driven industries such as healthcare records management, legal archiving, and government preservation initiatives.

Material Type Insights

Material selection plays a critical role in shaping purchasing decisions across the file folders market. Paperboard and cardstock folders lead the segment with approximately 62% market share, largely driven by sustainability initiatives, recyclability advantages, and lower production costs compared to plastic alternatives. Organizations increasingly prioritize environmentally responsible procurement practices, encouraging manufacturers to develop recycled and FSC-certified paper-based solutions. The leading segment growth is supported by corporate ESG commitments and government green procurement policies that favor biodegradable materials without compromising functionality.

Polypropylene and other plastic-based folders maintain steady demand due to superior durability, moisture resistance, and longer product lifecycles, particularly in healthcare facilities, educational institutions, and industrial workplaces where frequent handling is common. Hybrid material folders are gaining momentum as manufacturers combine reinforced edges, coated surfaces, and paper-based cores to extend usability while maintaining environmental compliance. These innovations address the growing need for sustainable yet long-lasting office supplies, enabling organizations to balance cost optimization with sustainability targets.

Distribution Channel Insights

Distribution dynamics within the file folders market continue to evolve as procurement models shift toward efficiency and digitalization. B2B contract sales represent the leading distribution channel, accounting for nearly 36% of global revenue. Large enterprises, educational networks, and government agencies increasingly rely on long-term supplier agreements to ensure consistent product availability, standardized specifications, and cost predictability. The leading segment growth is driven by centralized procurement strategies and institutional bulk purchasing practices that reduce administrative complexity.

Office supply retail stores remain important for small and medium-sized enterprises as well as independent professionals requiring flexible purchasing quantities. However, online platforms are emerging as the fastest-growing channel, supported by price transparency, simplified comparison tools, subscription-based restocking models, and improved logistics networks. Institutional procurement portals and direct manufacturer partnerships are gradually replacing traditional wholesale intermediaries, enabling manufacturers to strengthen margins while offering customized product solutions tailored to enterprise requirements.

End-Use Insights

Corporate and commercial offices constitute the largest end-use segment, contributing approximately 31% of total market share. Continuous administrative documentation, internal reporting, and compliance recordkeeping sustain steady consumption levels across enterprises of all sizes. The leading segment growth is primarily driven by ongoing business expansion in developing economies and persistent reliance on physical documentation alongside digital systems, particularly for legal validation and archival purposes.

Healthcare and legal industries represent the fastest-growing end-use categories, expanding at annual rates exceeding 6% as regulatory compliance standards intensify globally. Patient record management, legal case documentation, and audit trails require structured physical storage despite increasing digital transformation. Educational institutions continue to provide stable baseline demand supported by expanding student populations and administrative requirements worldwide. Household and home-office usage has also grown steadily following the normalization of remote and hybrid work models, encouraging individuals to maintain organized physical documentation systems. Additionally, export-oriented industries contribute to demand through logistics documentation, customs paperwork, and regulatory filing processes essential for international trade operations.

Explore more data points, trends and opportunities Download Free Sample Report

File Folders Market Segmentations

By Product Type

- Standard File Folders

- Expanding File Folders

- Hanging File Folders

- Classification & Divider Folders

- Presentation & Report Folders

- Specialty File Folders

By Material Type

- Paperboard & Cardstock

- Polypropylene (PP) Plastic

- PVC & Vinyl

- Recycled Paper Materials

- Hybrid Reinforced Materials

By Distribution Channel

- Office Supply Retail Stores

- Hypermarkets & Supermarkets

- Online & E-commerce Platforms

- B2B Contract Sales

- Institutional Procurement

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global file folders market, accounting for approximately 39% of total share in 2025. The region’s leadership is driven by rapid economic expansion, rising SME formation, and large-scale administrative activities across countries such as China, India, Indonesia, and Southeast Asian economies. Strong population growth and expanding education systems generate consistent institutional demand for filing products. Regional growth is further supported by increasing government digitization programs that paradoxically sustain physical documentation needs for verification and archival purposes. In India, growing investments in education infrastructure, public administration expansion, and formalization of business operations are accelerating demand. Manufacturing cost advantages and strong local production ecosystems also enable competitive pricing, reinforcing regional consumption growth.

North America

North America accounts for nearly 24% of global demand, led primarily by the United States and supported by well-established corporate procurement ecosystems. The region benefits from structured office management practices and extensive documentation requirements across healthcare, legal, and financial sectors. Regional growth is driven by replacement demand, product premiumization, and increasing adoption of sustainable office supplies aligned with corporate environmental commitments. High healthcare documentation volumes, regulatory compliance standards, and institutional purchasing contracts continue to sustain long-term consumption stability. Additionally, hybrid workplace models have supported incremental demand from home-office users.

Europe

Europe represents approximately 22% of the global market, with Germany, the United Kingdom, and France serving as primary consumption hubs. Regional growth is strongly influenced by stringent environmental regulations and circular economy initiatives encouraging recyclable and eco-certified office products. Government-led green procurement programs are accelerating innovation in sustainable materials and low-carbon manufacturing processes. Demand is also supported by stable public-sector administration and well-established educational institutions that maintain consistent procurement cycles. Increasing emphasis on product durability and lifecycle efficiency further shapes purchasing decisions across European organizations.

Latin America

Latin America demonstrates steady market expansion, with Brazil and Mexico leading regional demand due to growing service industries and administrative modernization initiatives. Expansion of financial services, education systems, and public-sector recordkeeping contributes to sustained consumption. Regional growth drivers include improving business formalization, rising SME activity, and gradual adoption of standardized documentation processes across enterprises. Investments in education access and institutional infrastructure modernization are expected to support long-term market development despite economic fluctuations.

Middle East & Africa

The Middle East & Africa region presents emerging growth opportunities supported by government modernization programs and expanding educational investments. Countries such as the UAE, Saudi Arabia, and South Africa are increasing administrative capacity through public-sector digitization and infrastructure development initiatives, which continue to require parallel physical documentation systems. Regional growth is further driven by expanding corporate sectors, rising foreign investments, and increasing establishment of educational institutions across African economies. Improvements in distribution networks and retail accessibility are also enhancing product availability, supporting gradual but sustained market expansion over the forecast period.

Key Players in the File Folders Market

- 3M Company

- ACCO Brands Corporation

- Smead Manufacturing Company

- Esselte Group

- Fellowes Brands

- Kokuyo Co., Ltd.

- PLUS Corporation

- Leitz

- Bantex

- Snopake Brands

- Pendaflex

- Avery Products Corporation

- Wilson Jones

- Elba

- Tops Products