Eco-Friendly Plastic Bags Market Size

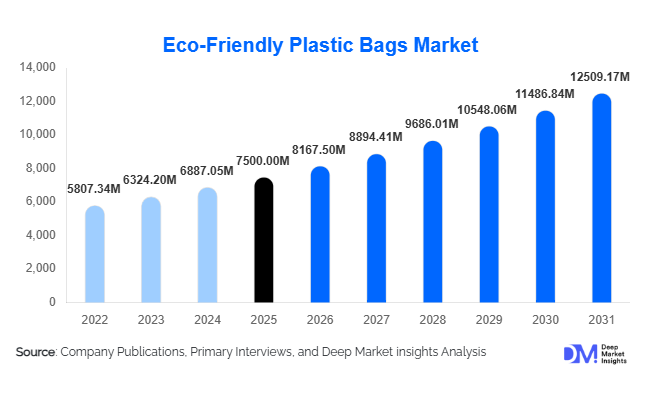

According to Deep Market Insights, the global eco-friendly plastic bags market size was valued at USD 7,500 million in 2025 and is projected to grow from USD 8,167.50 million in 2026 to reach USD 12,509.17 million by 2031, expanding at a CAGR of 8.9% during the forecast period (2026–2031). The eco-friendly plastic bags market growth is primarily driven by stringent government regulations banning single-use plastics, rising adoption of biodegradable and compostable materials, and increasing corporate sustainability commitments across retail, e-commerce, and food packaging industries.

The market is undergoing a structural transformation as industries shift from conventional polyethylene bags to sustainable alternatives such as PLA, PHA, starch blends, recycled plastics, and Oxo-biodegradable materials. Retail and supermarket chains are leading this transition due to high-volume consumption and regulatory pressure, while e-commerce and food delivery sectors are emerging as fast-growing application areas. Asia-Pacific dominates global production due to strong manufacturing capabilities, whereas Europe leads in regulatory-driven demand. North America continues to expand steadily, driven by corporate ESG initiatives and state-level plastic bans. Overall, the market is evolving into a mainstream packaging segment supported by innovation in bio-based materials, expanding recycling infrastructure, and increasing global awareness regarding environmental sustainability.

Key Market Insights

- Biodegradable and compostable materials are rapidly replacing conventional plastics, especially in retail and food packaging applications.

- Retail and supermarkets remain the dominant end-use segment, accounting for the highest consumption of eco-friendly plastic bags globally.

- Asia-Pacific dominates global supply and manufacturing, led by China and India, supported by large-scale production capabilities.

- Europe is the most regulation-driven market, with strict bans on single-use plastics accelerating adoption of sustainable alternatives.

- E-commerce and food delivery sectors are the fastest-growing applications, driven by packaging intensity and sustainability mandates.

- Corporate ESG commitments are significantly accelerating demand, especially among global retail chains and FMCG companies.

What are the latest trends in the eco-friendly plastic bags market?

Shift Toward Advanced Bio-Based Polymers

The market is witnessing a strong transition toward advanced bio-based materials such as PLA, PHA, and starch blends that offer improved biodegradability and mechanical strength. Manufacturers are increasingly investing in next-generation polymer technologies that reduce dependence on fossil-fuel-based plastics. These materials are being optimized for large-scale retail and industrial applications, ensuring performance parity with conventional plastics. Innovation in enzymatic degradation and nanotechnology reinforcement is also enhancing durability while maintaining eco-friendly properties, enabling broader adoption across high-volume packaging applications.

Integration of Circular Economy Models

Companies are increasingly aligning with circular economy principles by incorporating recycled content and designing bags for reuse and recyclability. Retailers are implementing closed-loop systems where used plastic bags are collected, processed, and reintroduced into production cycles. Governments are also promoting extended producer responsibility (EPR) frameworks, encouraging manufacturers to manage product lifecycle impacts. This trend is reshaping procurement strategies, particularly in Europe and North America, where sustainability compliance is becoming mandatory for market participation.

Rapid Expansion of Sustainable E-commerce Packaging

The surge in online retail and food delivery platforms has significantly increased demand for eco-friendly courier and packaging bags. Companies such as Amazon-style marketplaces and regional delivery platforms are shifting toward compostable and recyclable packaging formats to meet sustainability goals. This trend is particularly strong in Asia-Pacific and Latin America, where digital commerce penetration is rising rapidly. Lightweight biodegradable bags designed for logistics efficiency and branding customization are becoming a key product category in this segment.

What are the key drivers in the eco-friendly plastic bags market?

Stringent Environmental Regulations and Plastic Bans

Government regulations across more than 60 countries banning or restricting single-use plastics are the strongest growth driver for the market. Policies such as taxation on plastic bags, mandatory compostable packaging standards, and extended producer responsibility frameworks are accelerating substitution toward eco-friendly alternatives. These regulations are particularly strict in Europe and parts of Asia, directly influencing procurement decisions across retail and FMCG sectors.

Rising Corporate Sustainability and ESG Commitments

Global corporations are increasingly adopting ESG frameworks, which require measurable reductions in plastic waste and carbon footprint. Retail giants, quick-service restaurants, and e-commerce platforms are transitioning to biodegradable packaging to meet sustainability targets. This shift is creating large-scale institutional demand for eco-friendly plastic bags, particularly through long-term supply contracts with certified manufacturers.

Growing Consumer Preference for Sustainable Products

Consumer awareness regarding environmental pollution and plastic waste is significantly influencing purchasing behavior. Urban populations are increasingly favoring brands that adopt eco-friendly packaging solutions, forcing companies to adopt biodegradable and recyclable bags as part of their branding strategy. This behavioral shift is especially strong in developed economies and metropolitan regions across Asia-Pacific.

What are the restraints for the global market?

High Production and Material Costs

Eco-friendly plastic bags remain significantly more expensive than conventional plastic alternatives due to high costs of bio-based raw materials such as PLA and PHA. Limited economies of scale and dependence on agricultural feedstocks further increase price volatility, making adoption challenging in price-sensitive developing markets.

Limited Composting and Recycling Infrastructure

Many regions lack adequate industrial composting and recycling infrastructure required for proper degradation of eco-friendly plastics. As a result, compostable bags often end up in landfills, reducing their environmental effectiveness and creating skepticism among consumers and regulators, which slows down adoption rates.

What are the key opportunities in the eco-friendly plastic bags industry?

Technological Advancements in Bio-Polymer Manufacturing

Innovations in bio-polymer production, including cost-efficient fermentation processes and hybrid material engineering, present major opportunities for manufacturers. Scaling production of PLA and PHA materials can significantly reduce costs, improving competitiveness against traditional plastics and enabling mass-market adoption.

Expansion in Emerging Markets

Rapid urbanization and regulatory development in emerging economies such as India, Southeast Asia, and Latin America are creating strong demand potential. These regions are implementing phased plastic bans and encouraging domestic production of sustainable packaging, opening opportunities for both local and global manufacturers.

Integration with E-commerce and Logistics Ecosystems

The growing e-commerce sector presents a significant opportunity for eco-friendly courier and packaging bags. Companies are investing in lightweight, durable, and branded biodegradable packaging solutions that align with ESG requirements while supporting logistics efficiency and customer experience enhancement.

Product Type Insights

T-shirt bags dominate the eco-friendly plastic bags market, accounting for approximately 28% of global market share in 2025, primarily due to their extensive usage across supermarkets, grocery chains, and mass retail outlets. Their leadership is driven by high-volume consumption patterns, low production cost, and easy integration into existing retail checkout systems, making them the most commercially viable substitute for conventional plastic carry bags. Additionally, regulatory bans on single-use plastics in retail environments have accelerated their replacement cycle, particularly in Europe and Asia-Pacific.

Garbage and waste bags represent the second-largest segment, supported by growing municipal waste management initiatives and rising household demand for biodegradable disposal solutions. Shopping and grocery bags continue to expand steadily, driven by organized retail penetration and brand-driven sustainable packaging strategies adopted by FMCG companies. Produce bags are witnessing increased adoption in supermarkets transitioning toward plastic-free fresh food sections, particularly in Europe and developed Asia. Meanwhile, e-commerce courier bags are emerging as the fastest-growing segment due to explosive growth in online retail, where packaging intensity, last-mile logistics, and sustainability commitments from digital commerce platforms are driving rapid substitution toward compostable and recycled material-based solutions.

End-Use Insights

The retail and supermarket sector remains the dominant end-use segment, accounting for nearly 31% of total global demand, driven by high-frequency usage, regulatory enforcement at point-of-sale, and corporate sustainability commitments. Large retail chains are transitioning aggressively toward biodegradable packaging to align with ESG reporting requirements and consumer pressure for sustainable alternatives.

Food and beverage applications, particularly quick-service restaurants (QSRs), takeaway services, and food delivery platforms, are experiencing strong growth due to increasing packaging consumption intensity and regulatory push toward compostable materials. E-commerce and logistics represent the fastest-growing end-use segment, supported by rising online order volumes, packaging standardization, and brand-driven sustainability mandates. Municipal waste management is another key contributor, with governments adopting biodegradable garbage bags for public waste collection systems. Industrial and agricultural applications are also gradually expanding as environmental regulations extend beyond consumer-facing sectors into manufacturing and primary industries.

| By Material Type | By Product Type | By End-use Industry | By Distribution Channel |

|---|---|---|---|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global market with approximately 41% market share in 2025, driven by strong manufacturing capabilities, large-scale domestic consumption, and tightening environmental regulations. China serves as the global production hub, benefiting from economies of scale in polymer manufacturing and export-oriented packaging industries. India is witnessing rapid demand growth due to nationwide plastic bans, rising urban retail expansion, and government-led sustainability initiatives such as Swachh Bharat and state-level plastic restrictions. Southeast Asia is also emerging as a high-growth sub-region due to expanding retail infrastructure and increasing adoption of sustainable packaging in food delivery and e-commerce ecosystems. The region’s growth is primarily supported by regulatory enforcement, cost-competitive manufacturing, and accelerating digital commerce penetration.

Europe

Europe accounts for approximately 27% of global demand, making it the most regulation-intensive market globally. Growth is driven by strict EU directives on single-use plastics, circular economy mandates, and extended producer responsibility frameworks. Germany, France, and the United Kingdom are the leading national markets, supported by advanced recycling infrastructure and strong consumer preference for sustainable products. Europe’s demand is further reinforced by corporate ESG compliance requirements and widespread adoption of compostable packaging across retail and food service sectors. The region also benefits from high public awareness regarding environmental sustainability, making eco-friendly plastic bags a default choice in many retail environments.

North America

North America holds approximately 22% market share, led primarily by the United States, followed by Canada. Growth in this region is driven by state-level plastic bag bans, corporate sustainability initiatives, and increasing adoption of recyclable packaging solutions across retail, grocery, and food service industries. California, New York, and several other states are key regulatory drivers, enforcing strict limits on single-use plastics. The region also benefits from strong institutional procurement by large retail chains and quick-service restaurants integrating eco-friendly packaging into supply chains. Additionally, rising consumer awareness and ESG reporting pressures are accelerating adoption across both public and private sectors.

Latin America

Latin America is an emerging market led by Brazil and Mexico, where gradual regulatory frameworks and expanding modern retail networks are driving steady adoption of eco-friendly plastic bags. Growth is primarily supported by increasing urbanization, rising supermarket penetration, and gradual implementation of environmental regulations targeting single-use plastics. Brazil leads regional demand due to its large consumer base and retail expansion, while Mexico is experiencing increased adoption in food delivery and grocery sectors. Although infrastructure limitations exist, improving environmental awareness and foreign investment in retail and packaging industries are expected to accelerate market penetration in the long term.

Middle East & Africa

The Middle East and Africa region is witnessing gradual but steady growth, supported by retail modernization in GCC countries such as the UAE and Saudi Arabia. Government initiatives promoting environmental sustainability and waste reduction are encouraging the adoption of biodegradable packaging materials. The UAE has implemented progressive plastic reduction policies, while Saudi Arabia is investing in sustainable urban development under Vision 2031, indirectly supporting eco-friendly packaging demand. In Africa, South Africa and Kenya are emerging as key markets due to increasing environmental awareness and gradual retail sector formalization. Growth in this region is further supported by rising tourism, expanding FMCG distribution networks, and increasing imports of sustainable packaging products.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Eco-Friendly Plastic Bags Market

- Novolex Holdings

- Berry Global Inc.

- Amcor plc

- Mondi Group

- Sealed Air Corporation

- Huhtamaki

- Coveris Holdings

- Uflex Ltd.

- Poly-America

- Reynolds Group Holdings