Electronic Drums Market Size

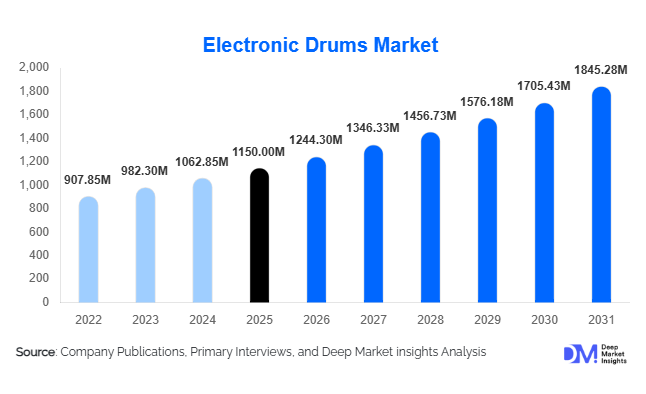

According to Deep Market Insights, the global electronic drums market size was valued at USD 1,150 million in 2025 and is projected to grow from USD 1244.30 million in 2026 to reach USD 1845.28 million by 2031, expanding at a CAGR of 8.2% during the forecast period (2026–2031). The electronic drums market growth is primarily driven by the increasing adoption of home-based music production, the rising popularity of digital music genres, and advancements in drum module and pad technologies. Additionally, growing interest among amateur musicians, content creators, and music learners is further accelerating demand globally.

Key Market Insights

- Electronic drums are gaining traction as compact and noise-controlled alternatives to traditional acoustic kits, especially in urban environments.

- Integration with digital audio workstations (DAWs) and MIDI systems is enhancing their utility for music production and recording.

- Asia-Pacific dominates the global market, supported by strong manufacturing bases and rising demand from emerging economies.

- North America remains a key consumption hub, driven by advanced music production ecosystems and high consumer spending.

- Online retail channels are expanding rapidly, enabling broader product accessibility and price transparency.

- Technological innovation, including AI-enabled learning and wireless connectivity, is reshaping user experience and product differentiation.

What are the latest trends in the electronic drums market?

AI-Enabled Learning and Smart Drumming Systems

Electronic drum manufacturers are increasingly integrating artificial intelligence and smart learning tools into their products. These systems provide real-time feedback on rhythm accuracy, timing, and technique, making them highly attractive for beginners and self-learners. AI-powered drum kits can adapt to user skill levels, offering personalized training modules and interactive lessons. This trend is aligned with the broader shift toward digital education and remote learning, where musicians seek convenient and efficient ways to develop skills. Mobile app integration further enhances the learning experience by providing analytics, tutorials, and performance tracking, positioning electronic drums as comprehensive learning platforms.

Growth of Home Studios and Content Creation

The rise of home studios and digital content creation is significantly influencing the electronic drums market. Musicians, YouTubers, and independent producers are increasingly investing in compact and versatile instruments that integrate seamlessly with recording software. Electronic drums offer advantages such as direct audio output, customizable sound libraries, and compatibility with production tools, making them ideal for modern content ecosystems. Social media platforms and streaming services are driving demand for high-quality audio production, encouraging users to adopt electronic drum kits as essential components of their setups.

What are the key drivers in the electronic drums market?

Expansion of Digital Music Production Ecosystems

The widespread adoption of digital audio workstations and music production software has created a strong demand for electronic instruments. Electronic drums play a critical role in these ecosystems by enabling seamless integration with MIDI and recording platforms. This trend is particularly prominent among independent artists and small studios, who rely on cost-effective and flexible tools for music creation.

Technological Advancements in Hardware Components

Continuous innovation in drum hardware, including mesh-head pads, advanced sound modules, and realistic cymbal triggers, has significantly improved the playing experience. These advancements have reduced the performance gap between electronic and acoustic drums, encouraging adoption among professional musicians. Enhanced durability and customization options are further contributing to market growth.

What are the restraints for the global market?

High Cost of Premium Electronic Drum Kits

Despite growing adoption, high-end electronic drum kits remain expensive due to advanced technology and premium components. This limits accessibility for entry-level users and price-sensitive markets, particularly in developing regions.

Preference for Acoustic Drums Among Traditional Musicians

Many professional drummers continue to prefer acoustic kits for their natural sound and dynamic response. This cultural and performance-based preference poses a challenge for widespread adoption of electronic alternatives in certain segments.

What are the key opportunities in the electronic drums industry?

Emerging Market Expansion

Emerging economies such as India, Brazil, and Indonesia present significant growth opportunities due to rising disposable incomes and increasing interest in music education. Localization of pricing and product features can help manufacturers penetrate these markets effectively.

Hybrid Acoustic-Electronic Systems

The development of hybrid drum systems that combine acoustic and electronic elements is opening new avenues for professional musicians. These systems offer enhanced sound versatility and are increasingly used in live performances and studio settings.

Product Type Insights

Full electronic drum kits continue to dominate the global market, accounting for approximately 52% of the total market share in 2025. The leadership of this segment is primarily driven by its all-in-one functionality, offering integrated drum modules, pads, cymbals, and connectivity features that appeal to both entry-level users and professional musicians. The growing adoption of home studios and digital music production has significantly boosted demand for full kits, as they provide a complete solution without the need for additional components. Within this category, mid-range kits are the most popular sub-segment, as they strike an optimal balance between affordability and advanced features such as mesh heads, customizable sound libraries, and DAW compatibility. Additionally, increasing product innovation from manufacturers, such as enhanced sound realism and compact foldable designs, has further strengthened this segment’s dominance.

Drum pads and controllers are witnessing steady growth, particularly among electronic music producers and DJs who require compact, portable instruments for beat-making and live performances. Meanwhile, hybrid drum systems are emerging as a niche but high-value segment, driven by professional musicians seeking to combine acoustic feel with electronic versatility in live concerts and studio environments.

Component Insights

Hardware components lead the electronic drums market, contributing nearly 68% of the total market share. This dominance is largely attributed to the critical role of physical components such as drum modules, pads, cymbals, and pedals in defining the performance and user experience of electronic drum kits. Among these, drum modules act as the core of the system, determining sound quality, customization capabilities, and connectivity features. Continuous advancements in hardware, such as mesh-head pads that replicate the feel of acoustic drums and multi-zone cymbals, are driving strong replacement demand and upgrades among existing users.

The growth of this segment is further supported by increasing consumer preference for realistic playing experiences, especially among professional drummers transitioning from acoustic to electronic kits. While software components, including sound libraries and DAW integration tools, are gaining traction, they remain complementary to hardware. However, the rising importance of software ecosystems is expected to gradually increase its share, particularly as digital music production becomes more mainstream.

Connectivity Insights

Wired connectivity systems dominate the market with approximately 64% share in 2025, primarily due to their reliability, stability, and minimal latency, factors that are critical for professional recording and live performances. USB and MIDI connections remain the standard for seamless integration with computers, audio interfaces, and production software. The dominance of wired systems is further reinforced by their widespread compatibility with existing studio infrastructure and lower susceptibility to signal interference.

However, wireless connectivity is emerging as a rapidly growing segment, driven by increasing demand for convenience, portability, and clutter-free setups among home users and amateur musicians. Bluetooth-enabled drum kits and wireless MIDI solutions are gaining popularity, particularly in the entry-level and mid-range segments. As wireless technologies continue to improve in terms of latency and reliability, their adoption is expected to increase, especially in non-professional applications.

End-User Insights

Amateur and individual learners represent the largest end-user segment, accounting for approximately 38% of the global market share. This segment’s dominance is driven by the growing popularity of music as a hobby, the rise of online learning platforms, and the increasing availability of affordable electronic drum kits. The accessibility of tutorials on platforms such as YouTube and mobile learning apps has significantly lowered the barrier to entry, encouraging more individuals to take up drumming.

Professional musicians and recording studios continue to be key contributors, particularly in the premium segment where demand for high-performance kits with advanced sound modules and customization features remains strong. Educational institutions are also emerging as a significant growth driver, as schools and music academies increasingly adopt electronic drums due to their low maintenance, space efficiency, and volume control capabilities. Additionally, demand from content creators and independent artists is expanding rapidly, further diversifying the end-user base.

Distribution Channel Insights

Online retail channels hold a leading position in the electronic drums market, accounting for around 42% of the total market share. The growth of this segment is primarily driven by the increasing penetration of e-commerce platforms, which offer a wide range of products, competitive pricing, and the convenience of home delivery. Consumers benefit from detailed product comparisons, user reviews, and promotional discounts, making online channels the preferred choice, especially for entry-level and mid-range products.

Direct-to-consumer (D2C) sales through brand websites are also gaining momentum, enabling manufacturers to strengthen customer relationships and improve profit margins. Despite the growth of online channels, offline retail remains relevant, particularly for high-end products where customers prefer hands-on experience before making a purchase. Specialty music stores continue to play a crucial role in providing product demonstrations, expert guidance, and after-sales services.

| By Product Type | By Component | By Connectivity | By End User | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 32% of the global electronic drums market, with the United States being the dominant contributor. The region’s growth is primarily driven by a well-established music industry, high disposable income levels, and widespread adoption of advanced music production technologies. The strong presence of professional musicians, recording studios, and content creators has significantly boosted demand for high-end electronic drum kits. Additionally, the increasing popularity of home studios and digital content creation platforms is further fueling market expansion. Technological adoption and early access to innovative products also position North America as a key market for premium electronic drum solutions.

Asia-Pacific

Asia-Pacific leads the global market with approximately 35% share in 2025 and is also the fastest-growing region, with a CAGR exceeding 9.5%. The region’s dominance is supported by its strong manufacturing base, particularly in countries such as Japan and China. Japan is recognized for its technological innovation and high-quality products, while China plays a crucial role in cost-effective mass production and exports. India is emerging as a high-growth market, driven by increasing youth interest in music, rising disposable incomes, and expanding digital penetration. Government initiatives promoting local manufacturing and the rapid growth of e-commerce platforms are further accelerating market growth across the region.

Europe

Europe holds approximately 22% of the global market share, with key demand coming from Germany, the United Kingdom, and France. The region’s growth is driven by a strong cultural emphasis on music education, widespread participation in live performances, and increasing adoption of digital instruments in professional studios. Additionally, government support for arts and cultural programs has contributed to sustained demand. The rising popularity of electronic music genres and the presence of established music festivals across Europe further support market expansion. Increasing adoption of home recording setups among independent artists is also driving demand for electronic drum kits.

Latin America

Latin America accounts for around 5% of the global market, with Brazil and Mexico as the primary contributors. Market growth in this region is driven by increasing interest in digital music production, growing internet penetration, and the expansion of online retail channels. The rising popularity of music as a form of entertainment and self-expression among younger populations is also contributing to demand. Additionally, the affordability of entry-level electronic drum kits is enabling wider adoption in price-sensitive markets, supporting steady growth in the region.

Middle East & Africa

The Middle East & Africa region holds approximately 6% market share, with the UAE and South Africa leading demand. Growth in this region is primarily driven by increasing investments in entertainment infrastructure, including music festivals, live events, and performance venues. Rising disposable incomes and growing interest in Western music styles are also contributing to market expansion. In addition, the proliferation of music education programs and the adoption of digital instruments in urban centers are supporting demand. The region is gradually emerging as a promising market, particularly for mid-range and premium electronic drum kits.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Electronic Drums Market

- Roland Corporation

- Yamaha Corporation

- Alesis (inMusic Brands)

- Korg Inc.

- Pearl Corporation

- Simmons (Guitar Center Brands)

- ATV Corporation

- 2Box

- Medeli Electronics

- Gewa Music

- Carlsbro

- KAT Percussion

- Donner

- Behringer

- Zoom Corporation