Eczema Skin Care Products Market Size

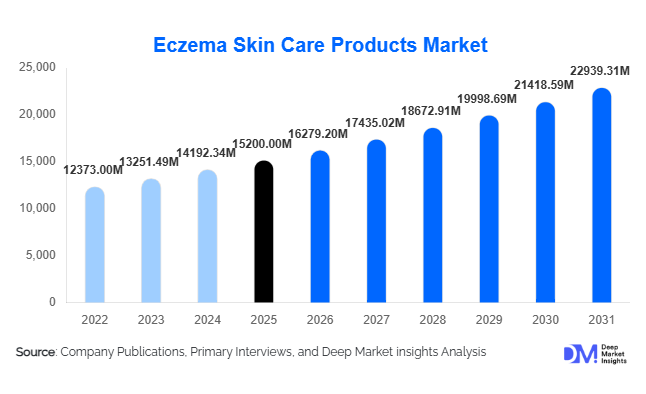

According to Deep Market Insights, the global eczema skin care products market size was valued at USD 15,200 million in 2025 and is projected to grow from USD 16,279.20 million in 2026 to reach USD 22,939.31 million by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). The market growth is primarily driven by the rising global prevalence of atopic dermatitis, increasing awareness regarding dermatological health, and the growing demand for specialized, non-irritating skincare formulations. The shift toward preventive skincare, coupled with expanding access to OTC dermatology products and advancements in biologics and non-steroidal treatments, is significantly shaping the global market landscape.

Key Market Insights

- Emollients and barrier repair moisturizers dominate, accounting for over one-third of total market demand due to their daily-use applicability.

- Non-steroidal and hypoallergenic formulations are gaining traction, driven by safety concerns associated with long-term steroid use.

- North America leads the market, supported by advanced healthcare infrastructure and strong consumer awareness.

- Asia-Pacific is the fastest-growing region, fueled by rising disposable incomes and increasing dermatological diagnosis rates.

- E-commerce is transforming distribution, enabling access to niche and premium dermatology products globally.

- Natural and clean-label skincare products are emerging as a key trend, especially among younger and health-conscious consumers.

What are the latest trends in the eczema skin care products market?

Shift Toward Natural and Microbiome-Friendly Formulations

Consumers are increasingly opting for products formulated with natural ingredients such as colloidal oatmeal, ceramides, and plant-based oils. This trend is driven by growing concerns over synthetic chemicals and skin sensitivity. Manufacturers are investing in microbiome-friendly products that maintain skin barrier integrity while reducing inflammation. Clean-label positioning, sustainability, and dermatological testing are becoming essential differentiators, particularly in premium product segments.

Digitalization and Direct-to-Consumer Expansion

The rise of e-commerce and tele-dermatology platforms is reshaping how consumers access eczema treatments. Direct-to-consumer brands are leveraging digital marketing, subscription models, and personalized skincare solutions to engage users. Online platforms enable better product comparison, reviews, and accessibility, particularly in emerging markets. AI-driven skin analysis tools and virtual consultations are further enhancing customer engagement and treatment adherence.

What are the key drivers in the eczema skin care products market?

Increasing Global Prevalence of Eczema

The rising incidence of eczema, particularly among infants and children, is a primary growth driver. Environmental factors such as pollution, climate change, and allergen exposure are contributing to higher diagnosis rates. This has led to sustained demand for both OTC and prescription-based skincare products globally.

Advancements in Dermatological Treatments

Innovations in skincare formulations, including ceramide-based moisturizers and biologics, are improving treatment outcomes. Non-steroidal options such as calcineurin inhibitors are gaining popularity due to fewer side effects, encouraging long-term usage, and expanding the addressable market.

Growing Consumer Awareness and Preventive Skincare

Rising awareness about skin health and preventive care is driving early adoption of eczema-friendly products. Consumers are increasingly incorporating therapeutic skincare into daily routines, boosting demand for mild and moderate eczema solutions.

What are the restraints for the global market?

Side Effects of Steroid-Based Treatments

Long-term use of corticosteroids can lead to adverse effects such as skin thinning and dependency, limiting their adoption. This has led to cautious usage among patients and healthcare providers, restraining growth in this segment.

High Cost of Advanced Therapies

Biologics and advanced prescription treatments remain expensive, restricting accessibility in low- and middle-income regions. Cost barriers continue to limit market penetration despite strong clinical efficacy.

What are the key opportunities in the eczema skin care products industry?

Expansion in Emerging Markets

Emerging economies such as India, China, and Brazil offer significant growth opportunities due to large untapped populations and improving healthcare access. Localization strategies and affordable product offerings can drive market expansion in these regions.

Development of Non-Steroidal Therapies

The demand for safer alternatives to corticosteroids is creating opportunities for innovation in non-steroidal and biologic treatments. Companies investing in targeted therapies can capture premium market segments and address unmet clinical needs.

Growth of Clean and Sustainable Skincare

Increasing consumer preference for organic and eco-friendly products is driving demand for clean-label eczema solutions. Brands focusing on transparency, sustainability, and ethical sourcing are well-positioned to gain a competitive advantage.

Product Type Insights

Emollients continue to dominate the eczema skin care products market, accounting for approximately 34% of the global market share in 2025. Their leadership is primarily driven by their role as the first-line treatment recommended by dermatologists across all severity levels of eczema. Emollients help restore the skin barrier, reduce moisture loss, and prevent flare-ups, making them essential for both acute and maintenance therapy. The increasing prevalence of mild-to-moderate eczema cases globally further strengthens their demand, as these conditions are largely managed through consistent moisturization. Additionally, the growing consumer shift toward preventive skincare and daily-use therapeutic products has reinforced the adoption of emollients. Barrier repair moisturizers are also gaining strong momentum, particularly due to advancements in ceramide-based formulations that actively rebuild the skin’s natural defense. Anti-itch products are witnessing increased uptake among chronic eczema patients, especially those seeking non-steroidal, long-term relief solutions, thereby supporting overall segment expansion.

Ingredient Composition Insights

Hypoallergenic and fragrance-free formulations hold around 28% market share, maintaining their leadership due to heightened consumer awareness regarding skin sensitivity and allergic reactions. The dominance of this segment is driven by strong dermatologist recommendations, particularly for pediatric and sensitive-skin patients. Increasing incidences of contact dermatitis and allergic triggers have led consumers to actively avoid artificial fragrances, preservatives, and harsh chemicals. Additionally, regulatory frameworks in developed regions are encouraging the use of safer, clinically tested ingredients, further supporting this segment’s growth. Natural and herbal formulations are emerging as the fastest-growing sub-segment, driven by rising demand for clean-label and sustainable skincare. Ingredients such as colloidal oatmeal, aloe vera, and plant-based oils are gaining popularity due to their perceived safety and efficacy, especially among younger and health-conscious consumers.

Distribution Channel Insights

Retail pharmacies dominate the distribution landscape with nearly 31% market share, largely due to their accessibility, established trust among consumers, and the availability of pharmacist guidance. Consumers often rely on pharmacies for OTC eczema treatments, especially in cases requiring immediate relief or professional advice without a prescription. The presence of well-known dermatological brands in pharmacy chains further reinforces this segment’s leadership. However, e-commerce platforms are the fastest-growing distribution channel, driven by increasing internet penetration, convenience, and the ability to access a wide range of global and niche products. Digital platforms also enable consumers to compare ingredients, read reviews, and access personalized recommendations, significantly influencing purchasing decisions. Subscription-based skincare models and direct-to-consumer (D2C) brands are further accelerating growth in this segment.

Age Group Insights

Infants and children represent the largest segment, accounting for approximately 40% of total demand, primarily due to the higher prevalence of eczema in pediatric populations. This segment’s dominance is driven by the early onset of atopic dermatitis, which often begins in infancy and requires long-term management. Parents are increasingly investing in specialized, safe, and dermatologically tested products for their children, contributing to sustained demand. Additionally, pediatric-focused product innovation, such as ultra-mild formulations, tear-free cleansers, and hypoallergenic moisturizers, has strengthened this segment’s growth. The increasing awareness among parents regarding early diagnosis and preventive care further supports the expansion of this category globally.

Severity Level Insights

Mild eczema cases dominate the market with a 46% share, as the majority of patients experience manageable symptoms that can be treated with OTC products such as emollients and gentle cleansers. The growth of this segment is driven by increased awareness and early-stage diagnosis, enabling consumers to manage symptoms before progression to severe conditions. Additionally, the availability of affordable OTC solutions and the shift toward preventive skincare routines have reinforced the dominance of this segment. Moderate and severe eczema segments, while smaller in share, are witnessing steady growth due to increasing adoption of prescription-based treatments, including biologics and advanced topical therapies, particularly in developed healthcare markets.

End-Use Insights

Individual consumers account for approximately 55% of the market, reflecting the strong preference for self-care and OTC treatment options. This segment’s leadership is driven by the convenience, affordability, and accessibility of non-prescription products, particularly for mild and moderate eczema cases. The growing trend of self-diagnosis and digital health awareness has further encouraged consumers to manage their condition independently. Dermatology clinics and hospitals are experiencing steady growth, supported by increasing demand for specialized care, particularly for chronic and severe eczema cases. The expansion of tele-dermatology services and improved access to healthcare professionals are also contributing to the growth of institutional end-users.

| By Product Type | By Ingredient Composition | By Distribution Channel | By Severity Level | By End User |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds the largest share at approximately 38% of the global market in 2025, led by the United States. The region’s dominance is driven by high awareness levels, advanced healthcare infrastructure, and the strong presence of leading dermatology and pharmaceutical companies. Additionally, the high prevalence of eczema, particularly among children, and increased healthcare spending significantly contribute to market growth. The widespread availability of premium and prescription-based treatments, coupled with robust insurance coverage and reimbursement policies, further accelerates adoption. Continuous product innovation and strong regulatory oversight, ensuring product safety, also reinforce market expansion in this region.

Europe

Europe accounts for around 27% market share, with Germany, the UK, and France leading demand. The region’s growth is supported by stringent regulatory frameworks that promote the use of safe, dermatologically tested products. High consumer awareness regarding skin health and a strong preference for hypoallergenic and organic formulations are key growth drivers. Additionally, increasing adoption of sustainable and eco-friendly skincare products aligns with European consumer values, further boosting demand. Government support for healthcare accessibility and the rising prevalence of allergic skin conditions also contribute to steady market growth across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR of approximately 8.5%. China and India are key growth drivers due to their large populations, rising disposable incomes, and increasing awareness of dermatological health. Rapid urbanization and rising pollution levels are contributing to higher incidences of eczema, thereby driving demand for treatment products. Additionally, expanding e-commerce penetration and the availability of affordable skincare solutions are improving product accessibility. Countries such as Japan and South Korea are also contributing to growth through innovation in advanced skincare formulations and strong consumer demand for premium products.

Latin America

Brazil and Mexico dominate the regional market, supported by expanding retail infrastructure and a growing middle-class population. Increasing awareness of skin health and improved access to dermatological care are key drivers of growth in this region. The rising penetration of international skincare brands and the expansion of e-commerce platforms are further enhancing product availability. Additionally, climatic conditions such as high humidity and heat contribute to skin sensitivity issues, indirectly driving demand for eczema skincare solutions.

Middle East & Africa

The Middle East and Africa region shows moderate growth, led by the UAE and Saudi Arabia. Rising healthcare investments, improving medical infrastructure, and increasing awareness of skin disorders are key growth drivers. The region’s harsh climatic conditions, including extreme heat and dryness, contribute to higher incidences of skin irritation and eczema, supporting product demand. Additionally, the growing presence of international skincare brands and the expansion of premium retail channels are enhancing market penetration. Government initiatives aimed at improving healthcare access and increasing dermatology services further support long-term growth in this region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|