Educational Toys Market Size

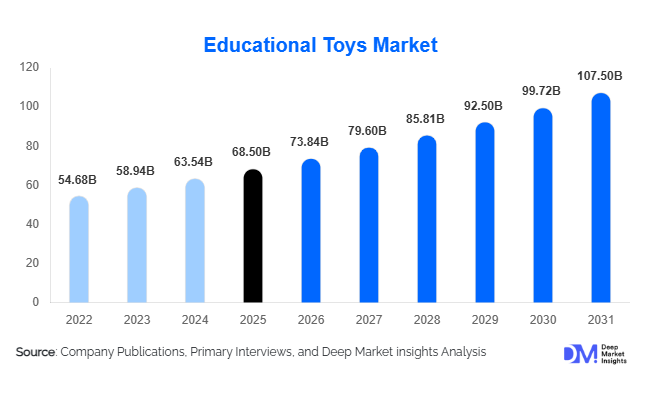

According to Deep Market Insights, the global educational toys market size was valued at USD 68.5 billion in 2025 and is projected to grow from USD 73.84 billion in 2026 to reach USD 107.50 billion by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The educational toys market is experiencing growth primarily driven by increasing parental focus on early childhood development, the rising adoption of STEM-based learning tools, and the integration of digital technologies into interactive toys. Growing awareness of experiential learning, coupled with expanding preschool education and higher disposable incomes in emerging economies, is further accelerating market expansion globally.

Key Market Insights

- STEM-based educational toys are witnessing rapid adoption, driven by global emphasis on future-ready skills such as coding, robotics, and problem-solving.

- Asia-Pacific dominates the market, supported by large child populations, rising middle-class income, and strong manufacturing capabilities.

- Traditional toys still hold a significant market share, reflecting parental concerns over excessive screen time among children.

- E-commerce channels are expanding rapidly, enabling broader product accessibility and direct-to-consumer sales models.

- Eco-friendly and sustainable toys are gaining traction, particularly in Europe and North America, due to regulatory pressures and consumer awareness.

- Technology integration, including AR, AI, and app-based learning platforms, is reshaping product innovation and user engagement.

What are the latest trends in the educational toys market?

Shift Toward Smart and Connected Learning Toys

The educational toys market is witnessing the increasing integration of smart technologies, including artificial intelligence, augmented reality, and IoT-enabled connectivity. Smart toys that adapt to a child’s learning pace and provide personalized educational content are gaining strong traction. App-integrated platforms are enabling real-time feedback, progress tracking, and immersive learning experiences, particularly in STEM and coding-based toys. This trend is especially prominent in developed markets, where digital literacy and access to connected devices are high. Manufacturers are also introducing subscription-based content ecosystems, allowing continuous engagement and recurring revenue streams.

Growing Demand for Sustainable and Eco-Friendly Toys

Sustainability is becoming a key purchasing criterion among consumers, driving demand for educational toys made from biodegradable, recycled, and non-toxic materials. Wooden toys, organic fabrics, and FSC-certified materials are increasingly replacing conventional plastics in premium segments. Regulatory frameworks in Europe and North America are further encouraging this shift by imposing strict safety and environmental standards. Brands that emphasize ethical sourcing and sustainable production are gaining a competitive advantage, particularly among environmentally conscious parents seeking safe and responsible products for children.

What are the key drivers in the educational toys market?

Rising Focus on Early Childhood Development

Increasing awareness regarding the importance of cognitive and motor skill development during early childhood is a major driver of the educational toys market. Parents are actively investing in toys that promote problem-solving, creativity, and social interaction. Educational institutions are also incorporating play-based learning methods, further boosting demand. This trend is particularly strong in urban areas where access to information and educational resources is higher.

Expansion of STEM Education Globally

The global push toward STEM education is significantly influencing the demand for educational toys. Governments and educational bodies are encouraging early exposure to science, technology, engineering, and mathematics, leading to increased adoption of robotics kits, coding toys, and science experiment kits. These products not only enhance academic learning but also prepare children for future career opportunities in technology-driven industries.

What are the restraints for the global market?

High Cost of Advanced Educational Toys

Technologically advanced educational toys, particularly those integrated with AI, AR, and robotics, often come at premium price points. This limits their accessibility in price-sensitive markets and restricts adoption among middle-income households. The cost factor remains a significant barrier, especially in developing economies where affordability plays a crucial role in purchasing decisions.

Concerns Over Screen Time and Digital Dependency

Growing concerns among parents regarding excessive screen time and its impact on children’s health and behavior are restraining the adoption of digital educational toys. Many consumers prefer traditional, non-electronic toys that encourage physical activity and reduce digital exposure. This trend poses a challenge for manufacturers focusing heavily on technology-driven products.

What are the key opportunities in the educational toys industry?

Expansion in Emerging Markets

Emerging economies such as India, China, Brazil, and Southeast Asian countries present significant growth opportunities due to rising disposable incomes, urbanization, and increasing awareness of early education. Government initiatives promoting literacy and skill development are further driving institutional demand for educational toys. Localization of products based on cultural and linguistic preferences can help companies penetrate these markets more effectively.

Integration of Advanced Learning Technologies

The incorporation of advanced technologies such as augmented reality, artificial intelligence, and gamification offers immense opportunities for innovation. Companies that invest in interactive and adaptive learning solutions can differentiate themselves and capture premium segments. Personalized learning experiences and data-driven insights are expected to redefine the educational toys landscape in the coming years.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 68.5 Billion |

| Market Size in 2026 | USD 73.84 Billion |

| Market Size in 2031 | USD 107.50 Billion |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

STEM toys continue to dominate the educational toys market, accounting for approximately 28% of the total market share in 2025. The leadership of this segment is primarily driven by the accelerating global focus on science, technology, engineering, and mathematics (STEM) education as a core foundation for future workforce readiness. Governments across developed and emerging economies are actively promoting STEM-based curricula, which has translated into higher adoption of robotics kits, coding toys, engineering sets, and AI-enabled learning tools. Additionally, partnerships between educational institutions and toy manufacturers are fostering product innovation and enhancing curriculum alignment. The rising penetration of digital learning ecosystems and gamified education platforms is further reinforcing the demand for STEM toys globally.

Beyond STEM, cognitive development toys and creative learning kits represent strong complementary segments, driven by demand for early-stage brain development and artistic expression. Products such as puzzles, logic games, and DIY craft kits are gaining popularity among parents seeking holistic development tools. Role-play and social learning toys are also witnessing increasing adoption, particularly in urban markets, as they help enhance emotional intelligence, communication skills, and collaborative learning among children. This diversification of product offerings is enabling manufacturers to cater to a wide spectrum of developmental needs.

Application Insights

Household consumption remains the largest application segment, contributing nearly 70% of total market demand. This dominance is driven by rising parental awareness regarding the importance of early childhood development and increasing discretionary spending on educational products. Urban households, particularly in developed economies and fast-growing emerging markets, are prioritizing experiential learning tools that combine education with entertainment. The proliferation of nuclear families and dual-income households is also contributing to higher spending on premium educational toys.

Educational institutions represent the fastest-growing application segment, supported by the widespread adoption of activity-based and experiential learning methodologies. Schools and preschools are increasingly integrating educational toys into their teaching frameworks to enhance student engagement and improve learning outcomes. Government-led initiatives aimed at strengthening foundational literacy and numeracy are further boosting institutional demand. Additionally, therapy and special education centers are emerging as a niche but high-growth segment, leveraging sensory and cognitive toys for developmental interventions, particularly for children with autism spectrum disorders and learning disabilities. This segment is expected to witness steady expansion as awareness and diagnosis rates continue to rise globally.

Distribution Channel Insights

Offline retail channels continue to dominate the educational toys market, accounting for approximately 55% of total sales. The preference for physical retail is largely driven by the need for product evaluation, safety assurance, and tactile experience before purchase, especially for younger children’s products. Specialty toy stores and large-format retail chains play a crucial role in influencing purchase decisions through in-store demonstrations and curated product displays.

However, online retail is emerging as the fastest-growing distribution channel, driven by increasing internet penetration, smartphone adoption, and the expansion of e-commerce platforms. Consumers benefit from a wider product assortment, competitive pricing, and access to reviews and ratings, which enhance decision-making. Direct-to-consumer (D2C) models are also gaining traction, enabling brands to establish stronger relationships with customers, offer personalized recommendations, and improve profit margins by reducing intermediary costs. Subscription-based educational kits and digital learning ecosystems are further strengthening the online sales channel.

Age Group Insights

The 3–6 years age group holds the largest market share at approximately 26%, driven by the critical importance of early childhood learning and skill development. This stage is characterized by rapid cognitive, linguistic, and motor skill development, prompting parents and educators to invest heavily in educational toys that support foundational learning. Products such as alphabet games, number kits, shape sorters, and interactive learning boards are highly popular within this segment.

The 6–10 years segment is also significant, particularly for STEM-based and advanced learning kits that promote analytical thinking, problem-solving, and creativity. Increasing school integration of STEM curricula is further boosting demand in this category. Meanwhile, the 0–3 years segment focuses on sensory and developmental toys designed to enhance motor skills and sensory perception. The 10–14 years category is gradually gaining traction with advanced robotics, coding kits, and hobby-based learning tools, reflecting a shift toward specialized skill development at an early age.

Explore more data points, trends and opportunities Download Free Sample Report

Educational Toys Market Segmentations

By Product Type

- STEM Toys

- Language & Literacy Toys

- Cognitive Development Toys

- Creative & Art-Based Toys

- Sensory & Motor Skill Toys

- Role Play & Social Learning Toys

By Age Group

- 0–3 Years

- 3–6 Years

- 6–10 Years

- 10–14 Years

- Above 14 Years

By Technology Integration

- Traditional (Non-electronic)

- Electronic Interactive Toys

- Smart Connected Toys

- AR/VR-Based Educational Toys

By Distribution Channel

- Offline Retail

- Online Retail

- Institutional Sales

By End-Use

- Household Consumers

- Educational Institutions

- Therapy & Special Education Centers

Regional Insights

North America

North America accounts for approximately 30% of the global educational toys market, with the United States contributing nearly 80% of regional demand. Growth in this region is primarily driven by high disposable income levels, strong awareness of the importance of early childhood education, and the widespread adoption of STEM-based learning tools. The presence of leading market players and continuous product innovation is further supporting market expansion. Additionally, increasing integration of technology into learning, including AI-enabled and app-connected toys, is enhancing consumer engagement. Government support for early education programs and strong retail infrastructure also contribute significantly to regional growth.

Europe

Europe holds around 25% of the market share, led by countries such as Germany, the United Kingdom, and France. The region’s growth is strongly influenced by stringent safety and environmental regulations, which are driving demand for high-quality, non-toxic, and sustainable educational toys. Consumer preference for eco-friendly products, particularly wooden and biodegradable toys, is shaping product innovation. Additionally, well-established preschool education systems and government-backed early learning initiatives are supporting consistent demand. Increasing emphasis on ethical sourcing and sustainability certifications is also encouraging manufacturers to adopt greener production practices.

Asia-Pacific

Asia-Pacific is the largest and fastest-growing region, accounting for approximately 35% of the global market, with a CAGR exceeding 9%. Growth is driven by large child populations, rising disposable incomes, rapid urbanization, and increasing awareness of early education. China and India are the key growth engines, with China contributing over 40% of regional demand due to its strong manufacturing base and export capabilities. Government initiatives promoting domestic manufacturing and education, such as skill development programs, are further accelerating market expansion. Additionally, the rapid growth of e-commerce platforms in the region is enhancing product accessibility and driving sales.

Latin America

Latin America accounts for nearly 5% of the market, with Brazil and Mexico leading demand. The region’s growth is supported by improving economic conditions, a rising middle-class population, and increasing awareness of child development and early education. Expansion of retail infrastructure and growing penetration of online sales channels are also contributing to market growth. Government investments in education and literacy programs are gradually boosting institutional demand for educational toys.

Middle East & Africa

The Middle East & Africa region holds approximately 5% market share, with countries such as the UAE and South Africa witnessing steady growth. Increasing investments in education infrastructure, rising urbanization, and growing expatriate populations are key drivers of demand in this region. The presence of international retail chains and premium toy brands in the Middle East is supporting the adoption of high-quality educational toys. In Africa, gradual improvements in education access and government initiatives aimed at enhancing literacy rates are expected to drive long-term market growth, although affordability remains a key challenge.

Key Players in the Educational Toys Market

- LEGO Group

- Mattel Inc.

- Hasbro Inc.

- Ravensburger AG

- Melissa & Doug

- VTech Holdings Ltd.

- Spin Master Corp.

- Bandai Namco Holdings

- TOMY Company Ltd.

- LeapFrog Enterprises

- Playmobil

- Gigo Toys

- Hape International

- Smartivity Labs

- ThinkFun Inc.