Fashion Apparel Market Size

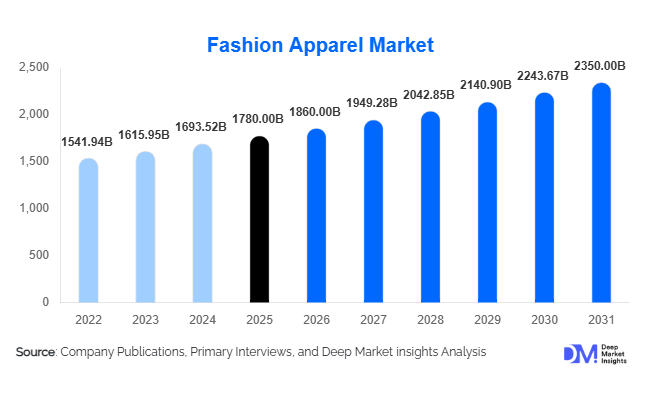

According to Deep Market Insights, the global fashion apparel market size was valued at USD 1,780 billion in 2025 and is projected to grow from USD 1,860 billion in 2026 to reach USD 2,350 billion by 2031, expanding at a CAGR of 4.8% during the forecast period (2026–2031). The market growth is primarily driven by rising disposable incomes, rapid urbanization, and the increasing penetration of e-commerce platforms that have transformed how consumers access and purchase fashion globally. The industry continues to evolve with the growing influence of fast fashion, digital-first retail strategies, and sustainability-driven innovation across supply chains.

Key Market Insights

- Fast fashion continues to dominate global apparel consumption, supported by shorter product cycles and trend-driven purchasing behavior among younger consumers.

- Online retail and D2C channels are rapidly gaining share, enabling brands to improve margins and enhance customer engagement through personalized offerings.

- Asia-Pacific dominates the global market, driven by large population bases, an expanding middle class, and strong manufacturing capabilities.

- Sustainable and ethical fashion is emerging as a critical differentiator, particularly in Europe and North America.

- Mid-range apparel accounts for the largest share, balancing affordability and quality for mass-market consumers.

- Technology adoption, including AI-driven demand forecasting and automated manufacturing, is reshaping production and retail efficiency.

What are the latest trends in the fashion apparel market?

Shift Toward Sustainable and Circular Fashion

Sustainability is becoming a defining trend in the fashion apparel market, with consumers increasingly prioritizing eco-friendly materials and ethical production processes. Brands are investing in recycled fabrics, biodegradable textiles, and circular business models such as resale and rental platforms. Governments and regulatory bodies, particularly in Europe, are introducing stricter environmental guidelines, pushing companies to adopt transparent supply chains. This shift is not only enhancing brand reputation but also enabling premium pricing strategies. Companies integrating sustainability into their core operations are gaining a competitive advantage while aligning with evolving consumer values.

Digital Transformation and Personalization

The integration of digital technologies is significantly transforming the fashion apparel landscape. E-commerce platforms, mobile applications, and AI-powered recommendation engines are enabling personalized shopping experiences. Virtual try-ons, augmented reality (AR), and data analytics are improving customer engagement and reducing return rates. Social media and influencer marketing continue to shape purchasing decisions, especially among younger demographics. The rise of direct-to-consumer (D2C) models is further enhancing brand-consumer relationships, allowing companies to gather valuable insights and optimize inventory management.

What are the key drivers in the fashion apparel market?

Rising Disposable Income and Urbanization

Increasing disposable incomes, particularly in emerging economies such as India, China, and Southeast Asia, are driving higher spending on apparel. Urban consumers are more fashion-conscious and influenced by global trends, leading to increased demand across multiple product categories. The expansion of organized retail and improved access to international brands further accelerate market growth.

Growth of E-commerce and Omnichannel Retail

The rapid growth of online shopping platforms has revolutionized the apparel industry. Consumers benefit from convenience, variety, and competitive pricing, while brands gain access to a global customer base. Omnichannel strategies, combining online and offline experiences, are becoming essential for maintaining customer loyalty and improving sales conversions.

What are the restraints for the global market?

Volatility in Raw Material Prices

Fluctuations in the prices of key raw materials such as cotton and synthetic fibers pose a significant challenge to manufacturers. These variations impact production costs and profit margins, particularly for fast fashion brands operating on thin margins. Supply chain disruptions further exacerbate cost pressures and inventory management issues.

Sustainability Compliance Costs

While sustainability presents growth opportunities, it also requires substantial investment in sourcing, production, and certification processes. Smaller companies may struggle to meet regulatory requirements and consumer expectations, limiting their ability to compete with established players.

What are the key opportunities in the fashion apparel industry?

Expansion in Emerging Markets

Emerging economies in Asia-Pacific, Latin America, and Africa present significant growth opportunities due to rising middle-class populations and increasing urbanization. Localized product offerings, affordable pricing strategies, and digital retail expansion can help companies capture untapped demand in these regions.

Growth of Athleisure and Functional Apparel

The increasing focus on health and wellness has driven demand for athleisure and performance wear. This segment is growing faster than traditional apparel categories, supported by changing lifestyles and hybrid work environments. Brands investing in innovation and comfort-driven designs are well-positioned to capitalize on this trend.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1780 Billion |

| Market Size in 2026 | USD 1860 Billion |

| Market Size in 2031 | USD 2350 Billion |

| CAGR | 4.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Upper wear continues to dominate the fashion apparel market, accounting for approximately 32% of the global market share in 2025. The leadership of this segment is primarily driven by its high purchase frequency and rapid style turnover, as consumers tend to update tops, shirts, and t-shirts more frequently than other apparel categories. Seasonal fashion cycles, workplace dressing norms, and the influence of fast fashion brands further accelerate demand. Additionally, upper wear offers greater scope for design variation, branding, and customization, making it a focal point for both premium and mass-market players.

Lower wear and innerwear segments also contribute significantly to overall market revenues, supported by essential demand and replacement cycles. Meanwhile, sportswear and athleisure are among the fastest-growing product categories, driven by increasing health consciousness, hybrid work culture, and the blending of casual and functional clothing. This shift toward comfort-oriented apparel is expected to further strengthen these segments over the forecast period.

Application Insights

Women’s apparel represents the largest application segment, holding nearly 48% of the market share in 2025. This dominance is primarily attributed to higher purchase frequency, broader product diversity, and stronger influence of fashion trends compared to other segments. The segment benefits from continuous innovation in styles, seasonal collections, and fast fashion cycles, which encourage repeat purchases. Additionally, increasing workforce participation among women and rising disposable income levels further support segment growth globally.

Men’s apparel follows with steady growth, driven by increasing fashion awareness, grooming trends, and the expansion of casual and smart-casual categories. The kids segment is also gaining traction, supported by rising birth rates in emerging economies and growing parental preference for branded and premium clothing. The influence of social media and mini-fashion trends is further contributing to the expansion of the kidswear segment.

Distribution Channel Insights

Offline retail continues to dominate the fashion apparel market, accounting for approximately 58% of the global market share in 2025. The segment’s leadership is driven by the need for physical product evaluation, fit assurance, and experiential shopping. Department stores, specialty outlets, and branded retail chains play a crucial role in driving sales, particularly in premium and luxury segments, where in-store experience is a key differentiator.

However, online retail is rapidly gaining momentum, supported by convenience, wider product assortment, competitive pricing, and increasing smartphone penetration. E-commerce platforms and brand-owned websites are witnessing double-digit growth, particularly in emerging markets. Additionally, direct-to-consumer (D2C) channels are expanding significantly, enabling brands to enhance customer engagement, gather data insights, and improve profit margins by eliminating intermediaries. Omnichannel strategies integrating online and offline experiences are becoming increasingly critical for sustained growth.

Price Segment Insights

The mid-range segment leads the fashion apparel market with approximately 45% share in 2025, driven by its strong value proposition of affordability combined with acceptable quality and design. This segment caters to a broad consumer base across both developed and emerging economies, making it the most commercially viable category for global brands.

Premium and luxury segments are experiencing steady growth, particularly in North America, Europe, and the Middle East, supported by rising disposable incomes, brand consciousness, and demand for exclusive products. These segments benefit from higher margins and strong brand loyalty. Meanwhile, the economy segment remains significant in price-sensitive markets such as Asia-Pacific and Latin America, where large population bases and cost-conscious consumers drive volume sales. The coexistence of all price segments highlights the market’s diverse consumer landscape.

Explore more data points, trends and opportunities Download Free Sample Report

Fashion Apparel Market Segmentations

By Product Type

- Upper Wear

- Lower Wear

- Innerwear & Loungewear

- Ethnic & Traditional Wear

- Sportswear & Activewear

- Outerwear

- Accessories Apparel

By Application

- Men

- Women

- Kids

- Unisex / Gender-neutral

By Distribution Channel

- Offline Retail

- Online Retail

- Direct-to-Consumer (D2C)

By Price Segment

- Economy / Mass

- Mid-range

- Premium

- Luxury / Designer

By Fabric Type

- Natural Fibers

- Synthetic Fibers

- Blended Fabrics

- Sustainable / Eco-friendly Fabrics

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global fashion apparel market, accounting for approximately 38% share in 2025, making it both the largest and fastest-growing region. China leads in terms of both production and consumption, benefiting from a well-established manufacturing ecosystem and strong domestic demand. India is the fastest-growing market in the region, with a projected CAGR of 7–8%, driven by rapid urbanization, a growing middle class, and increasing digital adoption.

The region’s growth is primarily fueled by rising disposable incomes, expansion of organized retail, increasing penetration of e-commerce platforms, and favorable government policies supporting textile manufacturing. Additionally, the presence of low-cost labor and strong export capabilities in countries such as Bangladesh and Vietnam further strengthen Asia-Pacific’s dominance in the global supply chain.

North America

North America holds approximately 22% of the global market share, with the United States being the primary contributor. The region is characterized by high consumer spending, strong brand penetration, and rapid adoption of fashion trends. Demand is increasingly shifting toward premium, sustainable, and athleisure apparel.

Key growth drivers include high e-commerce penetration, advanced logistics infrastructure, strong presence of global fashion brands, and increasing consumer preference for sustainable and ethically sourced clothing. The rise of D2C brands and digital-native fashion companies is also reshaping the competitive landscape in this region.

Europe

Europe accounts for nearly 20% of the global fashion apparel market, with major contributions from countries such as Germany, France, Italy, and the UK. The region is a global hub for luxury fashion and premium apparel, supported by well-established fashion houses and strong export demand.

Growth in Europe is driven by stringent sustainability regulations, high consumer awareness regarding ethical fashion, and strong demand for premium and luxury products. Additionally, innovation in sustainable materials and circular fashion models is positioning Europe as a leader in environmentally responsible apparel production.

Latin America

Latin America is experiencing moderate growth, led by Brazil and Mexico. The region’s fashion apparel market is supported by increasing urbanization, rising middle-class income, and growing fashion consciousness among consumers. Local brands and international retailers are expanding their presence to capture untapped demand.

However, economic volatility and currency fluctuations remain key challenges. Despite this, growth is supported by expanding retail infrastructure, increasing adoption of e-commerce, and rising demand for affordable fashion products, particularly in urban centers.

Middle East & Africa

The Middle East and Africa region is witnessing steady growth, with strong demand concentrated in countries such as the UAE and Saudi Arabia. The region benefits from high disposable incomes, a young population, and strong demand for premium and luxury apparel.

Growth drivers include expanding retail malls, increasing tourism, rising influence of Western fashion trends, and government initiatives to diversify economies beyond oil. In Africa, the region serves as an important manufacturing hub for global apparel exports, supported by low production costs and favorable trade agreements. The increasing penetration of digital retail and mobile commerce is further expected to accelerate market growth across both sub-regions.

Key Players in the Fashion Apparel Market

- Nike Inc.

- Adidas AG

- Inditex (Zara)

- H&M Group

- Fast Retailing (Uniqlo)

- LVMH

- Kering

- PVH Corp.

- VF Corporation

- Gap Inc.

- Levi Strauss & Co.

- Ralph Lauren Corporation

- Under Armour

- Hermès

- Burberry