Electronic Soap Dispenser Market Size

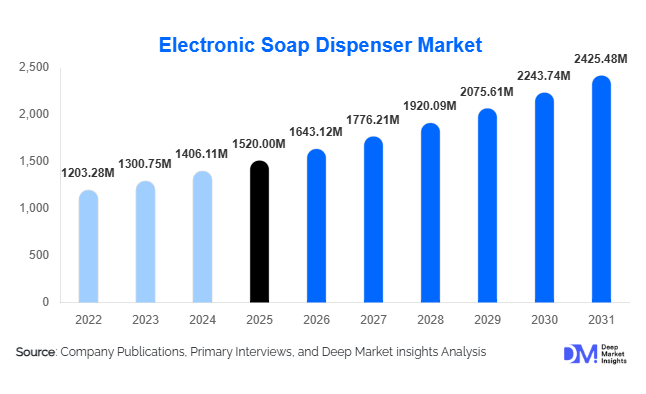

According to Deep Market Insights, the global electronic soap dispenser market size was valued at USD 1,520 million in 2025 and is projected to grow from USD 1,643.12 million in 2026 to reach USD 2,425.48 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The market growth is primarily driven by increasing hygiene awareness across residential and commercial environments, rapid expansion of healthcare and hospitality infrastructure, and rising adoption of touchless technologies in public sanitation systems.

Post-pandemic behavioral shifts have permanently strengthened demand for automated, sensor-based hygiene solutions. Commercial facilities such as hospitals, airports, shopping malls, corporate offices, and food-service establishments are increasingly replacing manual dispensers with electronic alternatives to minimize cross-contamination risks. In addition, growing smart home penetration and consumer preference for premium bathroom accessories are accelerating adoption in residential settings. Technological advancements, including infrared sensors, rechargeable lithium-ion batteries, adjustable dispensing mechanisms, and IoT-enabled refill monitoring systems, are further enhancing product efficiency and lifecycle cost advantages.

Key Market Insights

- Commercial end-use dominates the market, accounting for nearly 64% of total demand in 2025, driven by healthcare and hospitality infrastructure expansion.

- Wall-mounted dispensers lead the product segment with approximately 42% market share due to large-scale institutional installations.

- North America holds the largest regional share (34%), supported by stringent hygiene compliance standards in healthcare and food-service industries.

- Asia-Pacific is the fastest-growing region, expanding at nearly 9.5% CAGR due to infrastructure development in China and India.

- Battery-operated models account for 48% of installations, preferred for easy retrofitting and installation flexibility.

- The top five players collectively hold around 40% market share, indicating moderate competitive fragmentation.

What are the latest trends in the electronic soap dispenser market?

Smart & IoT-Enabled Hygiene Infrastructure

Integration of IoT-enabled electronic dispensers is emerging as a key trend in commercial facilities. Smart dispensers equipped with usage tracking, refill alerts, and remote monitoring capabilities enable facility managers to optimize maintenance schedules and reduce soap wastage by 10–15%. Large hospitals, airports, and corporate offices are increasingly investing in connected washroom systems as part of broader smart building initiatives. These systems improve operational efficiency, reduce downtime, and align with sustainability goals by minimizing overuse and leakage.

Sustainability and Refillable Cartridge Systems

Manufacturers are increasingly focusing on recyclable materials, refillable cartridges, and low-energy consumption designs. Stainless steel models with anti-corrosion properties are gaining popularity in premium commercial applications. Energy-efficient standby modes and rechargeable batteries are replacing disposable battery units, reducing lifecycle costs and environmental impact. ESG-driven procurement policies among multinational corporations are encouraging the adoption of sustainable dispenser systems.

What are the key drivers in the electronic soap dispenser market?

Heightened Hygiene Awareness

Global hygiene consciousness remains structurally elevated across healthcare, hospitality, and residential sectors. Regulatory mandates in hospitals and food-service establishments require contactless sanitation systems, directly boosting electronic dispenser adoption. The perception of improved cleanliness and reduced infection transmission continues to sustain replacement demand in developed economies.

Commercial Infrastructure Expansion

Rapid construction of airports, IT parks, shopping malls, and hotels, particularly in Asia-Pacific and the Middle East, is accelerating large-scale installations. Public sanitation upgrades under smart city programs further stimulate demand. Governments are allocating increased budgets toward automated washroom facilities in transportation hubs and healthcare centers.

What are the restraints for the global market?

High Initial Cost Compared to Manual Alternatives

Electronic soap dispensers are typically 2–4 times more expensive than manual variants, limiting penetration in price-sensitive regions. Budget constraints in small enterprises and public institutions can slow adoption rates.

Maintenance and Technical Reliability Issues

Sensor malfunctions, battery replacement needs, and clogging issues in high-usage environments increase operational costs. In developing regions, inconsistent maintenance practices can reduce product lifespan and discourage bulk procurement.

What are the key opportunities in the electronic soap dispenser industry?

Emerging Market Public Sanitation Programs

Large-scale government initiatives in India, Southeast Asia, and GCC countries aimed at improving public sanitation infrastructure present strong procurement opportunities. Smart city missions and healthcare infrastructure modernization programs are generating sustained institutional demand.

Premium Residential & Smart Home Integration

The rising adoption of smart home ecosystems creates opportunities for sensor-based bathroom accessories. Integration with voice assistants and automated home systems can create differentiated premium offerings. The residential segment is projected to grow at nearly 9% CAGR through 2031.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1520 Million |

| Market Size in 2026 | USD 1643.12 Million |

| Market Size in 2031 | USD 2425.48 Million |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Wall-mounted electronic soap dispensers dominate the global market, accounting for approximately 42% of total revenue in 2025. The leadership of this segment is primarily driven by high-volume installations across hospitals, hotels, airports, corporate offices, shopping malls, and educational institutions. Wall-mounted units are preferred in commercial settings because they optimize space utilization, reduce countertop clutter, and offer better durability in high-traffic environments. Additionally, institutional procurement policies often standardize wall-mounted formats for ease of maintenance and refill management. Increasing retrofit activities in healthcare facilities and hospitality chains across North America and Europe further strengthen this segment’s dominance.

Countertop models remain highly popular in residential applications due to aesthetic appeal and flexibility in placement. Deck-mounted integrated systems are gaining traction in premium commercial washrooms and luxury hospitality projects, particularly where seamless sink integration enhances hygiene perception. Portable compact models, although niche, are witnessing rising adoption in temporary healthcare camps, travel, and small office setups.

Installation Type Insights

Battery-operated dispensers lead the installation segment with nearly 48% share in 2025, largely due to their ease of installation and compatibility with retrofit projects. These units require minimal infrastructure modification, making them ideal for upgrading existing manual dispensers in commercial buildings. The ability to install without electrical rewiring significantly reduces upfront capital expenditure, particularly for small and mid-sized enterprises.

Rechargeable electronic dispensers are the fastest-growing sub-segment, supported by sustainability initiatives and long-term cost savings. Organizations aiming to reduce battery waste and maintenance cycles are increasingly adopting USB or lithium-ion rechargeable systems. Hardwired dispensers are predominantly installed in newly constructed commercial buildings, airports, and smart infrastructure projects where centralized power systems are incorporated at the design stage.

Material Insights

Plastic-based dispensers (ABS and polycarbonate) account for approximately 55% of the total market share, driven by affordability, lightweight construction, corrosion resistance, and ease of mass production. These models are particularly dominant in price-sensitive emerging markets across Asia-Pacific and Latin America, where cost efficiency influences procurement decisions.

Stainless steel dispensers are expanding rapidly in premium commercial environments due to superior durability, vandal resistance, and modern aesthetics. Adoption is particularly strong in Europe and North America, where corporate offices and luxury hospitality chains prioritize premium washroom design standards. Glass and composite materials represent a smaller but growing niche in high-end residential and boutique hospitality projects.

Capacity Insights

The 600 ml–1000 ml capacity segment leads the market with approximately 38% share in 2025. This range strikes a balance between refill frequency and dispenser size, making it ideal for office buildings, restaurants, retail complexes, and mid-sized healthcare facilities. Reduced maintenance cycles and optimized soap consumption make this capacity highly cost-efficient for facility managers.

Bulk dispensers above 1000 ml are widely deployed in airports, hospitals, factories, and transportation hubs with heavy daily footfall. Smaller units below 300 ml are primarily targeted at residential consumers and boutique commercial installations.

End-Use Insights

Commercial applications dominate the market with nearly 64% of global demand in 2025. Healthcare facilities represent the largest contributor within this segment, supported by stringent infection control regulations and ongoing hospital infrastructure expansion. The global healthcare infrastructure sector, valued in trillions of dollars, continues to generate steady procurement demand for automated hygiene systems. The hospitality sector is another major contributor, driven by hotel renovations, premium restroom upgrades, and brand-driven hygiene differentiation strategies. Corporate offices and IT parks increasingly adopt touchless washroom systems as part of employee wellness initiatives.

The residential segment is the fastest-growing end-use category, projected to expand at close to 9% CAGR through 2031. Rising disposable incomes, smart home integration, and growing consumer hygiene awareness are key drivers. Industrial applications, particularly in food processing and manufacturing facilities, are also expanding due to regulatory compliance requirements for sanitation and worker safety.

Explore more data points, trends and opportunities Download Free Sample Report

Electronic Soap Dispenser Market Segmentations

By Product Type

- Wall-Mounted Electronic Soap Dispensers

- Countertop (Freestanding) Dispensers

- Deck-Mounted Integrated Systems

- Portable/Compact Dispensers

By Installation Type

- Battery-Operated

- Rechargeable (USB/Lithium-Ion)

- Hardwired

By Material

- Plastic (ABS/Polycarbonate)

- Stainless Steel

- Glass & Composite Materials

By End-Use

- Residential

- Commercial

- Industrial

By Distribution Channel

- Online Retail

- Supermarkets/Hypermarkets

- Specialty Stores

- B2B Institutional Sales

Regional Insights

North America

North America accounts for approximately 34% of the global market share in 2025, with the United States contributing nearly 27% individually. The region’s dominance is driven by stringent hygiene regulations enforced across healthcare and food-service industries, strong replacement demand, and widespread adoption of smart building technologies. High labor costs further encourage automated hygiene systems to reduce maintenance frequency. Additionally, ongoing hospital modernization programs and airport infrastructure upgrades continue to stimulate the procurement of sensor-based dispensers.

Europe

Europe holds around 26% of the global market share, led by Germany, the United Kingdom, and France. Regional growth is strongly supported by sustainability-focused procurement policies, high standards for public sanitation, and premium washroom renovations in commercial real estate. The European Union’s emphasis on eco-friendly building certifications encourages the adoption of energy-efficient and stainless-steel dispenser systems. The hospitality and tourism sectors in Western Europe also contribute significantly to recurring demand.

Asia-Pacific

Asia-Pacific represents approximately 28% of global demand and is the fastest-growing region, expanding at nearly 9.5% CAGR. China serves as both the largest manufacturing hub and a major domestic consumer, benefiting from rapid urbanization and infrastructure growth. India is the fastest-growing country within the region, supported by large-scale sanitation initiatives, smart city programs, and healthcare infrastructure expansion. Rising middle-class incomes and increasing commercial construction across Southeast Asia further accelerate regional growth.

Middle East & Africa

The Middle East & Africa region holds around 7% market share. Growth is driven primarily by large-scale infrastructure projects in the UAE and Saudi Arabia, including airports, luxury hotels, shopping malls, and smart city developments. High-end hospitality investments and government-backed diversification initiatives away from oil-dependent economies are creating sustained demand for premium electronic washroom solutions.

Latin America

Latin America accounts for approximately 5% of the global market, with Brazil and Mexico leading regional installations. Growth is supported by expanding retail infrastructure, healthcare facility upgrades, and increasing hygiene awareness among urban consumers. While price sensitivity remains a constraint, rising investments in commercial real estate and the modernization of public facilities are gradually strengthening demand for electronic dispensers across the region.

Key Players in the Electronic Soap Dispenser Market

- TOTO Ltd.

- Sloan Valve Company

- Bobrick Washroom Equipment, Inc.

- GOJO Industries, Inc.

- Kohler Co.

- Bradley Corporation

- Simplehuman

- SVAVO

- Lovair

- Alpine Industries

- ASI American Specialties, Inc.

- Dolphy Australia

- Orchids International

- Xiaomi Corporation

- Reckitt (Dettol brand)