Egg Separator Market Size

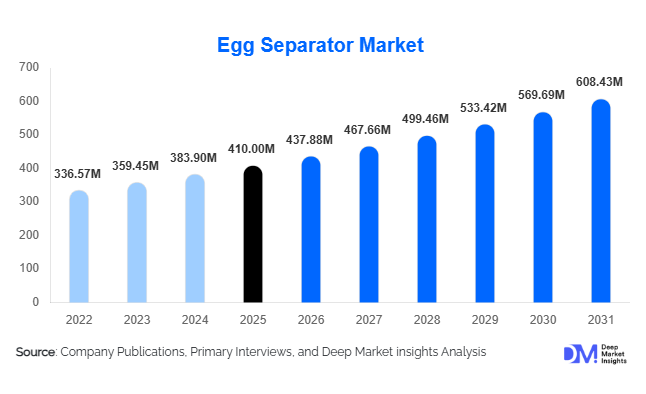

According to Deep Market Insights, the global egg separator market size was valued at USD 410 million in 2025 and is projected to grow from USD 437.88 million in 2026 to reach USD 608.43 million by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). The egg separator market growth is primarily driven by the rapid expansion of processed egg product manufacturing, increasing automation in food processing facilities, and rising demand for liquid egg and egg powder across bakery, confectionery, and ready-meal industries.

Key Market Insights

- Fully automatic egg separators dominate the market, accounting for nearly 58% of total revenue in 2025 due to high-capacity industrial installations.

- Egg processing companies represent the largest end-use segment, contributing approximately 42% of global demand.

- North America holds the largest regional share (32%), supported by strong liquid egg production and export capabilities.

- Asia-Pacific is the fastest-growing region, expanding at nearly 8% CAGR due to rapid poultry and food processing expansion.

- Integrated processing line systems account for over 60% of installations, as processors prefer complete automation solutions.

- Top five players control approximately 48% of global revenue, indicating moderate consolidation and strong technological differentiation.

What are the latest trends in the egg separator market?

Integration with Automated Egg Processing Lines

Modern egg separators are increasingly integrated into complete egg-breaking, pasteurization, and drying lines. Manufacturers are offering turnkey solutions that optimize yield, reduce contamination risk, and enable real-time monitoring. Smart sensors, automated shell detection, and AI-driven quality control systems are becoming standard features in high-capacity units. This integration enhances throughput efficiency and reduces manual handling, which is particularly critical in export-focused processing facilities. Processors are prioritizing stainless-steel hygienic designs compliant with stringent food safety standards, especially in North America and Europe.

Rising Demand for High-Capacity Industrial Systems

High-capacity separators capable of processing over 20,000 eggs per hour are witnessing strong adoption. This trend is linked to the expansion of egg powder and liquid egg export markets. Countries such as the United States, China, Brazil, and the Netherlands are expanding industrial processing infrastructure to serve global demand. Large-scale processors are investing in energy-efficient and high-yield separation systems to improve operational margins while complying with global food safety certifications.

What are the key drivers in the egg separator market?

Growth in Processed and Convenience Food Demand

Rising global consumption of bakery products, sauces, mayonnaise, protein beverages, and ready meals is significantly boosting demand for separated egg components. Egg whites and yolks are functional ingredients used for emulsification, aeration, and protein enrichment. As the global bakery and processed food industries expand steadily, industrial egg separation equipment demand continues to grow in parallel.

Automation and Labor Cost Optimization

Increasing labor costs and strict hygiene regulations are pushing processors toward automation. Fully automated egg separators minimize human contact, reduce contamination risks, and improve yield efficiency. Industrial facilities prefer automated systems to ensure consistent product quality and compliance with regulatory standards. The shift toward Industry 4.0 food processing further strengthens equipment demand.

What are the restraints for the global market?

High Initial Capital Investment

Fully automatic egg separators require substantial upfront capital, particularly high-capacity integrated systems. Small and mid-scale processors in developing markets often delay automation upgrades due to financing constraints. This limits adoption rates in price-sensitive regions.

Volatility in Poultry Production

Avian influenza outbreaks and fluctuations in egg production volumes can temporarily reduce processing investments. Supply disruptions in the poultry sector directly impact equipment demand cycles, creating short-term market uncertainty.

What are the key opportunities in the egg separator industry?

Export-Oriented Egg Processing Expansion

Growing international trade in egg powder, albumen, and yolk derivatives presents significant opportunities. Countries expanding export-focused processing facilities require high-capacity automated separators. Southeast Asia, Latin America, and parts of Africa are emerging as key investment destinations for new egg processing plants.

Smart Technology Integration and Predictive Maintenance

The adoption of IoT-enabled monitoring systems, predictive maintenance software, and yield optimization analytics provides differentiation opportunities for equipment manufacturers. Companies offering advanced data-driven separation systems can gain a competitive advantage, particularly in mature markets demanding operational efficiency.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 410 Million |

| Market Size in 2026 | USD 437.88 Million |

| Market Size in 2031 | USD 608.43 Million |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fully automatic egg separators dominate the global market, accounting for approximately 58% of the 2025 market value. The leadership of this segment is primarily driven by the rapid automation of egg processing facilities, increasing labor costs, and stringent food safety regulations that require minimal human intervention. Fully automatic systems are capable of processing high volumes with precision separation, reduced shell contamination, and optimized yield recovery, making them the preferred choice for large-scale liquid egg and egg powder manufacturers. Their seamless integration into complete egg-breaking, pasteurization, and spray-drying lines further strengthens demand, particularly in export-oriented facilities.

Semi-automatic systems serve mid-sized processors transitioning from manual operations, especially in developing markets where gradual automation is underway. Manual egg separators, while important for niche household and small HoReCa applications, contribute a comparatively small share of revenue due to low unit pricing and limited scalability.

Capacity Insights

High-capacity egg separators (above 20,000 eggs per hour) account for nearly 46% of global market revenue in 2025, making them the leading capacity segment. The primary driver for this dominance is the global expansion of industrial egg processing plants catering to liquid egg exports and large food manufacturers. High-capacity systems enable economies of scale, improved operational efficiency, and consistent product quality—key requirements for multinational food brands and institutional buyers.

Medium-capacity systems (5,001–20,000 eggs per hour) are widely adopted by regional processors supplying domestic bakery and foodservice markets. Low-capacity systems (up to 5,000 eggs per hour) are typically deployed in small-scale operations or emerging markets with limited production volumes. However, the shift toward consolidation and industrialization in poultry processing continues to drive faster growth in the high-capacity segment.

End-Use Industry Insights

Egg processing companies represent the largest end-use segment, contributing approximately 42% of total market share in 2025. This leadership is driven by the growing global demand for pasteurized liquid eggs, egg whites, yolks, and egg powders used across food manufacturing industries. Rising exports of egg-based ingredients, particularly from North America, Europe, China, and Brazil, are accelerating equipment installations in large processing facilities.

Bakery and confectionery manufacturers form the second-largest segment, supported by steady global growth in baked goods consumption and premium dessert categories. Egg whites are critical for aeration and structure, while yolks are widely used in emulsified products. The foodservice and HoReCa sector contributes stable demand in developed markets, especially in North America and Europe, where institutional catering and quick-service restaurants rely heavily on processed egg products for operational efficiency and food safety compliance.

Distribution Channel Insights

Direct sales dominate the distribution landscape, accounting for nearly 65% of total revenue in 2025. Industrial egg separators are high-value capital equipment requiring customization, technical consultation, installation support, and long-term service agreements. As a result, processors typically engage directly with manufacturers through contract-based procurement models. This channel is particularly strong in North America and Europe, where large-scale processing facilities prioritize integrated solutions.

Distributor and dealer networks play a crucial role in emerging markets across Asia-Pacific, Latin America, and Africa, where localized technical support and financing assistance are important. E-commerce channels remain limited to manual and small-scale units targeting household and small commercial users, contributing marginally to total market value.

Explore more data points, trends and opportunities Download Free Sample Report

Egg Separator Market Segmentations

By Product Type

- Manual Egg Separators

- Semi-Automatic Egg Separators

- Fully Automatic Egg Separators

By Capacity

- Low Capacity

- Medium Capacity

- High Capacity

By End-Use Industry

- Egg Processing Companies

- Bakery & Confectionery Manufacturers

- Processed Food Manufacturers

- Foodservice & HoReCa

- Household/Consumer Use

By Distribution Channel

- Direct Sales

- Distributor & Dealer Network

- E-commerce & Retail

Regional Insights

North America

North America accounts for approximately 32% of the global egg separator market in 2025, making it the largest regional market. The United States dominates regional demand due to its highly developed liquid egg processing industry, strong export activity, and large-scale bakery and food manufacturing sectors. The presence of integrated egg processing facilities with advanced automation systems significantly drives equipment upgrades and replacements. Strict food safety regulations enforced by federal agencies further support demand for hygienic, fully automated systems. Canada contributes steadily, driven by processed food production and cross-border trade with the U.S.

Europe

Europe holds nearly 29% market share, supported by advanced food processing infrastructure and stringent EU hygiene standards. The Netherlands serves as a major egg processing and export hub, while Germany, France, and Italy contribute significantly through strong bakery and confectionery industries. Regulatory emphasis on traceability, contamination control, and automation drives adoption of high-performance egg separation systems. Additionally, rising energy efficiency standards encourage processors to invest in modernized, integrated equipment with lower operational costs.

Asia-Pacific

Asia-Pacific represents approximately 27% of global demand and is the fastest-growing region, expanding at nearly 8% CAGR. China leads installations due to its position as the world’s largest egg producer and increasing modernization of poultry and food processing facilities. India is the fastest-growing national market within the region, supported by government-backed food processing initiatives, rising domestic consumption of processed foods, and export expansion. Southeast Asian countries are also witnessing increased investment in poultry integration and industrial food manufacturing, driving demand for mid- and high-capacity separators.

Latin America

Brazil and Mexico drive regional growth in Latin America. Brazil’s strong poultry industry and expanding egg powder exports are key growth drivers, encouraging installation of high-capacity industrial separators. Mexico benefits from rising domestic demand for processed foods and closer trade integration with North America. Gradual modernization of food processing facilities across the region further supports equipment upgrades.

Middle East & Africa

The Middle East is witnessing rising investments in food import substitution strategies, particularly in the UAE and Saudi Arabia, where governments are encouraging domestic food processing capacity to enhance food security. Expansion of integrated poultry farms and processing units is driving demand for industrial egg separators. In Africa, South Africa remains the most established market, supported by a relatively mature food processing sector. Long-term growth in the region is expected to be driven by increasing urbanization, rising protein consumption, and gradual industrialization of poultry value chains.

Key Players in the Egg Separator Market

- SANOVO TECHNOLOGY GROUP

- Moba Group

- OVO-TECH

- Pelbo S.p.A.

- Diamond FoodTech

- KYOWA Machinery

- Actini Group

- Wuhan Anon Tech-Trade

- Zhengzhou Allance Machinery

- Sime-Tek

- Tecno Poultry Equipment

- Buhler Industries

- Ovobel Foods Limited

- Jiangsu Taiyang Machinery

- EDA S.r.l.