Electric Fan Market Size

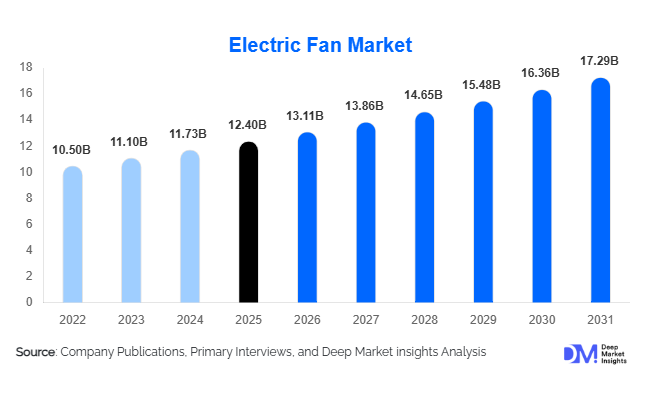

According to Deep Market Insights, the global electric fan market size was valued at USD 12.4 billion in 2025 and is projected to grow from USD 13.11 billion in 2026 to reach USD 17.29 billion by 2031, expanding at a CAGR of 5.7% during the forecast period (2026–2031). The electric fan market growth is primarily driven by rising global temperatures, increasing residential construction activity, rapid urbanization, and growing adoption of energy-efficient cooling appliances across residential, commercial, and industrial sectors.

Key Market Insights

- BLDC and energy-efficient fan technologies are rapidly transforming the industry, supported by government energy conservation programs and rising electricity costs globally.

- Asia-Pacific dominates the global electric fan market, driven by strong residential demand, urbanization, and large-scale manufacturing capabilities in China and India.

- Smart and IoT-enabled fans are gaining traction, particularly in North America and Europe, as consumers increasingly adopt connected home ecosystems.

- Industrial HVLS fans are witnessing strong demand growth, especially across warehouses, manufacturing plants, logistics hubs, and agricultural facilities.

- Online distribution channels are expanding rapidly, supported by e-commerce growth, direct-to-consumer strategies, and wider product accessibility.

- Solar-powered and rechargeable fans are emerging as high-potential segments, particularly in off-grid and power-deficient regions across Africa and South Asia.

Electric Fan Market Trends

Rapid Adoption of Energy-Efficient BLDC Fans

The electric fan industry is witnessing a significant transition toward Brushless DC (BLDC) motor technology due to increasing emphasis on energy efficiency and electricity savings. BLDC fans consume nearly 50–65% less electricity than traditional induction motor fans, making them increasingly attractive for residential and commercial applications. Governments across Asia-Pacific, particularly India, are encouraging adoption through energy-efficiency standards, labeling programs, and consumer awareness initiatives. Manufacturers are aggressively expanding BLDC product portfolios to address growing demand for sustainable appliances. Consumers are also increasingly willing to pay premium prices for lower operating costs, quieter operation, and improved durability. The trend is particularly strong in urban households where electricity expenses continue to rise and energy-conscious appliance purchasing behavior is accelerating.

Smart and Connected Fan Ecosystems Expanding

Smart electric fans integrated with IoT connectivity, mobile applications, voice assistants, and automation systems are reshaping the consumer appliance landscape. Manufacturers are introducing app-controlled ceiling fans equipped with occupancy sensors, AI-enabled airflow optimization, remote-control functionality, and compatibility with smart home ecosystems such as Alexa and Google Home. These features are gaining popularity among tech-savvy urban consumers seeking convenience, automation, and energy optimization. Smart fans are also increasingly integrated into green buildings and commercial infrastructure projects where centralized building management systems are utilized. Premiumization trends are encouraging consumers to shift toward aesthetically designed and technologically advanced fan products, particularly in North America, Europe, China, and affluent urban markets across Asia-Pacific.

Electric Fan Market Drivers

Rising Urbanization and Residential Construction

Rapid urbanization and large-scale housing development across emerging economies continue to drive substantial demand for electric fans globally. Countries such as India, China, Indonesia, Vietnam, and Brazil are witnessing sustained residential construction growth fueled by population expansion, rising middle-class income levels, and government-backed affordable housing initiatives. Ceiling fans remain one of the most essential and cost-effective cooling appliances in newly constructed residential units. Their affordability, low maintenance requirements, and low power consumption make them highly attractive for mass-market adoption. Additionally, replacement demand for decorative, premium, and energy-efficient fans is growing steadily in urban markets where consumers are upgrading home interiors and appliances.

Increasing Global Temperatures and Cooling Demand

Climate change and rising global temperatures are significantly increasing cooling requirements across residential, commercial, and industrial environments. Frequent heat waves and rising summer temperatures across Asia, Europe, and North America are boosting demand for affordable cooling appliances. Electric fans continue to offer a cost-effective alternative to air conditioning systems, particularly in price-sensitive and developing markets. Industrial and commercial facilities are also deploying high-performance ventilation systems and HVLS fans to improve worker comfort, air circulation, and operational efficiency. The growing need for low-energy cooling solutions is expected to sustain long-term market growth globally.

Electric Fan Market Restraints

Raw Material Price Volatility

Electric fan manufacturers continue to face challenges related to fluctuations in raw material prices, particularly steel, copper, aluminum, plastics, and electronic components. Commodity price volatility significantly impacts production costs and operating margins, especially within highly competitive economy and mid-range segments. Semiconductor shortages and supply chain disruptions also affect availability of smart electronics and BLDC components, increasing manufacturing complexity and pricing pressures. Smaller regional manufacturers often struggle to absorb rising input costs, leading to margin compression and increased market consolidation risks.

Growing Penetration of Air Conditioning Systems

In developed economies and premium urban markets, increasing adoption of air conditioning systems is limiting growth potential for conventional electric fans. Consumers with higher disposable incomes increasingly prefer centralized HVAC systems and advanced cooling solutions that provide temperature control and air purification. This trend is particularly visible across North America, parts of Europe, and affluent Asian cities. While fans continue to complement air conditioners in many households, standalone fan demand growth may moderate in high-income urban regions. Additionally, the electric fan industry remains highly fragmented, resulting in aggressive price competition and lower profitability in several markets.

Electric Fan Market Opportunities

Industrial Ventilation and Warehouse Expansion

Rapid expansion of logistics infrastructure, warehouses, manufacturing facilities, and industrial automation is creating significant opportunities for industrial ventilation systems and HVLS fans. Large-scale fulfillment centers, factories, transportation hubs, agricultural facilities, and data centers increasingly require efficient air circulation systems to reduce HVAC costs and improve indoor air quality. Industrial HVLS fans are gaining strong adoption because they provide energy-efficient airflow management across large commercial and industrial spaces. Emerging economies in Southeast Asia, the Middle East, and Latin America are witnessing increased infrastructure spending, further supporting industrial fan demand growth.

Growth in Solar-Powered and Rechargeable Fans

Solar-powered and rechargeable electric fans are emerging as high-growth opportunities in regions facing unreliable electricity supply and off-grid energy challenges. Governments and NGOs are increasingly promoting solar appliance adoption across rural communities in Africa, South Asia, and remote island economies. Portable rechargeable fans are witnessing strong demand among low-income households, healthcare centers, educational institutions, and humanitarian relief organizations. Manufacturers are investing in lightweight battery-integrated systems and hybrid solar technologies to improve product efficiency and affordability. Rising rural electrification programs and renewable energy investments are expected to accelerate adoption of alternative power-source fan systems over the coming years.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12.4 Billion |

| Market Size in 2026 | USD 13.11 Billion |

| Market Size in 2031 | USD 17.29 Billion |

| CAGR | 5.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Ceiling fans dominate the global electric fan market, accounting for nearly 42% of total market revenue in 2025. Their widespread adoption across residential housing projects, affordability, and low electricity consumption continue to support strong demand globally. Decorative and premium ceiling fans with integrated LED lighting, remote-control functionality, and BLDC motors are increasingly gaining traction in urban households. Table and pedestal fans remain highly popular in developing economies because of portability and affordability, while tower and bladeless fans are witnessing increasing demand in premium urban markets due to modern aesthetics and low-noise operation. Industrial ventilation fans, including axial and centrifugal systems, are experiencing rapid growth due to increasing demand from warehouses, manufacturing plants, logistics hubs, and agricultural facilities. High-velocity floor fans and HVLS systems are particularly gaining adoption in industrial and commercial infrastructure projects seeking energy-efficient airflow solutions.

Technology Insights

Conventional AC motor fans continue to account for the largest share of the market, representing nearly 61% of global revenues in 2025 due to their affordability and extensive installed base. However, BLDC fan technology is emerging as the fastest-growing segment globally. Consumers are increasingly shifting toward BLDC systems because of their superior energy efficiency, quieter operation, and lower long-term electricity costs. Smart connected fan systems are also witnessing strong growth, particularly across developed markets where IoT-enabled appliances are becoming mainstream. Manufacturers are integrating Wi-Fi connectivity, app-based controls, occupancy sensors, and voice assistant compatibility into premium fan portfolios. Solar-powered and hybrid battery-integrated fans are also gaining popularity across off-grid and power-constrained regions, supported by renewable energy adoption and rural electrification programs.

Distribution Channel Insights

Offline retail channels continue to dominate the electric fan market, accounting for approximately 68% of total global sales in 2025. Consumers in emerging markets often prefer physical product inspection and in-store purchasing for home appliances. Electronics stores, specialty appliance retailers, hypermarkets, and hardware stores remain important distribution channels globally. However, online retail is rapidly expanding due to increasing internet penetration, e-commerce adoption, and direct-to-consumer sales strategies. Online platforms enable consumers to compare specifications, pricing, reviews, and energy ratings more efficiently. Manufacturers are also strengthening digital marketing capabilities and exclusive online product launches to improve customer reach and profitability. E-commerce-led discounting and rapid delivery infrastructure are further accelerating online fan sales growth across Asia-Pacific, North America, and Europe.

Application Insights

Residential applications account for the largest share of the global electric fan market, representing nearly 58% of total demand in 2025. Rising urbanization, population growth, and residential construction activity continue to support strong ceiling fan and portable fan adoption globally. Commercial applications are also expanding steadily across offices, hospitality infrastructure, educational institutions, healthcare facilities, and retail establishments. Demand for low-noise and aesthetically designed fans is particularly increasing in premium commercial environments. Industrial applications represent one of the fastest-growing segments due to rapid warehouse expansion, industrial automation, and manufacturing growth. Agricultural ventilation systems and industrial cooling solutions are becoming increasingly important across poultry farms, greenhouses, logistics facilities, and heavy manufacturing plants where airflow optimization directly impacts operational productivity.

Price Range Insights

The mid-range segment accounts for the largest share of global electric fan sales, representing nearly 46% of market revenue in 2025. Consumers increasingly prefer products that balance affordability, energy efficiency, durability, and modern aesthetics. Economy fans continue to dominate volume sales in developing economies due to strong price sensitivity among mass-market consumers. However, premium electric fans are emerging as one of the fastest-growing categories, particularly in urban regions across North America, Europe, China, and India. Smart connectivity, decorative finishes, designer blades, silent operation, and integrated lighting systems are driving premium segment growth. Premiumization trends are enabling manufacturers to improve operating margins despite rising raw material costs and intense pricing competition.

Explore more data points, trends and opportunities Download Free Sample Report

Electric Fan Market Segmentations

By Product Type

- Ceiling Fans

- Table & Desk Fans

- Pedestal & Floor Fans

- Wall-Mounted Fans

- Exhaust & Ventilation Fans

- Tower & Bladeless Fans

- Industrial & Heavy-Duty Fans

By Technology

- AC Motor Fans

- BLDC Fans

- Smart Connected Fans

- Solar-Powered Fans

- Hybrid Battery-Integrated Fans

By Application

- Residential

- Commercial

- Industrial

By Distribution Channel

- Offline Retail

- Online Retail

- B2B Procurement Platforms

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global electric fan market, accounting for approximately 47% of total market revenue in 2025. China and India represent the two largest markets due to their massive populations, warm climatic conditions, strong residential construction activity, and large-scale manufacturing ecosystems. China remains the world’s leading producer and exporter of electric fans, supplying global consumer and industrial markets. India is among the fastest-growing markets due to rising urbanization, electrification, and increasing adoption of energy-efficient BLDC fans. Southeast Asian countries including Indonesia, Vietnam, Thailand, and the Philippines are also witnessing strong growth driven by tropical climate conditions and expanding middle-class populations.

North America

North America accounts for nearly 18% of the global electric fan market, led primarily by the United States. Demand is increasingly centered around premium ceiling fans, smart home-integrated systems, and industrial ventilation products. Consumers are increasingly adopting IoT-enabled and decorative fans for residential remodeling projects and smart home ecosystems. Warehousing expansion, logistics infrastructure growth, and commercial real estate investments are also supporting industrial fan demand across the region. Mexico is emerging as an important manufacturing hub due to nearshoring investments and export-oriented appliance production.

Europe

Europe represents approximately 16% of global market revenues, with Germany, France, the United Kingdom, Italy, and Spain serving as the major demand centers. Energy efficiency regulations, sustainability goals, and smart building initiatives are driving adoption of premium low-energy fans across residential and commercial sectors. Southern European countries experience particularly strong seasonal demand due to warmer climatic conditions. Consumers across Europe increasingly prioritize design aesthetics, quiet operation, and eco-friendly appliances, supporting premiumization trends within the market.

Latin America

Latin America accounts for nearly 9% of the global electric fan market, with Brazil representing the leading regional market due to warm climate conditions and strong residential demand. Mexico is witnessing increasing industrial fan demand supported by manufacturing expansion and export-oriented production facilities. Countries such as Colombia, Chile, and Argentina are also witnessing growing adoption of affordable cooling appliances across residential and commercial sectors.

Middle East & Africa

The Middle East & Africa region is witnessing strong market expansion driven by rising temperatures, infrastructure development, and increasing urbanization. Gulf Cooperation Council countries including Saudi Arabia and the UAE are investing heavily in commercial infrastructure, hospitality, and smart city projects, supporting rising demand for premium and industrial ventilation systems. Africa represents a long-term growth opportunity due to expanding electrification initiatives and increasing adoption of low-cost cooling appliances. Solar-powered and rechargeable fans are particularly gaining traction across off-grid and energy-deficient regions.

Key Players in the Electric Fan Market

- Panasonic Corporation

- Midea Group

- Crompton Greaves Consumer Electricals

- Orient Electric

- Havells India

- Hunter Fan Company

- Dyson

- Usha International

- Bajaj Electricals

- Emerson Electric

- LG Electronics

- Gree Electric Appliances

- Airmate Electrical

- Big Ass Fans

- Systemair