Electric Kick Scooter Market Size

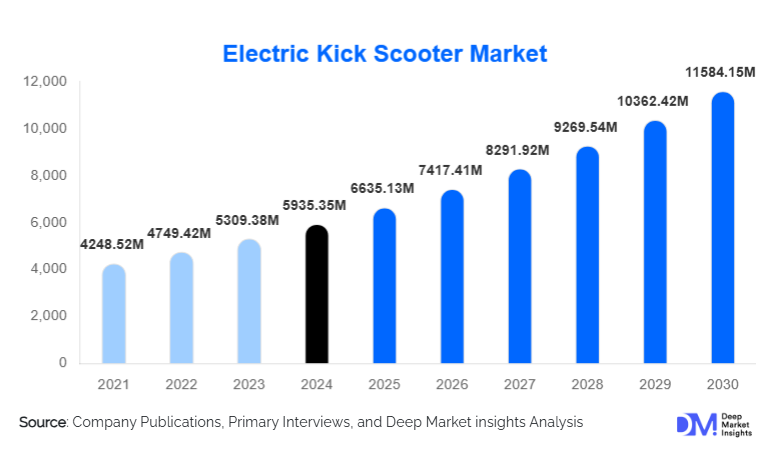

According to Deep Market Insights, the global electric kick scooter market size was valued at USD 5,935.35 million in 2025 and is projected to grow from USD 6,635.13 million in 2026 to reach USD 11,584.15 million by 2031, expanding at a CAGR of 11.79% during the forecast period (2026-2031). The electric kick scooter market growth is primarily driven by rising urban congestion, increasing demand for last-mile connectivity solutions, supportive government policies for zero-emission mobility, and continuous advancements in battery and motor technologies.

Key Market Insights

- Electric kick scooters are becoming a core component of urban micromobility ecosystems, addressing last-mile transportation gaps in densely populated cities.

- Personal ownership dominates global demand, supported by declining battery costs and rising consumer preference for flexible, private mobility options.

- Asia-Pacific leads global production and consumption, driven by large-scale manufacturing capacity and rapid urbanization.

- Shared mobility adoption is accelerating across North America and Europe due to city-level regulatory approvals and fleet expansion.

- Online and direct-to-consumer sales channels are reshaping purchasing behavior by offering competitive pricing and wider product availability.

- Smart connectivity and IoT integration are transforming product differentiation and fleet management efficiency.

Electric Kick Scooter Market Trends

Smart and Connected Electric Scooters

One of the most prominent trends in the electric kick scooter market is the integration of smart technologies. Manufacturers are increasingly embedding GPS tracking, Bluetooth connectivity, mobile app integration, anti-theft systems, and AI-based diagnostics into scooters. These features enhance user experience, enable real-time performance monitoring, and significantly reduce maintenance costs for shared mobility operators. Connected scooters also support geofencing, speed regulation, and predictive maintenance, making them highly attractive for urban fleet deployments. As cities demand better compliance and safety monitoring, smart scooters are becoming the industry standard rather than a premium add-on.

Design Optimization for Durability and Range

Manufacturers are focusing on improved structural durability, weather resistance, and extended riding range. The use of aircraft-grade aluminum frames, reinforced decks, and advanced suspension systems is increasing, particularly for shared mobility and commercial use. Battery optimization is another key trend, with higher energy-density lithium-ion cells enabling longer ranges without increasing weight. These improvements are expanding the applicability of electric kick scooters beyond short commutes to broader urban and semi-urban travel needs.

Electric Kick Scooter Market Drivers

Rising Demand for Last-Mile Urban Mobility

Urban congestion and insufficient public transportation coverage have intensified the need for efficient last-mile mobility solutions. Electric kick scooters offer a compact, affordable, and time-efficient alternative for short-distance travel, particularly in densely populated metropolitan areas. Their ability to integrate seamlessly with public transport systems has made them a preferred choice for daily commuters, students, and urban professionals, directly driving market expansion.

Supportive Government Policies and Emission Regulations

Governments across major economies are actively promoting electric mobility to reduce carbon emissions and improve air quality. Incentives such as subsidies, tax exemptions, reduced import duties, and investments in micromobility infrastructure are accelerating electric kick scooter adoption. Many cities are also expanding dedicated bike lanes and legalizing shared scooter fleets, creating a favorable regulatory environment for sustained growth.

Electric Kick Scooter Market Restraints

Regulatory Uncertainty and Safety Concerns

Despite growing adoption, inconsistent regulations related to speed limits, helmet usage, sidewalk riding, and fleet size restrictions pose challenges. Regulatory uncertainty across regions complicates large-scale deployment, particularly for shared mobility operators. Safety concerns related to accidents and pedestrian conflicts further restrain adoption in some cities.

Durability and Lifecycle Cost Challenges

Electric kick scooters, especially those used in shared fleets, face high wear-and-tear, vandalism, and battery degradation. Frequent maintenance and replacement costs can impact profitability, particularly in price-sensitive markets. Manufacturers must balance durability enhancements with cost control to maintain competitive pricing.

Electric Kick Scooter Market Opportunities

Expansion in Emerging Markets

Rapid urbanization and inadequate public transport infrastructure in emerging economies across Asia, Latin America, and the Middle East present significant growth opportunities. Demand for cost-effective, durable scooters suited to mixed road conditions is rising, supported by government EV initiatives and increasing smartphone penetration. Localization of manufacturing and distribution can further unlock these high-growth markets.

Integration with Smart City Infrastructure

The global push toward smart cities creates opportunities for integrating electric kick scooters into digital urban mobility platforms. Partnerships with municipalities for data sharing, fleet management, and infrastructure development can secure long-term contracts and recurring revenue streams for manufacturers and operators.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5935.35 Million |

| Market Size in 2026 | USD 6635.13 Million |

| Market Size in 2031 | USD 11584.15 Million |

| CAGR | 11.79% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Foldable electric kick scooters dominate the market, accounting for approximately 42% of global revenue in 2025. Their portability, lightweight design, and ease of storage make them ideal for daily commuters using public transportation. Non-foldable scooters are preferred in shared mobility fleets due to enhanced structural durability, while off-road and seated scooters cater to niche applications such as recreational riding and commercial patrol use. Product diversification is expanding the market’s addressable consumer base across both personal and professional use cases.

Battery Type Insights

Lithium-ion batteries represent nearly 78% of the global electric kick scooter market. Their superior energy density, faster charging capability, and longer lifecycle compared to lead-acid alternatives make them the preferred choice for manufacturers and consumers. Lithium iron phosphate (LFP) batteries are gaining traction in commercial and shared fleets due to improved thermal stability and safety, while lead-acid batteries are gradually declining due to weight and performance limitations.

Application Insights

Personal and private ownership remains the largest application segment, contributing approximately 55% of total market revenue in 2025. Shared mobility is the fastest-growing application, driven by urban fleet expansion, tourism recovery, and campus deployments. Commercial and institutional use, including security patrols, warehouses, and large campuses, is emerging as a high-growth niche, supported by demand for cost-efficient internal mobility solutions.

Distribution Channel Insights

Online marketplaces and direct-to-consumer platforms collectively account for nearly 48% of global sales. Consumers increasingly prefer digital channels for product comparison, reviews, and competitive pricing. Offline retail remains relevant for test rides, after-sales service, and premium product purchases, particularly in developed markets. Hybrid omnichannel strategies are becoming the norm among leading manufacturers.

Explore more data points, trends and opportunities Download Free Sample Report

Electric Kick Scooter Market Segmentations

By Product Type

- Foldable Electric Kick Scooters

- Non-Foldable / Rigid Electric Kick Scooters

- Off-Road / All-Terrain Electric Kick Scooters

- Seated Electric Kick Scooters

By Battery Type

- Lithium-Ion Battery Scooters

- Lithium Iron Phosphate (LFP) Battery Scooters

- Lead-Acid Battery Scooters

By Power Output

- Below 250W

- 250W–500W

- 501W–1,000W

- Above 1,000W

By Application

- Personal / Private Ownership

- Shared Mobility / Rental Fleets

- Commercial & Institutional Use

By Distribution Channel

- Direct-to-Consumer

- Online Marketplaces

- Offline Retail Stores

Regional Insights

Asia-Pacific

Asia-Pacific leads the electric kick scooter market with approximately 46% share in 2025. China dominates both manufacturing and consumption, while India is the fastest-growing market, supported by urbanization, government EV incentives, and rising middle-class adoption. Japan and South Korea contribute through technology-driven demand and premium product uptake.

Europe

Europe accounts for nearly 27% of global demand, led by Germany, France, the UK, and Spain. Strong regulatory support for micromobility, extensive cycling infrastructure, and high environmental awareness are key growth drivers. Shared mobility adoption is particularly strong in Western European cities.

North America

North America holds around 21% market share, driven primarily by the United States. Demand is supported by shared scooter fleets, premium personal scooters, and urban commuter adoption. Regulatory clarity in major cities is further supporting long-term growth.

Latin America

Latin America represents a smaller but rapidly expanding market, led by Brazil and Mexico. Urban congestion and affordability-driven demand are key adoption factors, with growing interest in shared mobility models.

Middle East & Africa

The Middle East and Africa region is witnessing rising adoption, particularly in the UAE and South Africa. Smart city initiatives, tourism-driven demand, and increasing EV infrastructure investments are supporting growth.