Faux Fur Market Size

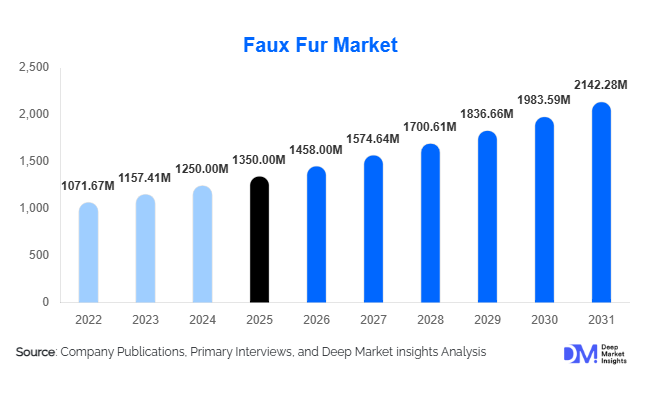

According to Deep Market Insights, the global faux fur market size was valued at USD 1,350 million in 2025 and is projected to grow from USD 1,458.00 million in 2026 to reach USD 2,142.28 million by 2031, expanding at a CAGR of 8.0% during the forecast period (2026–2031). The faux fur market growth is primarily driven by increasing consumer preference for cruelty-free and sustainable alternatives, rising adoption in fashion and home décor applications, and continuous innovation in synthetic fiber technologies that enhance texture realism and durability.

Key Market Insights

- Faux fur is rapidly replacing natural fur in fashion, driven by global bans on animal fur and strong ethical consumer sentiment.

- Polyester-based and recycled fibers are gaining traction, aligning the market with sustainability and circular economy goals.

- Europe dominates the global market, supported by stringent regulations and strong luxury fashion adoption.

- Asia-Pacific is the fastest-growing region, driven by rising disposable incomes and expanding textile manufacturing capabilities.

- E-commerce is accelerating product accessibility, especially among younger, fashion-conscious consumers.

- Technological advancements in textile engineering are improving quality, enabling the premium positioning of faux fur products.

What are the latest trends in the faux fur market?

Sustainable and Recycled Faux Fur Materials

The faux fur market is witnessing a strong shift toward sustainability, with manufacturers increasingly adopting recycled polyester and bio-based fibers. This trend is driven by rising environmental concerns and regulatory pressures to reduce plastic waste and carbon emissions. Brands are focusing on transparency, traceability, and eco-label certifications to appeal to environmentally conscious consumers. Circular economy practices, such as recycling textile waste into new faux fur products, are gaining traction. Additionally, collaborations between textile manufacturers and fashion brands are promoting sustainable product lines, positioning faux fur as an ethical and eco-friendly alternative to both real fur and traditional synthetic materials.

Premiumization and Realistic Texture Innovation

Advancements in textile technology are enabling the production of highly realistic faux fur that closely mimics natural fur in texture, density, and appearance. Innovations such as digital printing, 3D fiber structuring, and advanced dyeing techniques are enhancing product quality. This has allowed faux fur to penetrate premium and luxury fashion segments, where aesthetics and tactile experience are critical. Designers are increasingly incorporating faux fur into high-end collections, elevating its perception from a substitute material to a desirable fashion element. The trend toward premiumization is also reflected in higher price points and improved margins for manufacturers.

What are the key drivers in the faux fur market?

Rising Ethical Consumerism

Growing awareness of animal welfare issues has significantly influenced consumer purchasing decisions, leading to widespread adoption of faux fur. Many global fashion brands have committed to eliminating real fur from their collections, further boosting demand. Regulatory bans on animal fur in key markets such as Europe and North America have reinforced this shift, making faux fur a mainstream material across apparel and accessories.

Expansion of Fast Fashion and E-Commerce

The rapid growth of fast fashion and online retail platforms has increased the accessibility and affordability of faux fur products. E-commerce channels enable consumers to explore a wide variety of designs and price points, while fast fashion brands drive frequent product launches. This combination has accelerated market penetration, particularly among younger demographics who prioritize style and affordability.

What are the restraints for the global market?

Environmental Concerns Related to Synthetic Fibers

Despite its ethical advantages over real fur, faux fur is often criticized for its reliance on petroleum-based materials, which contribute to microplastic pollution and environmental degradation. This has led to growing scrutiny from environmental groups and consumers, potentially limiting adoption unless sustainable alternatives are further developed.

Volatility in Raw Material Prices

The cost of producing faux fur is closely tied to the price of petrochemical inputs such as polyester and acrylic. Fluctuations in crude oil prices can impact manufacturing costs and profit margins, creating pricing challenges for market participants and affecting overall competitiveness.

What are the key opportunities in the faux fur industry?

Adoption of Bio-Based and Circular Materials

The development of bio-based fibers and closed-loop recycling systems presents a significant growth opportunity for the faux fur market. Companies investing in sustainable innovations can differentiate their products, attract environmentally conscious consumers, and comply with evolving regulations. This shift is expected to drive premium pricing and long-term growth.

Expansion in Emerging Markets

Emerging economies in the Asia-Pacific and Latin America offer substantial growth potential due to rising disposable incomes and increasing exposure to global fashion trends. Localization of production and distribution can help manufacturers tap into these markets effectively, reducing costs and improving accessibility.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1350 Million |

| Market Size in 2026 | USD 1458 Million |

| Market Size in 2031 | USD 2142.28 Million |

| CAGR | 8.0% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Short hair faux fur continues to dominate the global market, accounting for approximately 35% of the total share in 2025. Its leadership is primarily driven by its versatility, cost-efficiency, and ease of integration across multiple product categories, especially in apparel and accessories. The lightweight nature of short hair faux fur makes it highly suitable for mass-market fashion, aligning well with fast fashion cycles and high-volume production requirements. Additionally, its relatively lower production cost compared to long hair variants enables broader adoption among mid-range and budget fashion brands, further strengthening its dominance.

Long hair faux fur represents the second-largest segment, driven by its premium aesthetic appeal and superior insulation properties, making it highly preferred in luxury outerwear and winter collections. The segment is particularly strong in colder regions such as Europe and North America, where demand for high-end winter apparel remains consistent. Meanwhile, textured, embossed, and printed faux fur segments are emerging as high-growth niches, fueled by increasing consumer demand for personalization and unique design elements. Advancements in digital printing and fiber engineering are enabling manufacturers to create intricate patterns and textures, allowing brands to differentiate their offerings and cater to evolving fashion trends.

Application Insights

The apparel segment leads the faux fur market, capturing nearly 45% of the global share in 2025, and remains the primary driver of overall demand. This dominance is largely attributed to the global shift toward cruelty-free fashion, coupled with strong seasonal demand for outerwear such as coats, jackets, and trims. The influence of major fashion brands adopting faux fur alternatives has significantly accelerated growth in this segment. Additionally, rapid product turnover in fast fashion and increasing penetration of vegan fashion lines are further reinforcing apparel’s leading position.

Home furnishings constitute the second-largest application segment, driven by rising consumer interest in luxury interiors and comfort-oriented products. Faux fur is widely used in blankets, throws, rugs, and upholstery, particularly in premium home décor markets across Europe and North America. The automotive segment is emerging as a high-growth application area, with manufacturers exploring faux fur for premium interiors, seat covers, and decorative trims as part of vehicle personalization trends. The toys and plush products segment continues to generate steady demand, especially in developed markets, where high-quality synthetic fibers are essential for safety, durability, and softness.

Distribution Channel Insights

Offline retail channels dominate the faux fur market, accounting for approximately 55% of total sales in 2025. This dominance is driven by consumer preference for physically evaluating product texture, softness, and quality before purchase critical factors in faux fur buying decisions. Specialty textile stores and department stores remain key distribution hubs, particularly for premium and luxury products. Additionally, established relationships between manufacturers and offline retailers ensure consistent supply chains and brand visibility.

However, online retail is the fastest-growing distribution channel, supported by the rapid expansion of e-commerce platforms and direct-to-consumer (D2C) strategies. Digital platforms provide consumers with access to a wider range of products, competitive pricing, and convenience, making them increasingly popular among younger demographics. The integration of advanced visualization tools, such as high-resolution imagery and augmented reality, is further enhancing online shopping experiences. Meanwhile, direct-to-manufacturer (B2B) channels play a crucial role in bulk supply, particularly for fashion brands and industrial buyers, enabling cost efficiencies and streamlined procurement processes.

End-Use Industry Insights

The fashion and apparel industry remains the largest end-use segment, contributing over 50% of the global market share, with a market size exceeding USD 700 million in 2025. Its dominance is driven by the increasing adoption of faux fur by global fashion houses, fast fashion brands, and emerging vegan fashion labels. The industry’s continuous demand for innovative materials, coupled with frequent product launches and seasonal collections, ensures sustained growth.

Home décor represents a significant secondary segment, supported by rising consumer spending on interior design and the growing popularity of luxury and comfort-focused living spaces. Faux fur products such as throws, cushions, and rugs are increasingly being used to enhance aesthetic appeal. The automotive industry is the fastest-growing end-use segment, with a projected CAGR exceeding 9%, as manufacturers incorporate faux fur into premium vehicle interiors and customization options. Export-driven demand is particularly strong in the Asia-Pacific region, where large-scale production capabilities and cost advantages enable manufacturers to supply global markets efficiently, reinforcing the region’s role as a key export hub.

Explore more data points, trends and opportunities Download Free Sample Report

Faux Fur Market Segmentations

By Product Type

- Short Hair Faux Fur

- Long Hair Faux Fur

- Curly Faux Fur

- Textured/Embossed Faux Fur

- Printed Faux Fur

By Application

- Apparel

- Home Furnishings

- Footwear

- Toys & Plush Products

- Automotive Interiors

- Fashion Accessories

By Distribution Channel

- Offline Retail

- Online Retail / E-commerce

- Direct-to-Manufacturer (B2B)

Regional Insights

North America

North America accounts for approximately 30% of the global faux fur market, with the United States representing the largest contributor. Regional growth is primarily driven by strong consumer awareness regarding animal welfare, widespread adoption of cruelty-free fashion, and regulatory measures discouraging the use of real fur. The presence of leading fashion brands and high consumer spending on premium apparel further supports demand. Additionally, the rapid expansion of e-commerce platforms and increasing preference for sustainable products are accelerating market growth. Canada also contributes significantly, particularly in winter apparel segments, where climatic conditions drive consistent demand for faux fur products.

Europe

Europe holds the largest share at around 35% in 2025, led by countries such as the UK, Germany, France, and Italy. The region’s dominance is strongly influenced by stringent regulations and bans on animal fur, which have accelerated the transition toward synthetic alternatives. Europe’s well-established luxury fashion industry plays a critical role in driving demand, with designers increasingly incorporating faux fur into high-end collections. Additionally, strong consumer preference for sustainable and ethically sourced products has encouraged innovation in recycled and bio-based faux fur materials. Government policies promoting circular economy practices and environmental sustainability further reinforce market growth in the region.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 9%, driven by rapid industrialization, rising disposable incomes, and expanding middle-class populations. China dominates both production and consumption, serving as a global manufacturing hub with extensive export capabilities. India is emerging as a high-growth market due to increasing urbanization, growing fashion consciousness, and government initiatives supporting textile manufacturing. Japan and South Korea contribute through demand for premium and technologically advanced faux fur products. The region’s strong export orientation, supported by cost-effective production and large-scale manufacturing infrastructure, is a key driver of global market expansion.

Latin America

Latin America is experiencing moderate growth, with Brazil and Mexico leading regional demand. Growth drivers include increasing urbanization, rising disposable incomes, and growing exposure to global fashion trends. The expansion of retail infrastructure and e-commerce platforms is improving product accessibility, while a growing middle class is driving demand for affordable luxury products. Additionally, the region’s developing textile industry is gradually increasing local production capabilities, supporting market growth.

Middle East & Africa

The Middle East & Africa region represents a niche but growing market for faux fur, particularly in luxury segments. The UAE and Saudi Arabia are key demand centers, driven by high disposable incomes, strong preference for premium lifestyle products, and increasing influence of global fashion trends. In Africa, South Africa leads demand, supported by a growing retail sector and rising consumer awareness. The region’s growth is further supported by the expansion of luxury retail outlets, tourism-driven demand, and increasing adoption of sustainable fashion alternatives among affluent consumers.

Key Players in the Faux Fur Market

- Aono Pile Co., Ltd.

- Ecopel

- Peltex Fibres SARL

- Kolunsag Muflon Sanayi

- Ningbo Zhongxin Fur Co., Ltd.

- Cixi Santai Chemical Fiber Co., Ltd.

- Jiangsu Unitex Textile Co., Ltd.

- Tongxiang Zhongwang Textile Co., Ltd.

- Zhejiang Dongxing Textile Co., Ltd.

- Haining Textile Co., Ltd.

- Fur Fabric International

- Taizhou City Lingmei Industrial Co.

- Sunwin Fur Products

- Jilin Chemical Fiber Group

- Hebei Zhongtai Textile