Eco-Friendly Recycled Toilet Paper Market Size

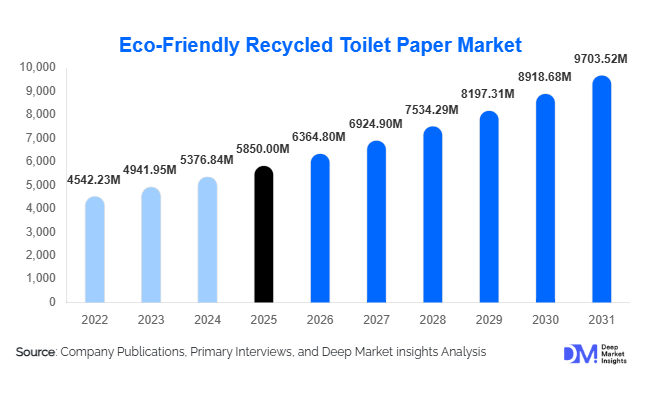

According to Deep Market Insights, the global eco-friendly recycled toilet paper market size was valued at USD 5,850 million in 2025 and is projected to grow from USD 6,364.80 million in 2026 to reach USD 9,703.52 million by 2031, expanding at a CAGR of 8.8% during the forecast period (2026–2031). The market growth is primarily driven by increasing environmental awareness, rising demand for sustainable household products, and regulatory pressure to reduce deforestation and carbon emissions associated with virgin pulp production.

Key Market Insights

- Consumer preference is rapidly shifting toward sustainable hygiene products, with recycled toilet paper gaining mainstream adoption across residential and commercial segments.

- Plastic-free and compostable packaging solutions are becoming a major differentiator, influencing brand positioning and purchase decisions.

- North America dominates the market, supported by strong retail penetration and high sustainability awareness.

- Asia-Pacific is the fastest-growing region, driven by urbanization, rising middle-class income, and increasing environmental consciousness.

- Direct-to-consumer subscription models are transforming distribution, offering convenience and improving customer retention.

- Technological advancements in fiber processing are improving product softness and strength, reducing the quality gap with virgin pulp products.

What are the latest trends in the eco-friendly recycled toilet paper market?

Shift Toward Plastic-Free and Zero-Waste Packaging

Manufacturers are increasingly adopting plastic-free packaging solutions, including paper wraps and compostable materials, to align with zero-waste consumer preferences. This trend is particularly strong in developed markets where regulatory pressure and consumer activism are high. Brands are leveraging packaging as a key sustainability differentiator, with many introducing minimalist and recyclable packaging formats. Retailers are also prioritizing shelf space for products that meet sustainability benchmarks, further accelerating adoption.

Growth of Direct-to-Consumer and Subscription Models

Subscription-based purchasing is emerging as a key trend, particularly in North America and Europe. Consumers prefer recurring delivery models for essential goods, ensuring convenience and cost savings. Brands are utilizing digital platforms to build direct relationships with customers, communicate sustainability narratives, and offer personalized product bundles. This trend is enhancing customer loyalty while reducing dependency on traditional retail channels.

What are the key drivers in the eco-friendly recycled toilet paper market?

Rising Environmental Awareness

Consumers are increasingly aware of the environmental impact of deforestation and water-intensive manufacturing processes associated with virgin pulp products. This has led to a shift toward recycled alternatives that use significantly less water and energy. The willingness to pay a premium for sustainable products is rising, particularly among urban and younger demographics, directly boosting market growth.

Regulatory Support and Corporate ESG Commitments

Governments and corporations are implementing sustainability policies that favor recycled products. Public procurement policies mandating recycled content in hygiene products are creating stable demand. Additionally, corporate ESG commitments are driving bulk adoption in offices, hospitality, and healthcare sectors.

Technological Advancements in Product Quality

Advancements in de-inking, fiber processing, and blending technologies have significantly improved the softness and durability of recycled toilet paper. These innovations are helping manufacturers overcome historical quality concerns, enabling recycled products to compete effectively with premium virgin pulp alternatives.

What are the restraints for the global market?

Higher Production Costs

Despite using recycled materials, the processing of waste paper involves complex cleaning and decontamination processes, leading to higher production costs. This results in higher retail prices compared to conventional toilet paper, limiting adoption in price-sensitive markets.

Raw Material Supply Constraints

The availability of high-quality post-consumer recycled paper varies significantly across regions. Inconsistent supply and price volatility of raw materials pose challenges for manufacturers, particularly in emerging markets with underdeveloped recycling infrastructure.

What are the key opportunities in the eco-friendly recycled toilet paper industry?

Institutional Procurement and Government Mandates

Government policies mandating sustainable procurement in public infrastructure, schools, and offices are creating significant opportunities. Long-term contracts with public institutions provide stable demand and encourage large-scale adoption of recycled toilet paper products.

Expansion in Emerging Markets

Emerging economies such as India, China, and Brazil present substantial growth potential due to rising hygiene awareness and urbanization. Local production using agricultural residues like bagasse and bamboo can reduce costs and enhance sustainability, making products more accessible.

E-commerce and Digital Brand Building

The rapid growth of e-commerce platforms enables brands to reach a wider audience and build strong sustainability-focused narratives. Digital channels also facilitate subscription models and direct engagement with eco-conscious consumers, enhancing market penetration.

Product Type Insights

Premium 2-ply recycled toilet paper dominates the global market, accounting for approximately 42% share in 2025. This segment leads primarily due to its optimal balance between affordability, comfort, and sustainability, making it the preferred choice for both residential consumers and institutional buyers. The growing consumer expectation for softness comparable to virgin pulp products has driven innovation in fiber blending and processing technologies, enabling 2-ply recycled variants to achieve higher durability and comfort standards. As a result, this segment has successfully transitioned from a mid-tier offering to a mainstream product category across developed markets.

Ultra-soft multi-ply variants (3-ply and above) are witnessing strong growth, particularly in North America and Europe, where premiumization trends and higher disposable incomes support demand. These products cater to consumers seeking luxury hygiene experiences without compromising environmental values. Meanwhile, unbleached and natural brown recycled toilet paper is gaining traction among highly eco-conscious consumers, driven by the demand for chemical-free and minimally processed products. Although these variants currently hold a smaller share, they are expanding steadily due to increasing awareness of chlorine-free and toxin-free manufacturing processes. Overall, the shift from basic 1-ply to higher-quality recycled products reflects both improving consumer perception and continuous technological advancements in product development.

Application (End-Use) Insights

The residential segment remains the largest contributor to the eco-friendly recycled toilet paper market, accounting for approximately 52% of total demand in 2025. This dominance is driven by daily consumption patterns, increasing awareness of sustainable living, and the growing availability of eco-friendly products through retail and e-commerce channels. Consumers are increasingly incorporating environmentally responsible products into routine household purchases, making residential usage the backbone of market demand.

However, commercial end-use segments are emerging as the fastest-growing contributors. The hospitality industry, in particular, is witnessing accelerated adoption as hotels and resorts integrate eco-friendly products to align with sustainability certifications and enhance brand positioning among environmentally conscious travelers. Similarly, healthcare facilities and corporate offices are adopting recycled toilet paper to meet ESG targets and regulatory compliance requirements. Bulk procurement policies and cost efficiencies in large-scale purchasing further support this trend. Public infrastructure applications, including airports, railways, and government buildings, are also expanding rapidly due to mandated green procurement policies. These segments are expected to drive incremental demand growth over the forecast period, supported by institutional sustainability initiatives.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate the distribution landscape, holding approximately 46% market share in 2025. Their leadership is driven by extensive product visibility, established consumer trust, and the ability to offer a wide range of eco-friendly options under one roof. Retail chains are increasingly prioritizing shelf space for sustainable products, supported by private-label eco-friendly offerings that enhance affordability and accessibility.

Online retail is the fastest-growing distribution channel, fueled by rising digital adoption, convenience, and the increasing popularity of subscription-based purchasing models. E-commerce platforms enable consumers to access detailed product information, sustainability certifications, and customer reviews, influencing purchasing decisions. Direct-to-consumer (D2C) models are gaining significant traction, allowing brands to build stronger relationships with customers, offer customized product bundles, and ensure recurring revenue through subscription services. Additionally, institutional sales through bulk contracts represent a substantial channel, particularly for commercial and public sector buyers, where long-term supply agreements and cost efficiencies play a critical role in procurement decisions.

| By Product Type | By Application | By Distribution Channel | By Raw Material Source | By Packaging Type |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America leads the global eco-friendly recycled toilet paper market with an estimated 34% share in 2025, driven primarily by the United States. The region benefits from high consumer awareness regarding environmental sustainability, well-established retail infrastructure, and strong penetration of eco-labeled products. A key growth driver is the widespread adoption of corporate ESG initiatives, with large organizations and institutions mandating sustainable procurement practices. Additionally, the presence of leading manufacturers and strong innovation capabilities supports product development and market expansion. Government regulations promoting recycling and waste reduction, along with high purchasing power, further reinforce North America’s market leadership.

Europe

Europe accounts for approximately 30% of the global market, with major contributions from Germany, the United Kingdom, and France. The region’s growth is strongly driven by stringent environmental regulations, including mandates on recycled content and restrictions on deforestation-linked products. Europe’s advanced recycling infrastructure and well-established circular economy frameworks enable efficient raw material sourcing and production. Consumer preference for sustainable and ethically produced goods is significantly higher compared to global averages, further accelerating demand. Additionally, government incentives and eco-label certifications such as EU Ecolabel play a critical role in influencing purchasing decisions across both residential and institutional segments.

Asia-Pacific

Asia-Pacific holds around 22% market share and represents the fastest-growing region, with a CAGR exceeding 10% during the forecast period. China and India are the primary growth engines, driven by large populations, rapid urbanization, and rising middle-class income levels. Increasing awareness of hygiene and environmental sustainability is contributing to higher adoption rates. Government initiatives promoting waste management and recycling infrastructure development are also key drivers. Japan stands out as a technologically advanced market, with high adoption of recycled products supported by efficient recycling systems. Additionally, the availability of alternative raw materials such as bamboo and agricultural residues enhances regional production capabilities and cost competitiveness.

Latin America

Latin America accounts for approximately 8% of the global market, led by Brazil and Mexico. The region’s growth is driven by urbanization, expanding retail networks, and a gradual improvement in consumer awareness regarding sustainable products. Increasing investments in retail infrastructure and the entry of international brands are enhancing product availability. However, price sensitivity remains a key challenge, limiting the widespread adoption of premium eco-friendly products. Government efforts to improve waste management systems and recycling rates are expected to support long-term market growth, particularly in urban centers.

Middle East & Africa

The Middle East & Africa region holds around 6% market share, with demand concentrated in countries such as the UAE and South Africa. Growth in this region is driven by rising urbanization, increasing disposable incomes, and growing awareness of sustainability, particularly among affluent consumers. The hospitality sector plays a significant role, as luxury hotels and resorts adopt eco-friendly products to meet international sustainability standards. Government initiatives promoting environmental conservation and green building practices are also contributing to market expansion. However, limited recycling infrastructure and lower awareness levels in certain areas continue to pose challenges to widespread adoption.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Eco-Friendly Recycled Toilet Paper Market

- Kimberly-Clark Corporation

- Procter & Gamble

- Essity AB

- Cascades Inc.

- Clearwater Paper Corporation

- Sofidel Group

- Seventh Generation Inc.

- Who Gives A Crap

- Marcal Paper Mills

- WEPA Group

- Oji Holdings Corporation

- Georgia-Pacific LLC

- Kruger Inc.

- Renova Group

- Hengan International Group