Emergency Response Training Market Size

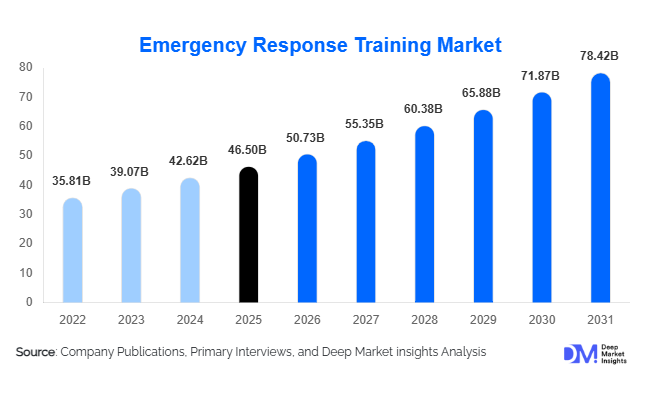

According to Deep Market Insights, the global emergency response training market size was valued at USD 46.5 billion in 2025 and is projected to grow from USD 50.73 billion in 2026 to reach USD 78.42 billion by 2031, expanding at a CAGR of 9.1% during the forecast period (2026–2031). The market growth is primarily driven by rising regulatory compliance requirements, increasing industrial and workplace safety mandates, and the growing adoption of advanced technologies such as VR and simulation-based training to enhance preparedness in high-risk industries globally.

Key Market Insights

- Simulation-based and VR training solutions are gaining traction, providing immersive, scenario-based learning experiences that improve emergency response effectiveness across industries.

- Emerging economies in Asia-Pacific, Africa, and Latin America are creating new demand, fueled by rapid industrialization, urbanization, and strengthening safety regulations.

- North America dominates the market, driven by stringent occupational safety regulations, widespread adoption of advanced training methods, and high public and private sector investments.

- Asia-Pacific is the fastest-growing region, supported by infrastructure expansion, increasing industrial workforce, and government safety initiatives in countries like India and China.

- Corporate ESG initiatives and workforce safety programs are expanding demand for comprehensive emergency response training, particularly in multinational corporations.

- Public-private partnerships and digital platforms are enabling scalable training programs and recurring revenue models for training providers globally.

What are the latest trends in the emergency response training market?

Technological Integration in Training Programs

Training providers are increasingly leveraging VR, AR, and AI-driven simulations to replicate real-world emergency scenarios. These immersive technologies enable trainees to experience fire outbreaks, chemical spills, and disaster events safely, enhancing skill retention and decision-making efficiency. Digital platforms also support remote and e-learning modules, making training accessible to distributed workforces and remote industrial sites. Gamified learning and scenario-based assessments are being integrated to increase engagement and practical application of skills.

Shift Toward Standardized and Regulatory Compliance Training

Organizations and governments are prioritizing regulatory compliance training for high-risk sectors such as oil & gas, healthcare, and manufacturing. OSHA, ISO, and regional safety standards are compelling companies to implement structured emergency response programs. Providers offering certifications aligned with global standards are seeing increased adoption, as compliance reduces legal liabilities and enhances workforce safety.

What are the key drivers in the emergency response training market?

Increasing Occupational Safety Regulations

Stringent safety regulations worldwide, particularly in high-risk industries, are driving consistent demand for emergency response training. Governments and regulatory bodies mandate periodic training to ensure workforce readiness for emergencies, increasing investments from corporations and public sector organizations.

Rising Incidence of Disasters and Industrial Accidents

Frequent natural disasters, fires, chemical spills, and public health emergencies are creating heightened awareness about preparedness. Organizations are investing in structured emergency response training to reduce operational downtime, minimize casualties, and ensure employee safety.

Adoption of Advanced Training Technologies

Simulation-based, VR, and AR training methods are increasingly preferred due to their ability to safely replicate high-risk scenarios. Such technologies are improving skill acquisition and emergency response efficiency, making them a critical factor for market growth.

What are the restraints for the global market?

High Implementation Costs

Advanced emergency response training setups, particularly those involving VR and simulation equipment, involve high capital expenditure, limiting adoption among small and medium enterprises. Cost constraints may restrict the scalability and widespread deployment of cutting-edge training solutions.

Lack of Standardized Global Training Frameworks

Regional differences in certification requirements and training standards create inconsistencies in program quality. Training providers must navigate fragmented regulations, which can hinder global expansion and uniform adoption of training programs.

What are the key opportunities in the emergency response training market?

Technological Advancement and VR/AR Integration

Advanced immersive technologies present opportunities for creating realistic, cost-effective training modules. VR and AR-based simulations reduce physical risk while allowing employees to experience complex emergency scenarios. This is especially valuable in high-risk sectors like oil & gas, aviation, and chemical manufacturing. Companies investing in scalable digital platforms can offer recurring subscription models and expand into geographically distributed markets.

Emerging Market Expansion

Rapid industrialization in Asia-Pacific, Africa, and Latin America is driving demand for structured safety programs. Governments in countries such as India, China, and Brazil are strengthening workplace safety laws and offering incentives for certified training programs. New entrants can tap into this growing demand by offering localized, compliant, and industry-specific training solutions.

Corporate ESG and Workforce Safety Initiatives

Organizations are increasingly linking emergency response training with ESG goals to enhance workforce well-being and operational resilience. Comprehensive training programs improve employee safety, reduce insurance premiums, and enhance brand reputation. Multinational corporations are investing in standardized global programs, creating opportunities for certified training providers to scale operations across regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 46.5 Billion |

| Market Size in 2026 | USD 50.73 Billion |

| Market Size in 2031 | USD 78.42 Billion |

| CAGR | 9.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Among training types, medical emergency training leads the global emergency response training market with an estimated 22% share in 2025, driven by its universal applicability across industries and the rising frequency of workplace health incidents and public health emergencies. The segment benefits from mandatory first-aid and CPR certification requirements across most developed and developing economies, making it a foundational component of workplace safety programs. Additionally, increasing awareness of cardiac arrest response, pandemic preparedness, and occupational health standards is further accelerating demand. In terms of delivery mode, simulation-based training dominates with approximately 28% market share, primarily due to its ability to replicate high-risk scenarios such as fires, chemical spills, and disaster situations in a controlled environment. The growing adoption of VR/AR technologies has significantly enhanced training effectiveness, enabling organizations to reduce real-world risk while improving employee preparedness and response times.

From a certification standpoint, regulatory compliance training accounts for nearly 35% of the market, supported by stringent global safety standards such as OSHA, ISO, and region-specific labor laws. Companies are increasingly prioritizing compliance to avoid legal liabilities, financial penalties, and operational disruptions. By provider type, private training companies hold a dominant 40% share, owing to their ability to offer specialized, scalable, and technology-driven training solutions. Their flexibility in customizing programs across industries and geographies positions them as preferred partners for multinational corporations and high-risk industries.

Application Insights

Emergency response training is extensively applied across high-risk industries such as oil & gas, healthcare, and manufacturing, which collectively contribute over 50% of total market demand. The oil & gas sector remains a key application area due to the inherently hazardous nature of operations, including offshore drilling, refining, and transportation of volatile materials. Similarly, the healthcare sector is witnessing strong demand driven by the need for rapid response to medical emergencies, infection control, and pandemic preparedness. Manufacturing industries are also investing heavily in training programs to mitigate workplace accidents, ensure compliance with international safety standards, and support export-oriented operations. Beyond traditional sectors, new applications are emerging in IT parks, corporate offices, educational institutions, and public infrastructure, particularly for fire safety, evacuation planning, and disaster preparedness. The rise of smart cities and large-scale infrastructure projects is further expanding application areas for emergency response training.

Export-driven industries are increasingly adopting standardized training programs to meet global compliance requirements, especially in regions supplying goods to North America and Europe. This trend is strengthening the demand for globally recognized certifications and structured safety programs.

Distribution Channel Insights

The distribution landscape is dominated by private training institutions and corporate in-house training programs, which collectively account for a significant portion of global revenue. Large enterprises are increasingly developing internal training capabilities to ensure continuous skill development and compliance with evolving safety standards. Digital transformation is reshaping distribution channels, with e-learning platforms, VR-based modules, and cloud-based training systems gaining widespread adoption. These platforms enable organizations to train geographically dispersed workforces efficiently while reducing costs associated with physical training infrastructure.

Public-private partnerships (PPPs) are emerging as a critical distribution channel, particularly in government-led disaster preparedness and public safety programs. Governments are collaborating with private players to scale training initiatives across urban and rural areas. Additionally, subscription-based training models are gaining traction, offering recurring revenue streams for providers and continuous access to updated training content for clients. Marketing channels such as industry events, digital campaigns, and targeted outreach are further enhancing awareness and adoption among corporate and industrial clients.

End-Use Segment Insights

The oil & gas industry leads the emergency response training market, accounting for the largest share due to its high-risk operational environment and stringent regulatory requirements. Activities such as offshore drilling, refining, and transportation of hazardous materials necessitate advanced and continuous training programs to ensure worker safety and operational continuity. The healthcare sector is the fastest-growing end-use segment, driven by increasing emphasis on patient safety, emergency preparedness, and pandemic response capabilities. Hospitals and healthcare institutions are investing heavily in advanced training programs, including simulation-based emergency response and infection control training, with the segment expected to grow at a CAGR exceeding 10%.

The manufacturing sector remains a key contributor, particularly in export-oriented economies where compliance with international safety standards is critical. Meanwhile, IT and corporate sectors are emerging as new growth areas, driven by the adoption of digital training platforms for fire safety, evacuation drills, and workplace emergency preparedness. Overall, industries with stringent compliance requirements and high workforce density are driving sustained demand, while new sectors are expanding the market scope through digital and scalable training solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Emergency Response Training Market Segmentations

By Training Type

- Fire Safety & Firefighting Training

- Medical Emergency Training (CPR, AED, First Aid)

- Disaster Management Training

- Hazardous Materials (HAZMAT) Training

- Industrial Emergency Response Training

- Workplace Safety & Evacuation Training

- Law Enforcement & Security Training

- Pandemic & Biohazard Response Training

By Delivery Mode

- Classroom-Based Training

- On-Site Practical Training

- Simulation-Based Training

- E-learning / Virtual Training

- VR/AR-Based Training

By End-User Industry

- Oil & Gas

- Manufacturing & Heavy Industry

- Healthcare & Hospitals

- Government & Public Sector

- Aviation & Transportation

- Construction & Infrastructure

- Energy & Utilities

- Corporate Offices & IT Parks

By Certification Level

- Basic Certification Programs

- Advanced/Professional Certification

- Regulatory Compliance Training

- Customized Corporate Training

By Service Provider

- Private Training Companies

- Government Agencies

- Corporate In-house Training

- Non-Profit Organizations

Regional Insights

North America

North America accounts for approximately 34% of the global emergency response training market in 2025, making it the largest regional market. The United States dominates regional demand, contributing nearly three-fourths of the market, supported by strict occupational safety regulations such as OSHA mandates, high awareness of workplace safety, and widespread adoption of advanced training technologies, including VR and simulation platforms. Canada also contributes significantly through industrial safety mandates and strong corporate training programs.

Key growth drivers in this region include continuous regulatory updates, high litigation risks associated with workplace incidents, strong insurance compliance requirements, and significant investments in public safety infrastructure. Additionally, the presence of major global training providers and high corporate spending on ESG and workforce safety initiatives further strengthen market growth.

Europe

Europe holds around 22% of the global market share, with leading countries including Germany, the United Kingdom, and France. The region is characterized by stringent labor laws, strong union influence, and comprehensive workplace safety frameworks, which drive consistent demand for emergency response training. Growth drivers in Europe include increasing focus on ESG compliance, sustainability-driven corporate strategies, and the adoption of standardized training programs across multinational operations. Additionally, the region’s advanced manufacturing base and emphasis on worker welfare are encouraging continuous investment in safety training. Government-backed initiatives promoting occupational health and safety further contribute to steady market expansion.

Asia-Pacific

Asia-Pacific (APAC) accounts for approximately 27% of the global market and is the fastest-growing region, with a CAGR exceeding 10%. Key markets include China, India, Japan, and Southeast Asian countries, where rapid industrialization and infrastructure development are driving demand for safety training.

Primary growth drivers include increasing industrial workforce, rising awareness of workplace safety, and government initiatives such as industrial safety reforms and compliance mandates. Countries like India and China are investing heavily in infrastructure and manufacturing, leading to higher demand for emergency preparedness training. Additionally, growing adoption of digital and simulation-based training solutions is accelerating market penetration in the region.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth, driven primarily by oil & gas sector expansion in countries such as the UAE, Saudi Arabia, and Nigeria. Large-scale infrastructure projects and increasing investments in industrial development are also contributing to market demand. Key drivers include stringent safety requirements in oil & gas operations, government-led infrastructure development programs, and rising focus on disaster preparedness in urban areas. Additionally, international collaborations and training partnerships are enhancing the availability of advanced training programs across the region.

Latin America

Latin America, led by Brazil and Mexico, represents a smaller but growing share of the global market. Industrial expansion, particularly in manufacturing and energy sectors, is driving demand for structured training programs. Growth drivers include increasing regulatory enforcement, rising safety awareness among employers, and growing participation in global trade requiring compliance with international safety standards. Government initiatives to improve workplace safety and investments in public sector training programs are also supporting market growth in the region.

Key Players in the Emergency Response Training Market

- Honeywell International Inc.

- 3M Company

- DuPont

- Siemens AG

- Raytheon Technologies

- Thales Group

- Lockheed Martin

- OSHA Training Institute

- Bureau Veritas

- SGS SA

- Intertek Group

- TÜV Rheinland

- RelyOn Nutec

- Falck Safety Services

- GP Strategies Corporation